Download PDF (pdf, 639 kb)

The Federal Reserve conducted a follow-up Diary of Consumer Payment Choice in 2016. Read the FedNotes paper on Understanding Consumer Cash Use: Preliminary Findings from the 2016 Diary of Consumer Payment Choice.

Executive Summary

As the payments landscape evolves, cash remains a unique, resilient, and heavily used consumer payment instrument. Still, with new payment options and ways to shop, consumers are adapting how they view and use cash. The Diary of Consumer Payment Choice (Diary) serves as the Cash Product Office’s (CPO) primary data source on consumer payment behavior. Insights from the Diary, and other data sources, help the CPO understand the role that cash will play in the future. This research helps the Federal Reserve (Fed) fulfill its objectives of maintaining confidence in U.S. currency and promoting a safe and efficient payment system.

When first conducted in 2012, the Diary showed that cash was the most frequently used payment instrument and that cash use was prevalent across all demographic groups. The key findings of the 2015 Diary of Consumer Payment Choice are similar and suggest that:

- Cash continues to be the most frequently used consumer payment instrument

- Cash is widely used in a variety of circumstances

- Cash dominates small-value transactions

- The average value of cash holdings has grown

The 2015 results also show that cash is facing competition from other payment instruments. In 2015, 32 percent of consumer transactions were made with cash, compared with 40 percent in 2012. Growing consumer comfort with payment cards and the growth of online commerce, among other factors, contribute to this trend. Nonetheless, a broad range of results suggests that cash remains resilient and continues to play a key and unique role for consumers.

The first section of the paper discusses high-level, aggregate trends in cash demand and in financial institutions’ currency orders and deposits with the Fed. The second section focuses on four findings about cash use from the 2015 Diary, outlined above. The final section explores three insights that the 2015 data give us on consumer payment preferences and practices.

Background: High-level Trends Suggest Cash Use is Evolving

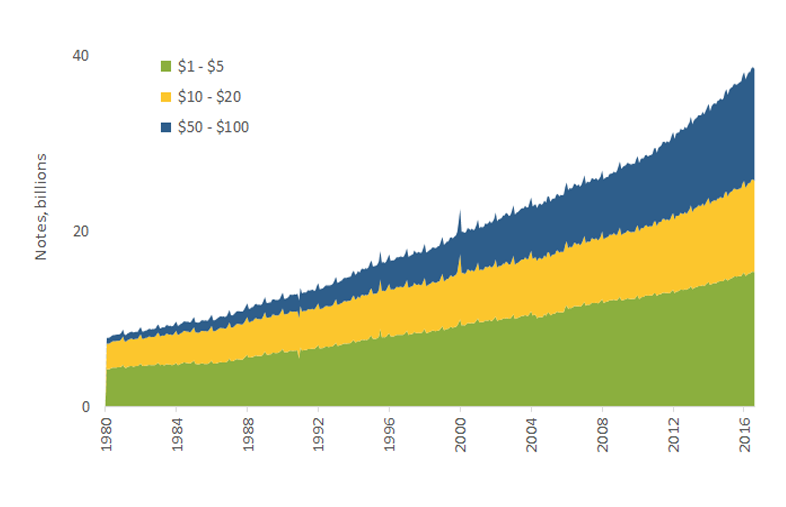

Despite innovations in smartphone technology and mobile payment apps, Fed data on the amount of currency in circulation suggest that demand for cash is strong. Figure 1 shows currency in circulation from January 1980 to August 2016 and includes notes held by merchants, financial institutions, and consumers. The amount of currency in circulation has increased steadily over time, and demand for higher denominations has accelerated in the years since the 2008 financial crisis.

