Now is the right time to ask whether the monetary policy framework and strategy that worked well in the past are well suited to address the challenges ahead. A flexible price-level targeting framework has the important traits of adaptability, accessibility, and accountability. It also offers significant advantages over inflation targeting for meeting price stability and employment goals. The following is adapted from a presentation by the president and CEO of the San Francisco Fed to the Shadow Open Market Committee in New York on May 5.

When I spoke in New York about a month ago, I contrasted where the U.S. economy was four years ago and where we are now. I have to say, it’s a very different conversation when unemployment is below 5% than it was in early 2013 when the unemployment rate appeared to be stuck at 8%.

It’s been said—and often attributed to C.S. Lewis—that getting over a painful experience is much like crossing monkey bars. You have to let go at some point in order to move forward.

Now that we’ve gotten the monkey of the recession off our backs, we have the luxury of being able to look to the future. This presents us with the opportunity to ask ourselves whether the monetary policy framework and strategy that worked well in the past remains well suited for the road ahead.

Such introspection is healthy and constitutes best practice for any organization. In fact, the Bank of Canada has already shown us the way. Every five years, they conduct a thorough review of whether their policy framework remains most appropriate in a changing world. This is an exercise all central banks should undertake, including the Fed.

There’s a buzzword in the world of emergency response: resiliency. You can’t predict precisely when or where the next storm will arrive, or exactly what it will look like. But you can make yourself resilient, so when the time comes, you’re ready and able to limit the damage and recover quickly.

We need to think of our resiliency toward the next economic storm in the same terms. Although an inflation targeting framework has served central banks across the globe well in the past, the world has changed in ways that call into question its efficacy going forward. In particular, there is mounting evidence that the natural rate of interest, or r-star, in the United States and elsewhere has fallen to historic lows, which hampers the ability of conventional monetary policy to respond to the next downturn (Laubach and Williams 2016, Holston, Laubach, and Williams 2016).

As I have argued before, in the best of all worlds, fiscal and other policies would be put in place that propel long-run economic prosperity and boost r-star on a sustained basis (Williams 2016). Absent such actions, monetary policy will be severely challenged to achieve stable prices and strong macroeconomic performance in a low r-star world. Therefore, now is the right time to examine whether monetary policy frameworks must adapt to changing circumstances.

There are a number of potential alternative strategies to cope with a low natural rate of interest, including regular reliance on unconventional policy tools, negative interest rates, and raising the inflation target (see Williams 2009, Blanchard, Dell’Ariccia, and Mauro 2010, Ball 2014, Reifschneider 2016, Bernanke 2016, Williams 2016, and Kiley and Roberts 2017). Each of these have various advantages and disadvantages.

In my remarks today, I’ll narrow the focus to one alternative policy framework that deserves particular attention because it offers significant advantages over inflation targeting, particularly in a low r-star world: flexible price-level targeting.

First principles

Before diving into the details of price-level targeting, let’s take a step back to first principles and ask: What makes for a successful monetary policy framework?

It comes down to three words: adaptability, accessibility, and accountability.

By this I mean that effective strategies should be able to adapt to change in an uncertain world. They should be accessible and transparent so that the public can plan and act in accordance with the strategy. And they should facilitate accountable benchmarking and performance measurement.

There’s an old joke about economists stranded on a desert island. A can of food washes up on the shore and they try to figure out how to open it. Their solution? “Assume a can opener.” History teaches us that we tend to run into trouble when we “assume a can opener” rather than being prepared to adapt to the realities around us.

As nature abhors a vacuum, monetary policy abhors stasis. Instead of being a rigid set of precepts, it follows the adage of “that which survives is that which is most adaptive to change.”

Underlying constants like potential GDP, the natural rate of unemployment, and the natural rate of interest are not really constant: They change over time in unpredictable ways. Monetary policy has proven most successful when it has been able to account for these changes.

Price-level targeting and anchoring inflation expectations

Although the natural rate of interest is the topic du jour, the challenges for monetary policy to adapt to uncertain and changing natural rates is not new. In a series of research papers, Athanasios Orphanides and I investigated the design of robust monetary policy strategies that can succeed in the face of real-world uncertainties, including about the natural rates of interest and unemployment.

To be precise, we studied what is called a “difference” monetary policy rule. This type of policy strategy is closely related to a version of the Taylor (1993) policy rule, but with the main difference that policy responds to deviations of the level of prices relative to a steadily growing target level, rather than deviations of the inflation rate from a target rate.

