After the Great Recession, the fraction of U.S. workers whose wages were frozen reached a record high. Many employers would have preferred to cut wages, but couldn’t do so because of the reluctance of workers to accept reduced compensation. These pent-up wage cuts initially propped up wage growth, reduced hiring, and pushed up unemployment. But, over the past 2½ years, inflation has eroded the real value of frozen wages, slowing wage growth and reducing the unemployment rate. This is similar to, but more pronounced than, the pattern observed in past recessions.

During the most recent recession the unemployment rate jumped 5.6 percentage points, but wage growth slowed only modestly. The economy has been recovering for four years and unemployment has declined considerably, but wage growth has continued to slow. These patterns contradict standard economic models that hold that unemployment and wage growth normally are tightly related and move in opposite directions.

This Economic Letter argues that these patterns are consistent with the reluctance of employers to adjust wages immediately in reaction to changing economic conditions. In particular, employers hesitate to reduce wages and workers are reluctant to accept wage cuts, even during recessions. This behavior, known as downward nominal wage rigidity, played a role in past recessions, but was especially apparent during the Great Recession. Wage rigidity kept nominal wage growth positive throughout the recession. This led to a significant buildup of pent-up wage cuts, that is, wage cuts that employers wanted, but were unable to make. As the economy recovers, pent-up wage cuts will probably continue to slow wage growth long after the unemployment rate has returned to more normal levels.

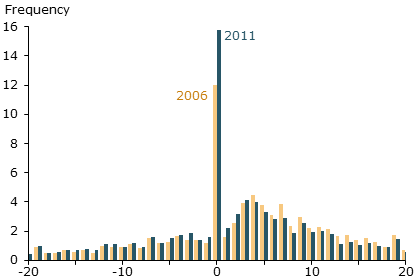

Figure 1

Distribution of wage changes in 2006 and 2011

Source: Current Population Survey and authors’ calculations.

Note: Wage changes are measured as approximate percentage changes.

The existence of downward nominal wage rigidity

Figure 1 clearly shows downward nominal wage rigidity in the distribution of wage changes among U.S. workers in 2006 and 2011. The data cover all workers and measure how their wages compared with their previous year’s wages, if they were employed. We use 2006 as an example of a typical wage change distribution and compare those numbers with the post-recession wage changes for 2011.

The distribution of wage changes in 2006 and 2011 both spike at zero, suggesting that the wages of many workers did not change from year to year. In both years, the distribution is larger to the right of zero, that is, for wage increases, than to the left of zero, for wage cuts. Consistent with downward nominal rigidity, this suggests that a large fraction of wage cuts employers wanted to carry out were not actually made. Instead, those workers were swept into the zero-change group.

What is more interesting in this figure is how 2006 and 2011 data differ. First, the fraction of workers whose wages were frozen jumped from 12% of the workforce in 2006 to 16% in 2011. Second, despite the severity of the Great Recession, very few workers experienced wage cuts. These numbers edged up only slightly from 2006 to 2011. Finally, and perhaps most interestingly, the percentage of workers who received wage increases dropped notably in 2011 compared with 2006. This compression of wage increases resulted in a larger spike at zero.

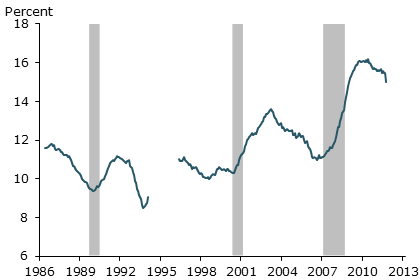

Figure 2

Workers with no wage change, 1986–2012

Source: Current Population Survey and authors’ calculations.

The larger distribution of workers whose wages did not change is not unique to the 2007 recession. Figure 2 plots the share of workers with no wage change year-over-year from 1986 through 2012. The percentage of workers whose wages are fixed over a year always increases during labor market downturns. The figure depicts notable increases in workers with frozen wages in the wake of the 1990 and 2001 recessions, which are shown by the gray bars. Yet the size of the spike following the 2007 recession sets it apart from the other recessions (see Daly, Hobijn, and Lucking 2012).

Wage growth and unemployment: The wage Phillips curve

The downward nominal rigidity shown in Figures 1 and 2 may explain some of the unusual dynamics of wage growth and unemployment during the most recent recession and recovery. To examine this, we turn to a relationship documented by William Phillips in 1958, known as the wage Phillips curve. The wage Phillips curve captures the relationship between wage growth and changes in unemployment relative to its natural rate, which is the lowest unemployment rate an economy can sustain over the long run without igniting inflation. We examine how the wage Phillips curve has behaved from 1986 to 2012, highlighting how it deviates during recessions from the normal close inverse relationship between wage growth and the unemployment gap.

To plot a U.S. wage Phillips curve, we need two inputs: wage growth and the unemployment gap. For aggregate wages, we combine four popular surveys compiled by the Bureau of Labor Statistics: compensation per hour, the employment cost index, average hourly earnings, and median usual weekly earnings. These are slightly different measures of compensation covering slightly different groups of workers. We use a statistical method called principal components to extract a single measure that captures the common signal from each of these series. The resulting combined wage growth measure is highly correlated with each of the four individual measures, but is considerably less volatile.