Figure 1: Currency in Circulation

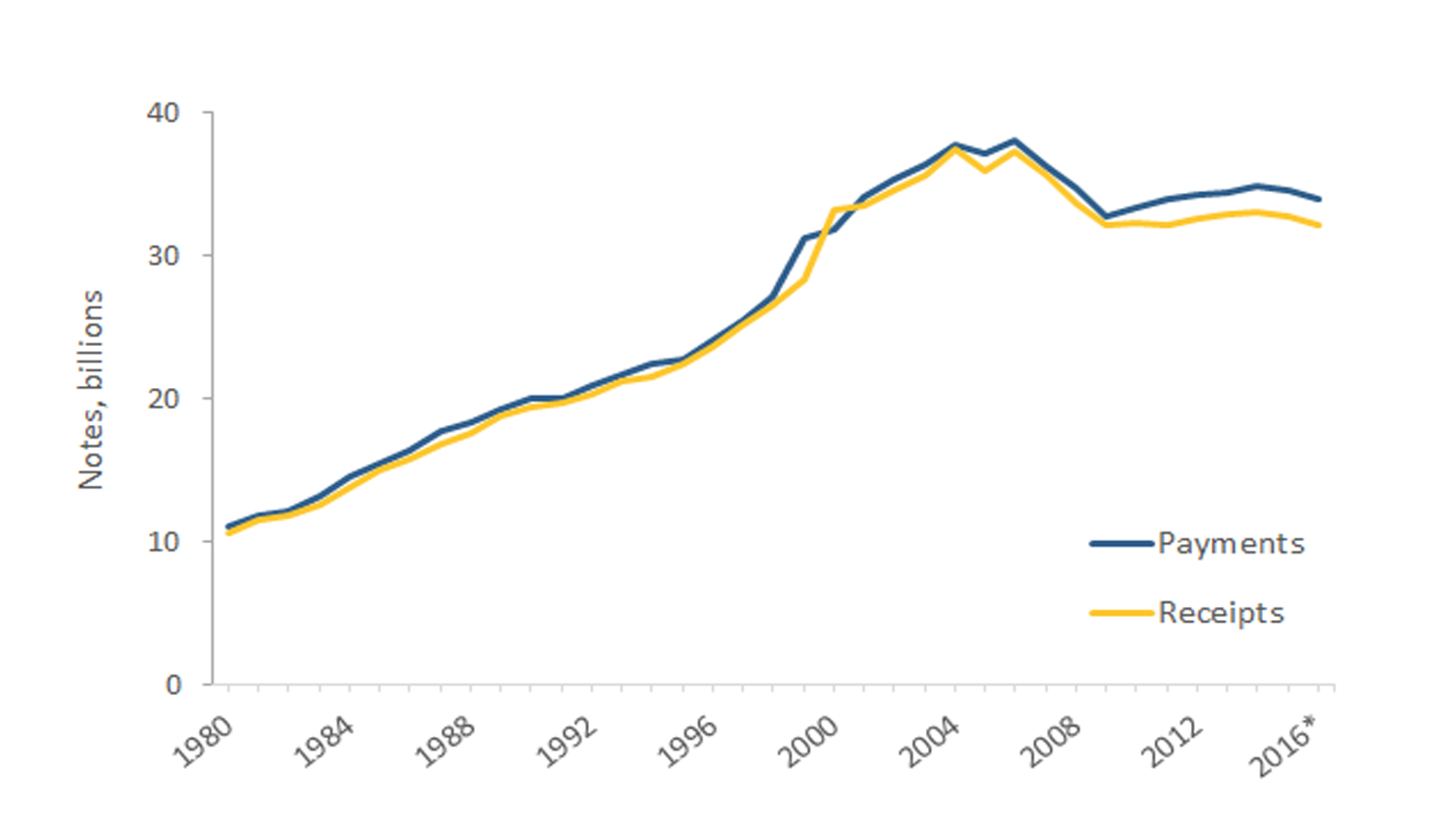

This steady growth in cash demand contrasts with the moderation the Federal Reserve is seeing in its payments to and receipts from depository institutions (Figure 2). Fed payments and receipts grew modestly after the implementation of the 2006 Recirculation Policy and have declined slightly since 2014. Concurrently, the gap between payments and receipts has grown since 2009, contributing to the more rapid growth in currency in circulation over this period.

Figure 2: Annual Total Reserve Bank Payments and Receipts

Taken together, these two perspectives suggest a potential change in how consumers, businesses, and financial institutions are using and handling cash. The moderation and slight decline in Fed receipts could mean, among other explanations, that consumers are using cash less frequently to pay for purchases. At the same time, continued growth in currency in circulation may mean that, in a low-interest rate environment, consumers and merchants are comfortable holding more cash, possibly for contingency purposes.

The Diary data offer more detailed insights into how consumers are using cash and how their behavior may contribute to the trends discussed above.

Key Findings from the 2015 Diary of Consumer Payment Choice

Finding 1: Cash is the most frequently used retail payment instrument

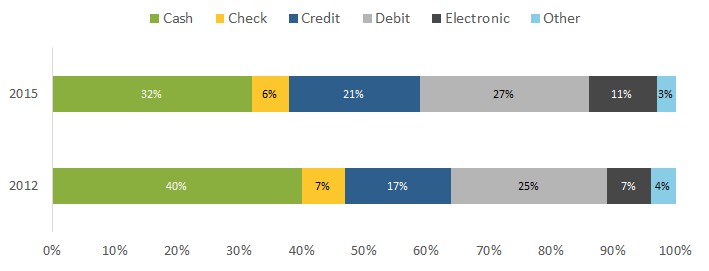

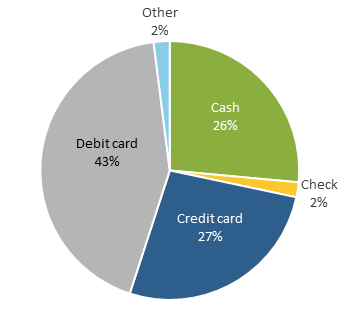

In 2015, cash remained the most frequently used retail payment instrument, used in nearly one-third (32 percent) of all transactions, including bill payments (Figure 3). Consumers used debit cards for 27 percent of their transactions, followed by credit cards for 21 percent of transactions. Electronic payments (e.g. ACH transfers and online bill pay) and checks comprised a small share of transaction volume, though the value of these payments tended to be higher than cash, debit, or credit payments.