One recurring finding of our research is that a policy strategy that targets the price level in this way and responds to the unemployment rate can be highly effective at stabilizing both inflation and unemployment in an environment of structural change and uncertainty (Orphanides and Williams 2002, 2007, 2013). In a nutshell, the big advantage of this approach is that any surges or drops in the inflation rate need to be made up in the future. This assures that, over the medium term, inflation stays on track, even if policymakers have a very imperfect understanding of the levels of natural rates or other structural changes affecting the economy.

As Martin Luther King, Jr. famously said: History is a great teacher. Episodes where monetary policy failed can be just as instructive as times when things went well. In that spirit, Athanasios and I studied a period when monetary policy failed and everyday people paid the price—both figuratively and literally (Orphanides and Williams 2013). I’m talking about the Great Inflation of the late 1960s and 1970s.

With the benefit of hindsight, we re-examined the choices made by policymakers to determine whether the devastating increases in inflation and unemployment that became known as stagflation could have been avoided. Our findings suggest that answer was yes, they could have—if the Fed had instead used an alternative, robust policy strategy that effectively targeted the price level, as well as responded to the unemployment rate.

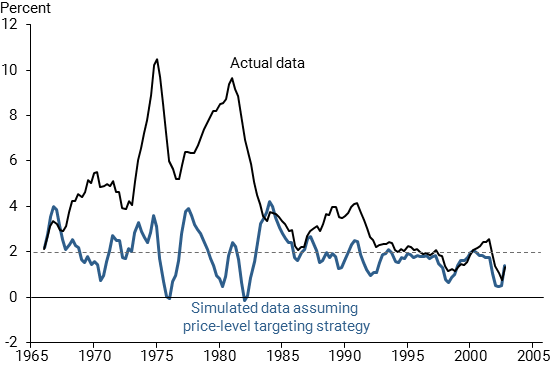

Without going into the details—I invite you to read the paper at your leisure—according to our model simulations, such a robust price-level strategy could have delivered fairly stable inflation throughout the 1960s and 1970s and beyond. This result is seen in Figure 1, where the black line shows the actual inflation rate, which twice reaches double digits. The blue line shows the simulated inflation rate that would have occurred if the Fed followed a policy strategy that aims for a constant 2% increase in the price level starting in 1966 (the simulation ends in 2003).

Figure 1

Inflation

Note: Four-quarter percent change in GDP deflator.

Source: Orphanides and Williams (2013), Bureau of Economic Analysis.

Under the price-level strategy, monetary policy would have avoided the mistake of the late 1960s of allowing the unemployment rate to remain very low for a long time, which contributed to the run-up in inflation during that period. As a result, the Great Inflation never materializes.

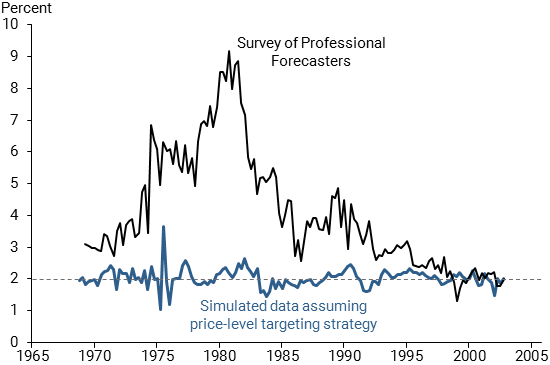

A key to this strategy’s success is the rock-solid anchoring of inflation expectations. Figure 2 compares a real-world measure of one-year-ahead inflation expectations from the Survey of Professional Forecasters (the black line) to the model’s predictions of what inflation expectations would have been if the Fed had followed the price-level targeting strategy (the blue line). An important aspect of this strategy is that it does not allow inflation to stray too far from 2% for long. This “walking the talk” of price stability reinforces the public’s understanding of the policy strategy and creates a positive feedback loop where stable inflation anchors inflation expectations, which in turn fosters stable inflation, which reinforces the anchoring of expectations, and so on.

Figure 2

Expected inflation

Note: Four-quarter percent change in GDP deflator.

Source: Orphanides and Williams (2013), Survey of Professional Forecasters.

