Daniel Wilson, research advisor at the Federal Reserve Bank of San Francisco, states his views on the current economy and the outlook.

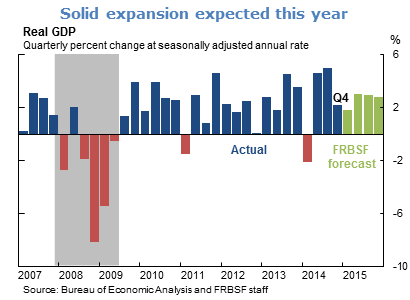

- Real GDP growth moderated somewhat in the fourth quarter of 2014 after exceptionally strong growth in the two prior quarters. This moderation was due primarily to a sharp drop in net exports as well as some weakness in government spending and business investment. Consumer spending, on the other hand, was quite strong in the fourth quarter.

- We expect a similar dynamic in the first quarter of 2015, with GDP growth being pushed up by strong consumer spending but pushed down by declining net exports. On top of that, the recent severe weather hitting the Midwest and East Coast likely reduced GDP growth by a few tenths in the first quarter. Some bounceback is expected in the second quarter as those weather effects reverse.

- We project above-trend economic growth for the rest of 2015 and the first half of 2016, fueled primarily by continued low interest rates and strong consumer spending, with the latter attributable to improved labor market conditions and lower gasoline prices. After the middle of this year, we expect a gradual decline toward our long-run trend growth rate of around 2% as interest rates start to rise, the boost from lower gas prices fades, and the negative effects of the stronger dollar persist into 2017.

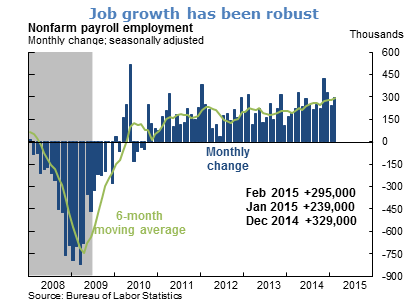

- Turning to the labor market, job growth has been robust, with monthly job gains averaging about 300,000 over the past six months.

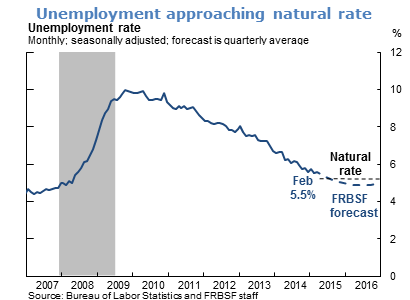

- Similarly, the unemployment rate has continued its gradual decline. We expect the unemployment rate to reach our estimate of the natural rate, which is 5.2%, by the middle of this year. After that, it is likely to undershoot the natural rate slightly, given above-trend GDP growth and very accommodative monetary policy.

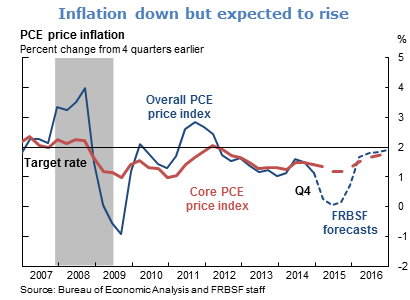

- Recent inflation data have softened further, but this was expected given the sharp drop in energy prices in the second half of 2014 and continuing through January. Lower import prices due to the recent dollar appreciation have also contributed to lower inflation. These disinflationary forces should dissipate by the middle of the year. After that, we expect inflation to gradually rise toward the Federal Open Market Committee’s 2% target over the next couple of years, especially as the labor market gets close to full strength and wage pressures build.