Figure 3: Share of Transaction Number by Payment Instrument

Compared to 2012, cash’s share of transactions in 2015 declined approximately eight percentage points, from 40 percent to 32 percent. Consumer use of debit and credit cards increased two and four percentage points, respectively, and account for 48 percent of all reported transactions in the 2015 data.

Cash’s decline in transaction share can be attributed to two types of factors: (1) fundamental changes in consumer behavior and preferences and (2) structural changes to the Diary survey tool.

Fundamentally, consumer preferences and shopping behavior appear to have changed as consumers increasingly use non-cash payment instruments. Fewer people cited cash as their preferred payment instrument (see Insight 1 below), and consumers are increasing the amount of shopping they do online or through remote platforms. The share of transactions that took place online or remotely increased to 10 percent in 2015, up from 6 percent in 2012.

Structurally, changes to the survey instrument and a different panel of diarists may have contributed to part of the change in cash’s share of transactions in 2015. The addition of a bill payment module at the end of the third Diary day provided a more accurate record of bill payments, increasing the share of reported electronic payments. The 2015 Diary participants also recorded fewer small-value transactions.1 As cash tends to be used for small-value transactions, the lower number of reported small-value transactions disproportionately diminished cash’s share of total transactions. Appendix I provides more information on changes between the 2012 and 2015 Diaries.

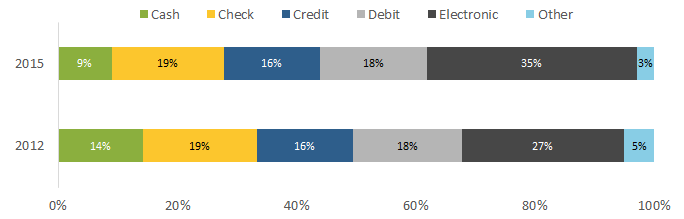

Figure 42 looks at each payment instrument’s share of total payment value and further demonstrates the impact of the 2015 Diary’s changes in small-value transactions and bill payments. Cash, and its concentrated use for small-value transactions, accounted for 9 percent of total payment value. Credit and debit cards, combined, accounted for 34 percent of the total value spent, while electronic payments made up 35 percent.

Figure 4: Share of Value by Payment Instrument

Cash’s share of total payment value decreased five percentage points, while check, credit cards, and debit cards remained the same, and electronic payments’ share increased eight percentage points. The data show that cash and electronic payments can be thought to have opposite consumer uses: cash is used most often for small-value purchases, while electronic payments are used less frequently, but primarily for large-value purchases and bill payments.

Finding 2: Cash is widely used, even when other options are available

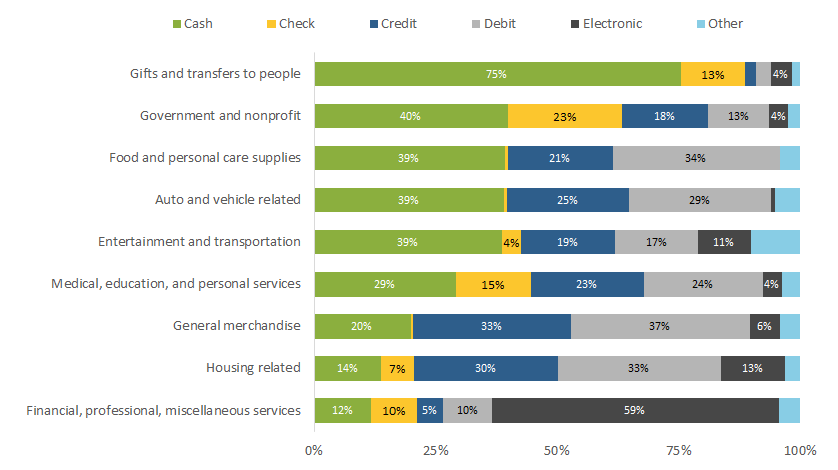

Despite its decline in share of reported transactions, cash was used for a variety of merchant categories, even when other payment options were available. Figure 5 shows the different payment instruments used for various spending categories and shows that cash is the most used payment instrument in six of nine merchant categories. Gifts and transfers to people, where cash was used for 75 percent of transactions, was the category with the highest share of cash transactions. Other cash-intensive categories included government and nonprofit purchases (40 percent), food and personal care supplies (39 percent), and auto- and vehicle-related purchases (39 percent). Merchant categories where cash is used less than 20 percent of the time were housing-related purchases and financial, professional, miscellaneous services. These categories traditionally involve larger transactions that are paid with non-cash instruments.