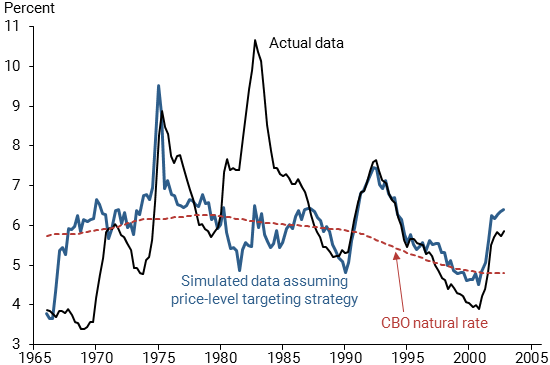

The price-level policy is not only effective in terms of price stability, but also helps stabilize the unemployment rate by avoiding swings in unemployment resulting from the Fed trying to get inflation back on track (Figure 3). With the Great Inflation avoided, the economic slowdown needed to bring inflation down in the early 1980s doesn’t occur. Interestingly, the policy strategy followed in this model simulation implicitly assumes a constant natural rate of unemployment. Nonetheless, the policy does a reasonably good job of tracking the natural rate of unemployment, which is assumed to be equal to the Congressional Budget Office’s estimate shown by the dashed red line in the figure.

Figure 3

Unemployment rate

Source: Orphanides and Williams (2013), Bureau of Economic Analysis, and Congressional Budget Office.

Price-level targeting and low r-star

This analysis makes a strong case for a flexible price-level targeting in “normal” times of change and uncertainty. But we are now living in a “low r-star world,” and that only strengthens the case for price-level targeting.

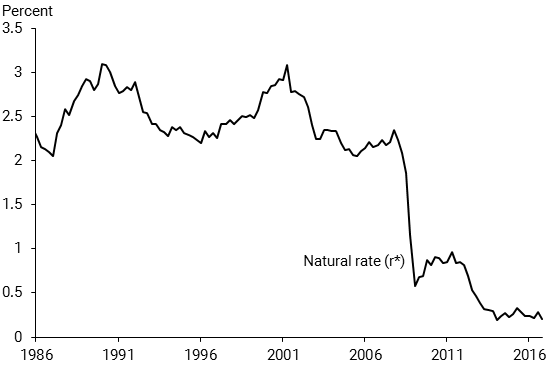

If you look at natural interest rates across the globe, you’ll find something they have in common: In country after country they’re at historic lows. What’s more, they appear poised to stay that way as trends pushing the natural rate lower are unlikely to reverse anytime soon (see Williams 2015, Hamilton et al. 2015, Kiley 2015, Lubik and Matthes 2015, and Laubach and Williams 2016). To put this in perspective, the weighted average of natural rates in Canada, the United Kingdom, the United States, and the euro area currently stands around ¼%. That’s more than 2 percentage points below the average natural rate that prevailed in the two decades before the financial crisis (Figure 4) (Holston, Laubach, and Williams 2016).

Figure 4

Estimates of r-star

Note: GDP-weighted average of United States, Canada, United Kingdom, and the euro area; weights are GDP at purchasing power parity, OECD estimates. Prior to 1995, euro-area weights are summed weights of the 11 original euro-area countries.

Source: Estimates from Holston, Laubach, and Williams (2016).

Why is price-level targeting well adapted to a low r-star world? If price growth is a little lower than target, say, during a downturn, the central bank aims to get the price level back up in the years ahead—and vice-versa. Baked into its very design is a “lower for longer” policy prescription in response to sustained low inflation (Reifschneider and Williams 2000, Eggertsson and Woodford 2003). This helps support the return of the price level to the desired level and anchor inflation expectations even when interest rates are constrained at the lower bound (see Koenig 2013 and Sheedy 2014 for further benefits).

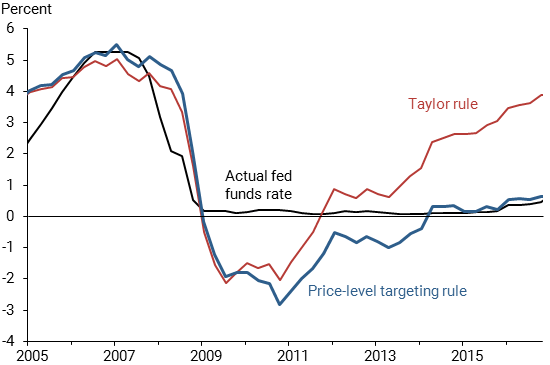

This aspect of price-level targeting can be seen by comparing the prescriptions of a standard Taylor (1993) rule to one adapted to a price-level framework. Figure 5 shows the prescriptions for these two policy strategies for the years 2005–2016, where 2005 is chosen as a starting point because this is generally viewed as a year that the economy was close to its goals in terms of inflation and the unemployment rate. For these calculations, inflation is measured by the four-quarter percent change in the core personal consumption expenditures price index, and economic activity is measured by the unemployment rate. For both rules, the coefficient on the unemployment gap is set equal to –1.For comparison, the actual federal funds rate is shown by the black line.

