Interest rates during the current economic recovery have been unusually low. Some have argued that yields have been pushed down by declines in longer-run expectations of the normal inflation-adjusted short-term interest rate—that is, by a drop in the so-called equilibrium or natural rate of interest. New evidence from financial markets shows that a decline in this rate has indeed contributed about 2 percentage points to the general downward trend in yields over the past two decades.

The general level of U.S. interest rates has gradually fallen over the past few decades. In the 1980s and 1990s, lower inflation expectations played a key role in this decline. But more recently, actual inflation as well as survey-based measures of longer-run inflation expectations have both stabilized close to 2%. Therefore, some researchers have argued that the decline in interest rates since 2000 reflects a variety of persistent economic factors other than inflation. These longer-run real factors—such as slower productivity growth and an aging population—affect global saving and investment and can push down yields by lowering the steady-state level of the short-term inflation-adjusted interest rate (Bauer and Rudebusch 2016 and Williams 2016). This normal real rate is often called the equilibrium or natural or neutral rate of interest—or simply “r-star.”

However, other observers have dismissed the evidence for a new lower equilibrium real rate and downplayed the role of persistent factors. They argue that yields have been held down recently by temporary factors such as the headwinds from credit deleveraging in the aftermath of the financial crisis. So far, this ongoing debate about a possible lower new normal for interest rates has focused on estimates drawn from macroeconomic models and data. In this Economic Letter, we describe new analysis that uses financial models and data to provide an alternative perspective (see Christensen and Rudebusch 2017). This analysis uses a dynamic model of the term structure of interest rates that is estimated on prices of U.S. Treasury Inflation-Protected Securities (TIPS). The resulting finance-based measure provides new evidence that the equilibrium interest rate has gradually declined over the past two decades.

Macro-based estimates of the equilibrium interest rate

The issue of whether there has been a persistent shift in the equilibrium interest rate is quite important. For investors, this short-term real rate of return that would prevail in the absence of transitory disturbances serves as a key foundation for valuing financial assets. For policymakers and researchers, the equilibrium interest rate provides a neutral benchmark to calibrate the stance of monetary policy: Monetary policy is expansionary if the short-term real interest rate lies below the equilibrium rate and contractionary if it lies above. Therefore, determining a good estimate of the equilibrium real rate has been at the center of recent policy debates (Nechio and Rudebusch 2016 and Williams 2017).

Given the significance of the equilibrium interest rate, many researchers have used macroeconomic models and data to try to pin it down. As Laubach and Williams (2016, p. 57) define it, the equilibrium interest rate is based on “a ‘longer-run’ perspective, in that it refers to the level of the real interest rate expected to prevail, say, five to 10 years in the future, after the economy has emerged from any cyclical fluctuations and is expanding at its trend rate.” Laubach and Williams (2003, 2016) estimate this equilibrium interest rate using a simple macroeconomic model and data on a nominal short-term interest rate, consumer price inflation, and the output gap. Similarly, Johannsen and Mertens (2016) and Lubik and Matthes (2015) provide closely related estimates also by using macroeconomic models and data.

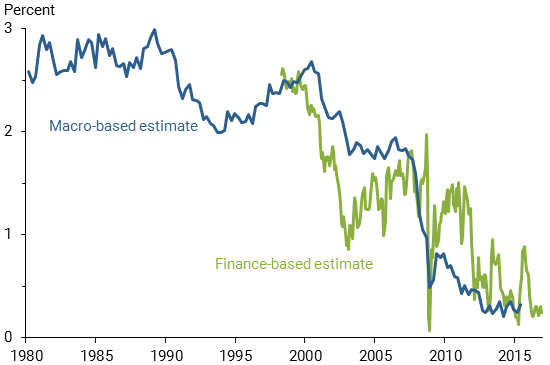

The blue line in Figure 1 summarizes the results of these three fairly similar studies. It shows the average of their three estimated equilibrium real interest rates, which smooths across specific modeling assumptions in each study. In the 1980s and 1990s, this simple macro-based summary measure remained around 2½%. This effectively constant equilibrium interest rate is consistent with the conventional wisdom of that time. It is only in the late 1990s that a decided downtrend begins, and the macro-based measure falls to almost zero by the end of the sample.