Figure 5: Payment Instrument Use by Spending Category

As with the 2012 Diary, cash remains the most or the second most used payment instrument in a majority of merchant categories. However, cash’s share of transactions within each category was quite different between 2012 and 2015. For example, cash’s share within gifts and transfers to people, housing-related, and auto- and vehicle-related purchases increased eight, six, and five percentage points, respectively. Even with the availability of peer-to-peer (P2P) money transfer apps like Venmo and PayPal, cash continues to be the most popular choice for P2P payments. In contrast, cash use declined for food and personal care supplies and general merchandise by 12 and nine percentage points, respectively, which reflects in part the decline in the reported number of small-value transactions.

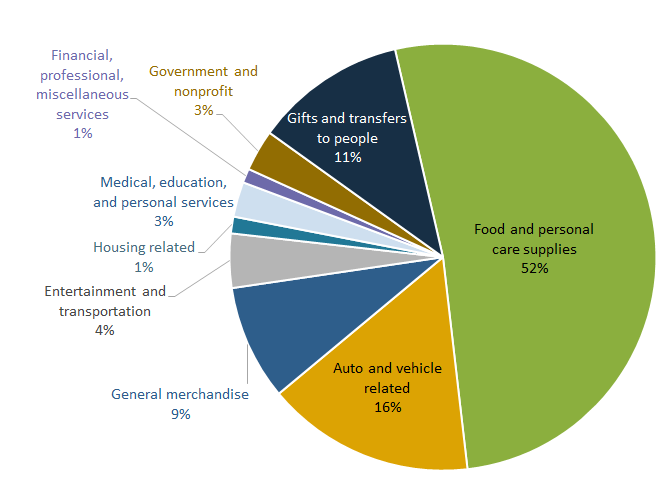

Figure 6 shows the 2015 Diary’s cash transactions and the various merchant categories into which they fell. Food and personal care supplies, auto- and vehicle-related, general merchandise, and gifts and transfers to people comprised nearly 90 percent of cash transactions. Together, the data from Figures 5 and 6 highlight an important point: a merchant category may have high cash use, but that category may make up only a small share of total cash transactions. Using gifts and transfers to people as an example, while 75 percent of P2P transactions were made in cash, only 11 percent of cash transactions were used for P2P payments. Therefore, changes in cash use for a cash-intensive category like food and personal care supplies yield a greater impact on total cash transactions, compared to similar changes in less cash-intensive categories.

Figure 6: Cash Spending Categories

Finding 3: Cash dominates small-value payments

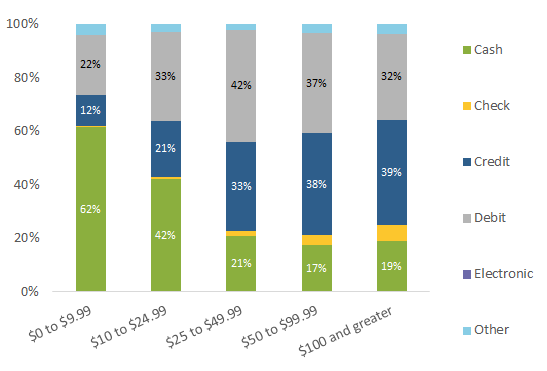

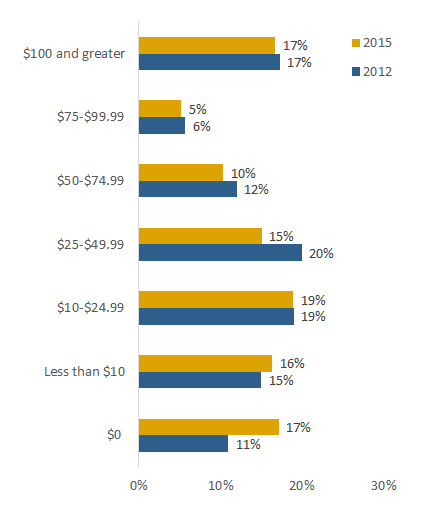

In 2015, cash continued to dominate small-value transactions, with cash being used for more than 50 percent of transactions under $25. As shown in Figure 7, cash was used for more than 60 percent of purchases under $10. For purchases between $10 and $24.99, cash was used 42 percent of the time. Between 2012 and 2015, the share of cash transactions under $10 fell five percentage points and cash’s share of purchases ranging $10 to $24.99 declined seven percentage points. Nonetheless, overall cash use for small-value transactions remains high.

