Total factor productivity—a measure of the efficiency with which labor and capital are used—has fallen during the current recession. But, after adjustment for lower utilization of labor and capital, such productivity has risen strongly over the past two years. These growth–accounting measures suggest that efficiency gains have continued during the recession, boding well for long-term economic growth.

An important question facing policymakers is how much slack the economy has. One interpretation of the surge in inflation in the 1970s is that the Federal Reserve overestimated the level of potential output and, hence, thought the economy had a lot more slack than it actually did (Orphanides 2002).

This Economic Letter looks at potential output from the perspective of growth accounting, which assesses some of the key supply-side factors determining sustainable, noninflationary potential output. Perhaps most importantly, we find that the underlying pace of efficiency improvements—“technological progress,” broadly construed—has remained strong during the recession. This strength offers a reason for cautious optimism about potential output and the long-term health of the American economy. More immediately, stronger potential relative to the same observed output implies substantial slack in the economy.

Inputs, utilization, and total factor productivity

Growth accounting decomposes output growth into changes in inputs of labor and capital (buildings, computers, machine presses, etc.) and the efficiency with which these factors are combined. This method does not seek to explain why inputs change the way they do: Some changes might be warranted, efficient responses to the shocks hitting the economy. But, as we discuss, growth accounting can still shed light on whether a decline in potential output explains any of the drop in actual output during the recession.

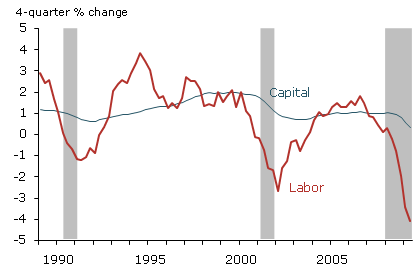

Figure 1

Contribution of capital and labor to growth

Source: Fernald 2009.

Note: Contribution is factor input growth times share of income.

As Figure 1 shows, labor input has plunged in this recession (see data). Labor input comprises both hours worked and changes in labor quality, a measure that captures such observable dimensions as experience and education. In addition to weak aggregate demand, another reason labor input may have fallen—as unemployment surged from 4.5% in early 2007 to 9.5% in June 2009—is the need to shift labor and capital away from construction and finance. It takes time for workers to find new jobs in other sectors, which raises unemployment. However, Valletta and Cleary (2008) suggest that these reallocations on their own might temporarily increase the unemployment rate by perhaps a percentage point, indicating that other forces are almost surely at work.

The contribution of capital input to growth has also slowed noticeably. Nonresidential investment has fallen sharply and now barely covers depreciation of existing capital, implying that capital input will also grow little, if at all, for the next year or more. On its own, the weakness in growth of the economy’s productive capacity directly reduces potential output growth by about a percentage point compared with recent experience. But this does not mean that the level of potential output has actually fallen.

The economy’s productive potential depends not only on inputs, but also on the efficiency with which they are combined. In its simplest form, growth accounting measures efficiency growth as actual output growth less the contributions of capital and labor. This “total factor productivity” (TFP) residual captures anything that affects the relationship between measured inputs and output. Over long periods of time, TFP is driven primarily by innovation, knowledge, and efficiency—factors that raise the economy’s productive capacity.

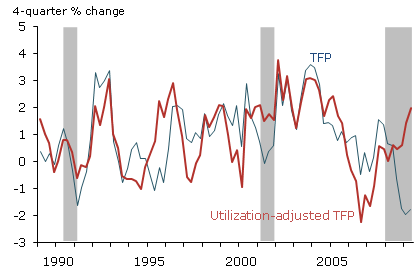

Figure 2

Two measures of total factor productivity

Source: Fernald 2009.

The thin line in Figure 2 shows that TFP growth has turned negative, as typically occurs in recessions. However, this does not mean that innovation has reversed or that the economy has become less efficient. Instead, a long-standing explanation attributes this fall in TFP during recessions to difficult-to-quantify variations in labor effort and intensity of capital use.

Firms, for example, may hesitate to fire skilled workers they will need once the economy recovers, because they will lose valuable firm-specific skills and knowledge. Instead, firms are likely to reduce overtime (which reduces measured labor input) and also, less obviously, the required effort of each worker (which is difficult to measure). At the same time that firms vary the intensity with which they use labor, they are also likely to vary capital utilization—that is, the intensity with which machinery and structures are used, most obviously the number of hours per week the capital actually operates (e.g., Shapiro 1996).

The thick line in Figure 2 controls for the effects of varying utilization on measured TFP. Our method follows Basu, Fernald, and Kimball (2006) in using the variation in hours per worker as a proxy for variations in labor effort and capital’s workweek. The discussion above suggests that hours per worker is an observable measure of factor intensity related to other, less visible measures of intensity, including labor effort and the workweek of capital—implying that measured TFP should tend to move in the same direction. Using annual industry data, Basu, Fernald, and Kimball found that the effect of changes in hours per worker on measured TFP is indeed statistically and economically significant.

Over the past two years, TFP growth adjusted for sharply declining labor and capital utilization nearly matches its long-term average since 1947 of 1.4% per year. The pace has been particularly rapid over the past year, exceeding its average of 1.7% over the recent fast-growth period from about 1995 to 2005.