Figure 5

Prescriptions from alternative policy strategies

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Federal Reserve Board, and Federal Reserve Bank of San Francisco staff calculations.

Under this price-level strategy, the federal funds rate responds one-for-one with movements in: the inflation rate, the percent deviation of the price level from the target level, and the negative of the percentage point deviation of the unemployment rate from its natural rate. For these calculations, I have assumed a constant natural rate of interest of 2% and a constant natural rate of unemployment of 5%, consistent with standard views on these natural rates at the start of this sample.

What stands out in this figure is how close the prescriptions of these two policy strategies are to each other before and during the recession. They only differ in a meaningful way during the economic recovery after years of inflation consistently running below target. The buildup of one-sided misses below the inflation goal causes the price-level strategy to keep rates low despite the improvement in the unemployment rate and the gradual movement of inflation back towards 2%.

Price-level targeting and accessibility and accountability

So there are clear benefits to this framework when it comes to adaptability. How about accessibility and accountability?

In terms of accessibility, a price-level goal is easy to explain and is in some ways a more natural way for the public to think of price stability than an inflation target. A price-level target provides greater clarity on where prices will be 5, 10, and 30 years into the future, time horizons that people think about when buying a car, a home, or planning for retirement. This should lend itself to greater transparency and clarity for the public—especially when interest rates are constrained by the lower bound.

The same logic holds true for accountability. A price-level regime would provide a clear and accessible metric by which to judge whether the central bank is successfully delivering on its price stability mandate by looking at whether the price level is near its stipulated goal.

And as the examples I discussed attest, this is not a “dove” or “hawk” issue: a flexible price-level framework is well suited for achieving both price stability and employment goals. In the 1960s and early 1970s, a price-level framework would have called for tighter monetary policy, and thereby avoided the stagflation of the late 1970s. In recent years, it called for easier monetary policy than a standard Taylor rule.

Conclusion

I have highlighted some key potential advantages of a price-level framework over inflation targeting. By the way, some of these are shared by the related approach of nominal GDP targeting, an approach that is also worthy of further detailed study and consideration.

It’s important to note that there are potential drawbacks to a price-level framework as well. For one, it is only likely to succeed in the ways that I have described if it is followed consistently over time and well understood by the public (Williams 2006). This is not a short-run “fix” for the low r-star problem, but rather a long-term solution that will take many years to have full effect. Second, it may not be sufficient to deal with a very low r-star world without other complementary policy actions, whether in fiscal or monetary policy.

The likelihood that r-star will remain low for the foreseeable future is one of the reasons I’m convinced that we need to assess the pros and cons of alternative frameworks and strategies … because our menu of options looks something like this:

- We can hope that another storm doesn’t come;

- We can hope that our existing toolkit, perhaps extended to include negative interest rates, is up to the task;

- We can brace ourselves for a new normal where recessions last longer and run deeper, recoveries are slower, and we risk losing the nominal anchor;

- Or we can prepare for the next storm by taking appropriate actions in advance to commit to a more resilient framework; a framework that maintains our commitment to price stability and maximum employment; anchors inflation expectations; and has all the advantages of the current regime.

It’s better to study and debate these issues now, when we’ve attained recovery, than to wait for the next downturn or crisis to hit. I don’t know about you, but I’d far prefer to prepare for the next storm while we’re in calm waters, than to wait until our boats are taking on water.

I’ll finish where I started by emphasizing the need for monetary policy strategies that will make us resilient and effective in the years ahead: Adaptable. Accessible. Accountable.

Under these criteria–and given the realities of the low r-star world in which we live—I believe that a price-level framework merits very serious consideration for central banks including the Fed.

John C. Williams is president and chief executive officer of the Federal Reserve Bank of San Francisco.