Figure 7: Payment Instrument by Amount, In-Store 2015

One potential explanation for cash’s large share of small-value transactions is that merchants either do not accept debit or credit cards, or they require a minimum purchase to accept cards. However, the 2015 Diary found little evidence that small-value cash transactions were driven by a lack of merchant card acceptance or merchant-imposed transaction minimums for card use. The findings suggest that consumers are using cash for small-value transactions out of convenience, not merchant-specific pressures (see box below).

Most in-store transactions (63 percent) fall into the under $25 value range. The large share of purchases in this price range, combined with consumers’ propensity to use cash for purchases in this price range, explains why cash is still the most frequently used payment instrument. However, if merchants increase their online presence and consumers shift shopping activity to electronic and mobile channels, cash’s share of transactions—including small-value transactions—could decline.

Card acceptance and minimums had little impact on cash use for small-value transactions

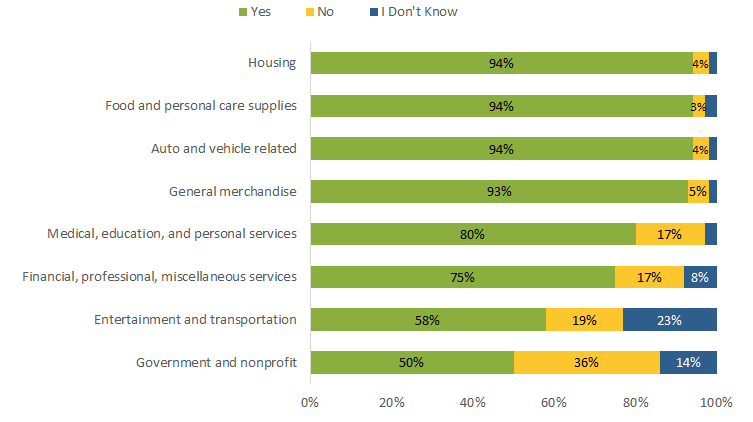

For each recorded transaction, Diary participants recorded whether the merchant accepted payment cards and, if so, whether there was a minimum purchase required to use a card. Figure 8 shows participants’ responses by merchant category.

Figure 8: Card Acceptance Rate by Merchant Type

Card acceptance was high among most merchants, even those in traditionally cash-intensive sectors like food and personal care supplies. This high level of card acceptance comes as innovations like card readers and QR scanners gain popularity. Despite high levels of card acceptance, consumers continue to use cash for small-value transactions.

The 2015 Diary also asked participants whether merchants required a minimum purchase before accepting a payment card. Most participants either did not encounter a minimum purchase requirement or did not know whether a minimum purchase was required, suggesting that the presence or absence of a minimum was not an issue for that transaction. In all spending categories, 89 percent or more of transactions took place without requiring a minimum. Even for small-value transactions, required minimums did not appear to drive cash use.

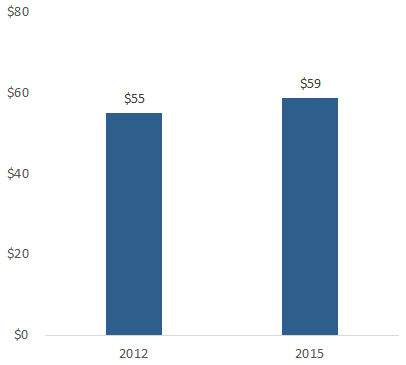

Finding 4: Average value of consumer cash holdings increased slightly

The majority of U.S. consumers continue to carry cash. Nearly 83 percent of diarists held cash at the end of at least one day of the Diary reporting period, and 69 percent held cash at the end of all three days. The average amount of cash that diarists held each day increased from $55 to $59 between 2012 and 2015 (Figure 9).

Figure 9: Average Cash Holding

Though consumers’ average cash holding increased, the median value declined from $29 to $21 between 2012 and 2015. The divergence between the median and average values indicates that some participants above the median held substantially more cash in 2015 than in 2012. More than half (52 percent) of participants held less than $25 on average in 2015, compared to 45 percent in 2012 (Figure 10).

Figure 10: Average Cash Holding Amount

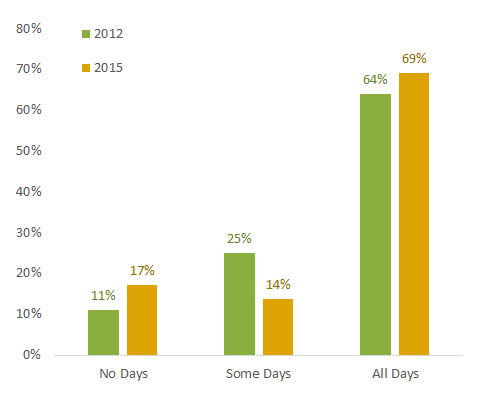

Consumers also appear to be changing how frequently they hold cash (Figure 11). During the Diary reporting period, most diarists moved to one of two extremes, either ending all three days holding some cash or ending all three days holding zero cash. A larger share (17 percent) did not hold cash during their 2015 Diary period, compared to 11 percent in 2012. Similarly, a larger share (69 percent) ended all three days of the Diary with cash, up from 64 percent in 2012.