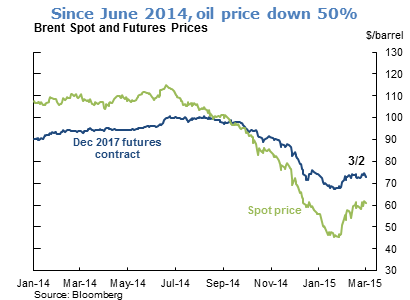

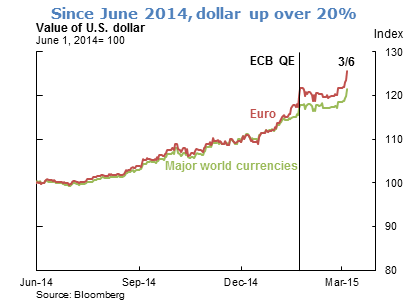

- Our outlook for both economic growth and inflation is influenced heavily by the dramatic recent movements in oil prices and the value of the dollar. Since June 2014, oil prices have fallen by roughly 50%. And, though we’ve seen oil prices bounce back a bit from their lows in recent weeks, prices of oil futures indicate that the market is expecting prices to remain low at least through 2017. Also, since June 2014, the “price” of the dollar has appreciated about 20% relative to major world currencies and about 25% relative to the euro.

- These two factors have worked in tandem to push down inflation via lower energy prices and lower prices for imported goods and services. But they have countervailing—and longer lasting—effects on economic growth. The dollar appreciation makes U.S. exports more expensive to foreigners and imports cheaper for domestic buyers, holding down domestic growth. Similarly, lower oil prices hurt domestic oil producers. However, because the United States is a net importer of oil, this negative effect on U.S. economic growth is dominated by the positive effects from lower energy costs for domestic businesses and higher spending by consumers whose overall purchasing power is increased by lower gas prices.

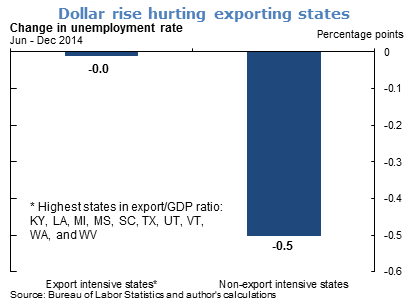

- One way to see the negative effects of the dollar appreciation and lower net exports is to compare the recent economic fortunes of export-intensive states with other states. The 10 states with the highest export shares show no change in average unemployment from June to December 2014. By comparison, for all other states the average unemployment rate fell by half a percentage point over the same period.

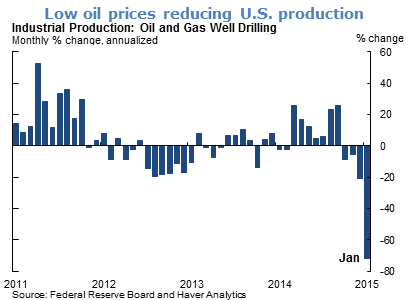

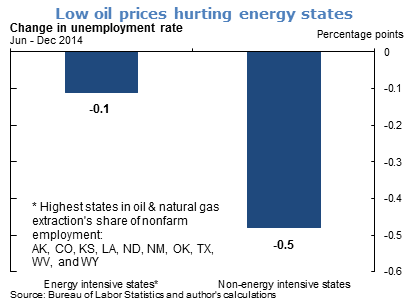

- Similarly, the negative effects of declining oil prices on the domestic oil extraction industry have been felt much more in some states than in others. The price declines have led to a big drop in drilling activity in states with a sizable oil extraction industry. The average unemployment rate for the 10 states with the highest employment shares in oil and natural gas extraction fell by only one-tenth of a percentage point from June to December. By comparison, the average unemployment rate among all other states fell half a percentage point over this period.

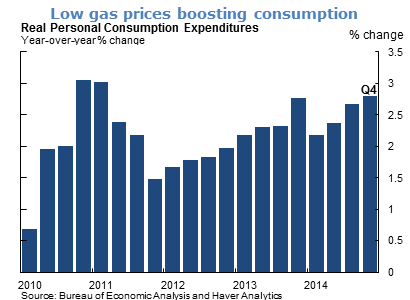

- Despite these negatives for some states, lower oil prices also mean cheaper gasoline for consumers throughout the nation. This is part of the reason that growth in personal consumption expenditures was quite strong in the second half of 2014.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.