Figure 1

Estimates of the equilibrium real interest rate

However, the various macro-based approaches for identifying a new lower equilibrium interest rate have several potential shortcomings. First, these estimates depend on having the correct specification of the complete model, including the output and inflation dynamics. One difficulty in this regard is how to account for the period after the Great Recession when nominal interest rates were constrained by the zero lower bound. During that episode, the link between interest rates and other elements in the economy was altered in ways that are difficult to model. Finally, these estimates use extensively revised macroeconomic data to create historical equilibrium interest rate estimates that would not have been available in real time.

A new finance-based estimate of the equilibrium interest rate

Given the possible limitations of the macro-based estimates, we turn to financial models and data to provide a complementary estimate of the equilibrium interest rate. As detailed in Christensen and Rudebusch (2017), we use the market prices of TIPS, which have coupon and principal payments adjusted for changes in the consumer price index (CPI). These securities compensate investors for the erosion of purchasing power due to price inflation, so they provide a fairly direct reading on real interest rates. We assume that the longer-term expectations embedded in TIPS prices reflect financial market participants’ views about the steady state of the economy including the equilibrium interest rate. Unlike the macro-based estimates, one advantage of this market-based measure is that it can be obtained in real time at a high frequency—even daily. In addition, it doesn’t depend on an uncertain specification of the dynamics of output and inflation. Furthermore, because real TIPS yields are not subject to a lower bound, we avoid complications associated with zero nominal interest rates altogether.

Our analysis focuses on a term structure model that is based only on the prices of TIPS. This choice contrasts with previous TIPS research that has jointly modeled inflation-indexed and standard nominal U.S. Treasury yields (for example, Christensen, Lopez, and Rudebusch 2010). Such joint specifications can also be used to estimate the steady-state real rate—though earlier work has emphasized only the measurement of inflation expectations and risk. However, a joint specification requires additional modeling structure—including specifying an inflation risk premium and inflation expectations. The greater number of modeling elements—along with the requirement that this more elaborate structure remain stable over the sample—raise the risk of model misspecification, which can contaminate estimates of the equilibrium interest rate. By relying solely on TIPS yields, we avoid these complications as well as problems associated with the lower bound on nominal rates.

Still, the use of TIPS for measuring the steady-state short-term real interest rate poses its own empirical challenges. One difficulty is that inflation-indexed bond prices include a real term premium. In addition, despite the fairly large amount of outstanding TIPS, these securities face appreciable liquidity risk resulting in wider bid-ask spreads than nominal Treasury bonds. To estimate the equilibrium rate of interest from TIPS in the presence of liquidity and real term premiums, we use an arbitrage-free dynamic term structure model of real yields augmented with a liquidity risk factor as described in Andreasen, Christensen, and Riddell (2017). The identification of the liquidity risk factor comes from its unique loading for each individual TIPS. This loading assumes that, over time, an increasing proportion of any bond’s outstanding inventory is locked up in buy-and-hold investors’ portfolios. Given forward-looking investor behavior, this lock-up effect implies that a particular bond’s sensitivity to the market-wide liquidity factor will vary depending on how seasoned the bond is and how close to maturity it is. Our analysis uses prices of the individual TIPS rather than the more usual input of yields from fitted synthetic curves. By observing prices from a cross section of TIPS that have different age characteristics, we can identify the liquidity factor. With estimates of both the liquidity premium and real term premium, we calculate the equilibrium interest rate as the average expected real short rate over a five-year period starting five years ahead.