Figure 11: Cash Holding Frequency

Diary participants’ movement toward the extremes suggests that consumers’ relationship with cash is evolving. They are either no longer holding cash, or they are holding it more frequently and in larger amounts. These habits may suggest that, for those who continue to hold cash, its function as a backup payment option is gaining traction. For those holding less cash or not holding it at all, cash’s role as a transactional payment instrument has diminished; for these consumers, cash’s usefulness as a back-up instrument may not be compelling enough to carry it.

Insights on Consumers and Consumer Preference

Insight 1: Consumers’ stated preferences influence how they pay

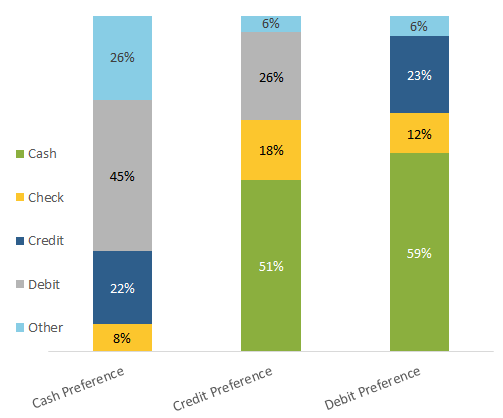

The 2015 Diary asked which payment instrument each participant preferred to use for non-bill purchases, bill payments, and online payments. For non-bill purchases, 43 percent of diarists cited debit cards as their preferred payment instrument. For the remainder of participants, the shares of people citing credit cards and cash were roughly even, at 27 percent and 26 percent, respectively (Figure 12).

Figure 12: Primary Payment Preferences

Compared to the 2012 Diary, the 2015 Diary showed changing consumer payment preferences. In both years, debit cards were cited as the most popular payment instrument. However, in 2015, the share of participants preferring credit cards increased five percentage points, while cash’s share declined by four percentage points from 2012. As credit availability and economic conditions have improved since the financial crisis, consumer preferences appear to have shifted somewhat from cash to credit cards.

While the majority of consumers prefer cards, cash remains the most preferred backup payment instrument. When asked what payment instrument they preferred if their primary option was unavailable, 55 percent of people who prefer checks, debit cards, or credit cards chose cash (Figure 13).

Figure 13: Backup Payment Preferences

Insight 2: Consumers who prefer and use cash are a diverse group

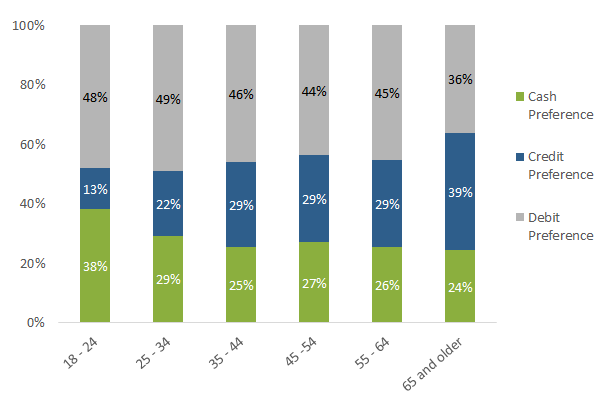

Contrary to conventional wisdom, consumers who prefer and use cash are a diverse group. When it comes to age, the Diary shows that many younger consumers are actually cash “lovers.”3 Although the share of people preferring cash declined across all age groups between the 2012 and 2015 Diaries, those in the 18 to 24 years category included the largest share of people who prefer cash, at 38 percent (Figure 14). Nearly a quarter of every other age group selected cash as their primary preference.

Figure 14: Primary Payment Preference by Age

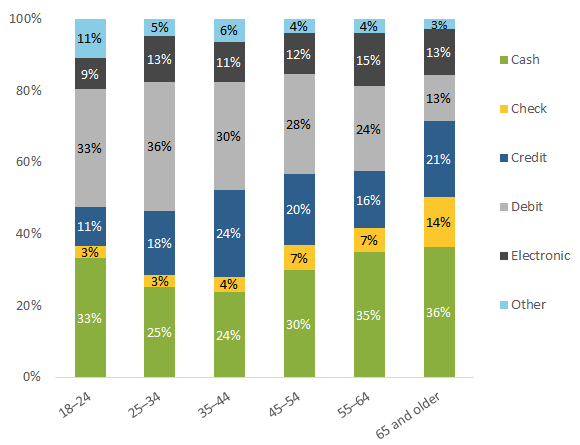

This age-agnostic pattern carries over to cash use as well (Figure 15). Consumers 65 and older made the most cash transactions, averaging 36 percent of their total monthly transactions. Every age group made more cash transactions than credit card transactions, and cash transactions continued to comprise at least 24 percent of each age group’s total reported transactions. Comparing 2012 to 2015, however, cash use dropped the most for participants between 35-44 years, who had the smallest share of transactions made with cash. This group saw a decrease in their number of cash transactions, with cash’s share falling from 40 percent in 2012 to 24 percent in 2015.