References

Ball, Laurence. 2014. “The Case for a Long-Run Inflation Target of Four Percent.” IMF Working Paper 14/92, June.

Bernanke, Ben S. 2016. “Modifying the Fed’s Policy Framework: Does a Higher Inflation Target Beat Negative Interest Rates?” Ben Bernanke’s Blog, Brookings, September 13.

Blanchard, Olivier, Giovanni Dell’Ariccia and Paolo Mauro. 2010. “Rethinking Macroeconomic Policy.” Journal of Money, Credit, and Banking 42(s1), pp.199–215.

Eggertsson, Gauti, and Michael Woodford. 2003. “The Zero Bound on Interest Rates and Optimal Monetary Policy.” Brookings Papers on Economic Activity 2003(1), pp. 139–211.

Hamilton, James D., Ethan S. Harris, Jan Hatzius, and Kenneth D. West. 2015. “The Equilibrium Real Funds Rate: Past, Present, and Future.” Working paper, Hutchins Center on Fiscal and Monetary Policy at Brookings, October.

Holston, Kathryn, Thomas Laubach, and John C. Williams. 2016. “Measuring the Natural Rate of Interest: International Trends and Determinants.” FRB San Francisco Working Paper 2016-11, December. Estimates available.

Kiley, Michael T. 2015. “What Can the Data Tell Us About the Equilibrium Real Interest Rate?” Finance and Economics Discussion Series 2015-077, Board of Governors of the Federal Reserve System.

Kiley, Michael T., and John M. Roberts. 2017. “Monetary Policy in a Low Interest Rate World.” Brookings Papers on Economic Activity, Spring, forthcoming.

Koenig, Evan F. 2013. “Like a Good Neighbor: Monetary Policy, Financial Stability, and the Distribution of Risk.” International Journal of Central Banking 9(2, June), pp. 57–82.

Laubach, Thomas, and John C. Williams. 2016. “Measuring the Natural Rate of Interest Redux.” Business Economics 51(2, July), pp. 57–67.

Lubik, Thomas A., and Christian Matthes. 2015. “Calculating the Natural Rate of Interest: A Comparison of Two Alternative Approaches.” FRB Richmond Economic Brief 15-10 (October).

Orphanides, Athanasios, and John C. Williams. 2002. “Robust Monetary Policy Rules with Unknown Natural Rates.” Brookings Papers on Economic Activity 2002(2), pp. 63–145.

Orphanides, Athanasios, and John C. Williams. 2007. “Robust Monetary Policy with Imperfect Knowledge.” Journal of Monetary Economics 54 (August), pp. 1,406–1,435.

Orphanides, Athanasios, and John C. Williams. 2013. “Monetary Policy Mistakes and the Evolution of Inflation Expectations.” In The Great Inflation: The Rebirth of Modern Central Banking, eds. Michael D. Bordo and Athanasios Orphanides. Chicago: University of Chicago Press.

Reifschneider, David. 2016. “Gauging the Ability of the FOMC to Respond to Future Recessions.” Finance and Economics Discussion Series 2016-068, Board of Governors of the Federal Reserve System.

Reifschneider, David, and John C. Williams. 2000. “Three Lessons for Monetary Policy in a Low Inflation Era.” Journal of Money, Credit, and Banking 32(4, November), pp. 936–966.

Sheedy, Kevin D. 2014. “Debt and Incomplete Financial Markets: A Case for Nominal GDP Targeting.” Brookings Papers on Economic Activity, Spring, pp. 301–361.

Taylor, John B. 1993. “Discretion vs. Policy Rules in Practice.” Carnegie-Rochester Conference Series on Public Policy 39, pp. 195–214.

Williams, John C. 2006. “Monetary Policy in a Low Inflation Economy with Learning.” In Monetary Policy in an Environment of Low Inflation, Conference Proceedings, Bank of Korea International Conference 2006. Seoul, Korea: The Bank of Korea, 2006, pp. 199–228. Reprinted in FRB San Francisco Economic Review 2010.

Williams, John C. 2009. “Heeding Daedalus: Optimal Inflation and the Zero Bound.” Brookings Papers on Economic Activity 2009(2), pp. 1–37.

Williams, John C. 2015. “The Decline in the Natural Rate of Interest.” Business Economics 50(2, April), pp. 57–60.

Williams, John C. 2016. “Monetary Policy in a Low R-star World.” FRBSF Economic Letter 2016-23 (August 15).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org