To measure the unemployment gap, we compute the difference between the unemployment rate and its natural rate as estimated by the Congressional Budget Office (2012). The unemployment gap is considered a good measure of labor market strength. When the unemployment gap is high, unemployment is far above its natural rate, and the labor market is weak and has a lot of slack. When the unemployment gap is low, the labor market is strong and slack is low.

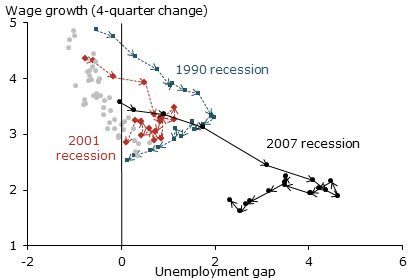

Figure 3

U.S. wage Phillips curve, 1986-2012

Source: Bureau of Labor Statistics and authors’ calculations.

The wage Phillips curve is based on the idea that, as labor market slack rises, wage growth will fall, and vice versa. Figure 3 plots the relationship between our measures of the unemployment gap and wage growth from 1986 to 2012. In particular, three sequences connected by arrows in the figure show the path of this relationship during and after the past three recessions. The gray points not connected by arrows show the relationship during the other quarters in our 27-year sample.

Overall, the wage Phillips curve displays the expected relationship between wage growth and labor market slack (see Phillips 1958, Samuelson and Solow 1960, and Galí, 2011). Higher slack measured by the unemployment gap is correlated with slower wage growth, and lower slack is correlated with faster wage growth. The gray dots in Figure 3 reflect this normal relationship. However, the basic relationship between wage growth and labor market slack breaks down during and after recessions. In each of the three recession series in Figure 3, wage growth slows much less than expected as the unemployment gap increases. Wage growth then continues to slow long after the unemployment gap has begun to normalize.

To see this more clearly it is useful to break the pattern traced by the arrows into two phases. The first is the recessionary period, when the unemployment rate runs up, pushing up the unemployment gap. During this phase, wage growth declines less than its usual relationship with the unemployment gap would indicate. The second phase is the recovery. As the unemployment rate starts to decline during the labor market recovery, wage growth continues to decline. Consequently, during the early part of recoveries, labor market slack and wage growth move down together in a positive relationship, rather than the negative relationship that characterizes the average wage Phillips curve. The result is that recessions generate clockwise loops in the wage Phillips curve. These loops coincide with periods when the fraction of workers with no wage changes rises sharply, shown by the spikes in Figure 2.

Interpreting clockwise loops in the wage Phillips curve

Combining the evidence from the figures suggests that pent-up wage cuts due to downward nominal wage rigidity (Figure 2) could be the source of the clockwise loops in the wage Phillips curve (Figure 3). In Daly and Hobijn (2013), we pursue this idea, showing that clockwise loops in the wage curve occur naturally in a simple model of monetary policy with downward nominal wage rigidity. This pattern may reflect that, as the economy falls into a recession, businesses would like to reduce wages, but cannot do so because of downward wage rigidity. With wages fixed above their optimal value, employers lay off more workers and hire fewer workers than they normally would. The unemployment rate increases more than it would if wages were flexible and could adjust downward. This disproportionate adjustment is reflected in the first phase of the wage Phillips curve loops.

As the recovery takes hold, businesses gradually reduce wage growth. At the same time, inflation typically erodes the real wages of workers, relieving some of the pent-up demand of employers for wage cuts. This gradual process can continue long after the unemployment gap begins to narrow. At the same time, slower wage growth also means businesses are able to hire more workers, which stimulates the demand for labor and pushes the unemployment rate down further. This is what drives the second phase of the clockwise loops.

In both phases, downward nominal wage rigidity causes the unemployment gap and wage growth to diverge from their normal relationship. As the economy gradually recovers, this divergence is corrected and the wage Phillips curve returns to normal.

Conclusion

Evidence shows that pent-up wage cuts reflecting downward nominal wage rigidity have been an important force during the most recent recession and recovery. This has shaped the dynamics of unemployment, wage growth, and inflation from 2006 to 2012. The Great Recession was not special, however. We find that pent-up wage cuts have slowed wage growth in the aftermath of all three recessions since 1986. The main difference is that the depth of the most recent recession has intensified the impact of downward nominal wage rigidity. The spike in workers who are experiencing no wage changes has reached record levels. Once it begins to decline, we expect wage growth to accelerate.

Mary C. Daly is a senior vice president and associate director of research in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Bart Hobijn is a senior research advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Timothy Ni is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Congressional Budget Office. 2012. The Budget and Economic Outlook: Fiscal Years 2012 to 2022. Washington, DC: Congressional Budget Office.

Daly, Mary C., and Bart Hobijn. 2013. “Downward Nominal Wage Rigidities Bend the Phillips Curve.” FRB San Francisco Working Paper 2013-08.

Daly, Mary C., Bart Hobijn, and Brian Lucking. 2012. “Why Has Wage Growth Stayed Strong?” FRBSF Economic Letter 2012-10 (April 2).

Galí, Jordi. 2011. “The Return of the Wage Phillips Curve.” Journal of the European Economic Association 9(3), pp. 436–461.

Phillips, A. William. 1958. “The Relationship between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom 1861–1957.” Economica 25(100), pp. 283–299.

Samuelson, Paul A., and Robert M. Solow. 1960. “Analytical Aspects of Anti-Inflation Policy.” American Economic Review 50, pp. 177–194.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org