Figure 15: Payment Instrument Use by Age

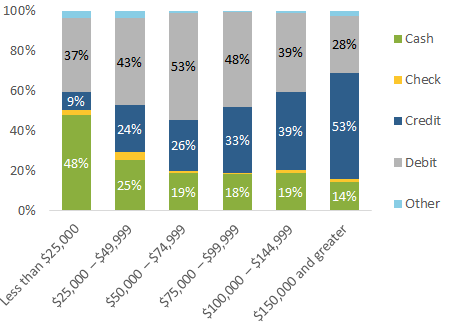

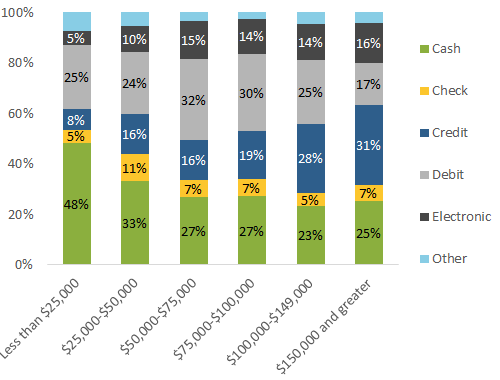

Income has a strong influence on payment preference (Figure 16), but not on cash use (Figure 17). Households earning less than $25,000 annually have a particularly strong cash preference, with 48 percent preferring cash, down from 55 percent in the 2012 Diary. Households earning greater than $75,000 annually saw a two to three percentage point increase in cash preference, though households earning $150,000 and greater continued to exhibit the smallest cash preference at 14 percent.

Figure 16: Primary Payment Preference by Income

Figure 17: Payment Instrument Use by Income

Despite their stated preferences, in 2015, nearly everyone uses cash. As in 2012, all income groups made roughly the same number of monthly cash transactions in 2015 (approximately 15 transactions per month). However, households with greater incomes made more transactions overall, and as a result, made a smaller share of their total transactions in cash.

People who use cash are not limited to specific demographic groups. Even if consumers cite a preference for cards, many continue to make cash purchases, and cash spending occurs across all demographic groups.

Insight 3: Consumer cash holdings vary by demographics

The 2015 Diary showed that consumers tend to hold cash regardless of their payment preferences. However, age and income have some influence on how much cash consumers hold.

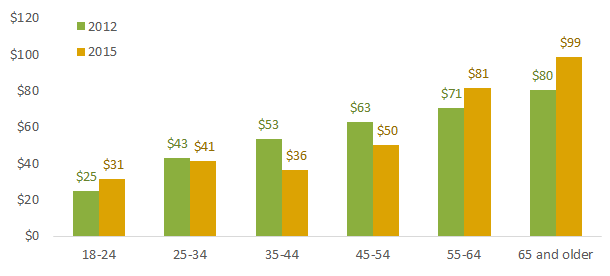

Average cash holdings tend to increase with age (Figure 18). The 65 and older age group held the highest amount of cash, averaging $99 each day, an increase from the $80 average held in 2012. At the other end of the spectrum, consumers 18-24 years held the least cash, though they increased their average holdings, from $25 in 2012 to $31 in 2015. The biggest decrease in cash holdings was seen in the 35-44 years age group, which decreased their average holding from $53 to $36 between 2012 and 2015.

Figure 18: Average Cash Holdings by Age

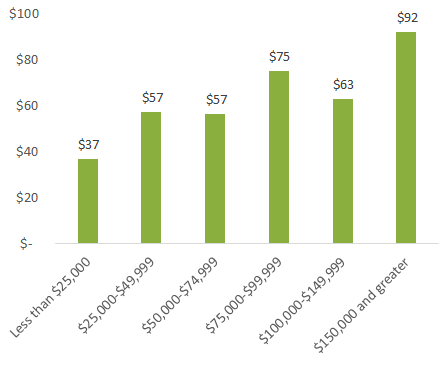

Income plays a role in cash holdings as well (Figure 19). In 2012, participants in higher income households held greater amounts of cash. In 2015, this pattern continued, though the disparity across income groups is less stark. Households earning less than $25,000 held the smallest average amount of cash at $37, a decrease from the $49 they held in 2012. Households earning $150,000 and greater held the highest amount, holding an average of $92 per day. Households earning between $25,000 and $150,000 held roughly similar amounts on average, between $57 and $75 per day.