The utilization measure used for this adjustment assumes that the recent relationship between observed hours worked and unobserved labor effort and capital’s workweek is consistent with its historical pattern. The direction and rough magnitude of the correction is consistent with other measures of utilization. Most notably, the Federal Reserve’s measure of capacity utilization for manufacturing, mining, and utilities has fallen to the lowest level ever recorded since the series began in 1948.

Adjusted TFP remains highly volatile. Some part of the volatility may reflect the lack of measurement of “intangible” investments, such as research and development, improved business processes, or installation of capital (Oliner, Sichel, and Stiroh 2007). These investments divert resources from current production, reducing measured productivity in the present, but are clearly important for maintaining growth. Some of the strong recent utilization-adjusted TFP performance might result from cash flow concerns that have led firms to defer intangible investment causing measured utilization-adjusted TFP to rise temporarily relative to its true value. One interpretation of the surge of utilization-adjusted TFP in the early 2000s is that firms were substantially deferring such intangible investments. Once the economy recovered in the mid-2000s, utilization-adjusted TFP fell very sharply, as is apparent in the figure, as firms once again began making unobserved intangible investments aimed at future production.

By its very nature, the intangibles story is difficult to assess. Nevertheless, there is no reason to think that the pace of innovation and efficiency gains has actually fallen recently.

Implications for potential output

The strength of utilization-adjusted TFP raises doubts about several seemingly plausible arguments for why the level of potential output might have declined recently. In particular, an impaired financial sector and the need to reallocate resources should reduce utilization-adjusted TFP. However, given the strong growth in this measure, these stories might not be quantitatively important.

First, an impaired financial sector could reduce the economy’s efficiency by, for example, making it more difficult for firms to obtain credit needed to buy key intermediate inputs. In addition, some firms might be unable or unwilling to finance high-productivity projects. The strength of utilization-adjusted TFP performance thus far suggests that an impaired financial sector has not yet substantially reduced efficiency. Possibly, the financial sector was not, in fact, better at allocating resources earlier in the 2000s than it is now or promises to be going forward.

Second, the need to reallocate resources away from finance, construction, and perhaps other areas takes resources (such as lawyers and search firms) that are not, then, available to produce current market output. In essence, these resources are a form of intangible investment involved in moving resources to where they are most valuable. As a result, while the reallocation is occurring, the economy’s measured output is likely to be low relative to inputs. Moreover, to the extent that tangible, intangible, and human capital is specialized for use in finance and construction and cannot be used elsewhere, then this capital is effectively scrapped. If this happens, actual and potential output fall. But our statistics assume the capital is still in place, so measured utilization-adjusted TFP again should fall. Hence, the recent strength of utilization-adjusted TFP suggests that the drag from reallocation is probably not large relative to other factors driving potential output, including the underlying pace of innovation and efficiency gains.

Finally, if firms are currently reducing other intangible investments, then true utilization-adjusted TFP is lower than we measure. This story would imply that true potential output is also lower than it appears. However, it does not necessarily imply that there is less slack in the economy. In particular, the true values of both current utilization-adjusted TFP and current actual output—adjusted for reduced production of intangibles—are both lowered by the same amount.

Conclusion

As is typical in recessions, measured total factor productivity growth has fallen during the current downturn. After adjusting for declining factor utilization, however, TFP growth has exceeded its long-term pace over the year. Impairment of the financial sector and a substantial shift of resources away from construction and finance imply that utilization-adjusted TFP growth should have fallen. To the extent that reduced intangible investment has driven a higher fraction of resources to current market output, thereby supporting robust growth of adjusted TFP, this strength might be overstated somewhat. Nevertheless, there is no evidence that the pace of efficiency gains has slowed.

The full ramifications of the current economic and financial crisis for the underlying pace of potential output growth are surely complex. However, in most models of the economy, technological innovations are a key determinant of potential output. So, to the extent that efficiency gains have been maintained through the crisis, growth accounting offers little evidence that potential output itself has fallen. Given the large declines in actual output, the estimates are consistent with a substantial gap between actual and potential output.

Going forward, capital is unlikely to contribute meaningfully to potential output growth over the next year. This weakness is likely to reduce potential output growth by about a percentage point compared with its recent history. If sustained efficiency gains continue, however, the weakness in potential output growth will be muted.

References

Basu, Susanto, John Fernald, and Miles Kimball. 2006. “Are Technology Improvements Contractionary?” American Economic Review 96(5, December) pp. 1418–1448.

Fernald, John. 2009. “A Quarterly Utilization-Adjusted Series on Total Factor Productivity.” Manuscript, Federal Reserve Bank of San Francisco.

Oliner, Stephen D., Daniel E. Sichel, and Kevin J. Stiroh. 2007. “Explaining a Productive Decade.” Brookings Papers on Economic Activity 38(2007-1) pp. 81–152.

Orphanides, Athanasios. 2002. “Monetary Policy Rules and the Great Inflation.”American Economic Review Papers and Proceedings 92(2, May) pp. 115–120.

Shapiro, Matthew. 1996. “Macroeconomic Implications of Variation in the Workweek of Capital.” Brookings Papers on Economic Activity 1996(2), pp. 79–133.

Valletta, Rob, and Aisling Cleary. 2008. “Sectoral Reallocation and Unemployment.” FRBSF Economic Letter 2008-32 (October 17).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org