Our finance-based estimate of the natural rate of interest is shown as the green line in Figure 1. These estimates are adjusted slightly upward to account for a persistent 0.23 percentage point measurement bias in CPI inflation. The model uses data back to the late 1990s around the time when the TIPS program was launched. Fortuitously, TIPS were introduced about the same time as the macro-based estimates started to decline, so the available sample is particularly relevant for discerning shifts in the equilibrium real rate. During their shared sample, the macro- and finance-based estimates exhibit a similar general trend—starting from just above 2% in the late 1990s and ending the sample near zero. Most importantly, both methodologies imply that the equilibrium rate is currently near its historical low. The finance- and macro-based estimates of the equilibrium rate rely on different assumptions about the structure of the economy and different data sources. Thus, they have different pros and cons, so their broad agreement about the level of the equilibrium rate is mutually reinforcing.

There are differences between the precise trajectories over time of the two estimates. The macro-based estimate of the natural rate shows only a modest decline from the late 1990s until the financial crisis and the start of the Great Recession. Then, it drops precipitously to less than 1% and edges only slightly lower thereafter. Arguably, the timing of the macro-based path leaves open the possibility that the recession played a key role in causing the decline in the equilibrium rate. This suggests that the drop could be at least partly reversed by a cyclical boom. In contrast, the finance-based estimate falls in the early 2000s, levels off a bit above 1%, and then declines more in 2012. Therefore, the drop in the finance-based estimate does not coincide with the Great Recession, which is consistent with more secular drivers such as demographics or a productivity slowdown.

Finally, we should note that the model dynamics of fluctuations in the equilibrium rate are estimated to be very persistent. Thus, looking ahead, our model also suggests that the natural rate is more likely than not to remain near its current low for at least the next several years.

Conclusion

Given the historic downtrend in yields in recent decades, many researchers have investigated the factors pushing down the steady-state level of the short-term real interest rate. To complement earlier empirical work based on macroeconomic models and data, we estimate the equilibrium real rate using only prices of inflation-indexed bonds. From 1998 to the end of 2016, we estimate that the equilibrium real rate fell from just over 2% to just above zero. Accordingly, our results show that about half of the 4 percentage point decline in longer-term Treasury yields during this period represents a reduction in the natural rate of interest.

Jens H.E. Christensen is a research advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Glenn D. Rudebusch is senior policy advisor and executive vice president in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Andreasen, Martin M., Jens H.E. Christensen, and Simon Riddell. 2017. “The TIPS Liquidity Premium.” FRB San Francisco Working Paper 2017-11.

Bauer, Michael D., and Glenn D. Rudebusch. 2016. “Why Are Long-Term Interest Rates So Low?” FRBSF Economic Letter 2016-36 (December 5).

Christensen, Jens H.E., Jose A. Lopez, and Glenn D. Rudebusch. 2010. “Inflation Expectations and Risk Premiums in an Arbitrage-Free Model of Nominal and Real Bond Yields.” Journal of Money, Credit, and Banking 42(6), pp. 143–178.

Christensen, Jens H.E., and Glenn D. Rudebusch. 2017. “A New Normal for Interest Rates? Evidence from Inflation-Indexed Debt.” FRB San Francisco Working Paper 2017-07.

Johannsen, Benjamin K., and Elmar Mertens. 2016. “The Expected Real Interest Rate in the Long Run: Time Series Evidence with the Effective Lower Bound.” FEDS Notes, Board of Governors of the Federal Reserve System, February 9.

Laubach, Thomas, and John C. Williams. 2003. “Measuring the Natural Rate of Interest.” Review of Economics and Statistics 85(4, November), pp. 1,063–1,070.

Laubach, Thomas, and John C. Williams. 2016. “Measuring the Natural Rate of Interest Redux.” Business Economics 51(2), pp. 57–67.

Lubik, Thomas, and Christian Matthes. 2015. “Calculating the Natural Rate of Interest: A Comparison of Two Alternative Approaches.” FRB Richmond Economic Brief 15-10 (October 15).

Nechio, Fernanda, and Glenn D. Rudebusch. 2016. “Has the Fed Fallen behind the Curve This Year?” FRBSF Economic Letter 2016-33 (November 7).

Williams, John C. 2016. “Monetary Policy in a Low R-star World.” FRBSF Economic Letter 2016-23 (August 15).

Williams, John C. 2017. “Three Questions on R-star.” FRBSF Economic Letter 2017-05 (February 21).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org