Figure 19: 2015 Average Cash Holdings by Household Income

Conclusion

The 2015 Diary results suggest that cash remains a highly valued and useful payment instrument. Cash is still the most frequently used payment instrument. A wide variety of people prefer cash, and even those who prefer another payment instrument still use cash frequently. Cash is often favored for its convenience, particularly for specific use cases such as P2P transfers and small-value transactions.

Cash’s declining share of total payments is indicative of the growth of non-cash payment instruments and new ways to shop online or remotely.4 While cash’s share may be declining, continuing growth in currency in circulation points to cash’s significance in the economy.

The Federal Reserve Banks of Boston, Richmond and San Francisco will continue to field the Diary of Consumer Payment Choice in the future.These and other studies will provide ongoing insight into cash’s role in the economy, and will inform the CPO’s operations and long-term strategic planning.

The views in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Federal Reserve System.

About the Diary of Consumer Payment Choice

The Diary of Consumer Payment Choice is a survey designed to study the purchase and payment behavior of U.S. consumers. The study is conducted using a nationally representative sample of U.S. consumers. The second fielding of the Diary of Consumer Payment Choice (Diary) took place from October 16 to December 15, 2015. Participants were asked to record information on all transactions—purchases, bill payments, deposits, withdrawals, etc.—conducted during an assigned consecutive three-day period.

The 2015 Diary is the second iteration of a research initiative by the Federal Reserve Banks of Boston, Richmond, and San Francisco. The initial Diary, conducted in 2012, found that cash was a valuable payment instrument for a significant portion of consumers and businesses. In the 2012 study, consumers used cash more frequently than any other payment instrument, and cash played a dominant role for small-value transactions and for key demographic groups like lower-income consumers.

About the Cash Product Office

As the nation’s central bank, the Federal Reserve ensures that cash is available when and where it is needed, including in times of crisis and business disruption, by providing FedCash® Services to depository institutions and, through them, to the general public. In fulfilling this role, the Fed’s primary responsibility is to maintain public confidence in the integrity and availability of U.S. currency.

The Federal Reserve System’s Cash Product Office (CPO) provides strategic leadership for this key function by formulating and implementing service level policies, operational guidance, and technology strategies for U.S. currency and coin services provided by Federal Reserve Banks nationally and internationally. In addition to guiding policies and procedures, the CPO establishes budget guidance for FedCash® Services, provides support for Federal Reserve currency and coin inventory management, and supports business continuity planning at the supply chain level. It also conducts market research and works directly with financial institutions and retailers to analyze trends in cash use.

Appendix I

Changes to the 2015 Diary of Consumer Payment Choice Structure

For both the 2012 and 2015 Diaries, participants tracked all transactions (deposits, withdrawals, purchases, bills, etc.) for an assigned, consecutive three-day period within the observation window. In 2012, the observation window was the month of October. The 2015 Diary expanded the observation window to two months, from October 16 to December 15. This extended timeframe allowed researchers to observe payment choice and purchase behavior through part of the 2015 holiday season.

Approximately 2,500 participants completed the 2012 Diary. Slightly fewer than 1,500 participated in 2015. To increase the number of observations for the 2015 Diary, 500 of the 1,500 participants took the Diary a second time, approximately one month after their initial completion. This repeat participation had the benefit of allowing researchers to assess whether individuals changed their behavior during the holiday season.

Other additions to the 2015 Diary included:

- A separate bill payment module at the end of a diarist’s third day to improve bill payment records during the observed diary period

- Follow-up questions regarding card acceptance to determine whether individuals were using cash for convenience or out of necessity

- Additional preference questions to allow participants to specify different payment preferences based on transaction value and on whether the purchase took place in-person or not

The 2015 Diary also revealed a marked change in the total number of transactions and small-value transactions when compared to the inaugural 2012 study. This reduction likely impacts small-value transactions that took place in-person and had a high probability of cash use. More information about this reduction can be found in the paper “Measures of Cash Use from a New Payments Diary” (forthcoming) by the Consumer Payment Research Center located at the Federal Reserve Bank of Boston.

Footnotes

1. See “Measures of Cash Use from a New Payments Diary” (forthcoming) by the Consumer Payment Research Center, located at the Federal Reserve Bank of Boston, on potential reasons why small-value transactions were lower.

2. Please note that some percentages in the following charts may not add to 100 due to rounding.

3. Bloomberg (August 2014). “Young Americans Hate Cash.”

4. Federal Reserve Bank of San Francisco. 26 April 2016. Shopping Experience Trends and their Impact on Cash.