Zheng Liu, senior research advisor at the Federal Reserve Bank of San Francisco, states his views on the current economy and the outlook.

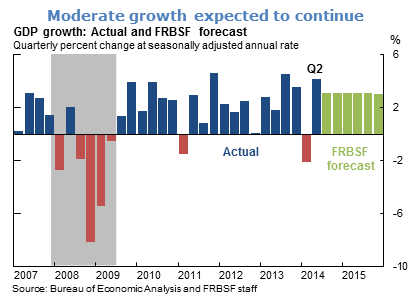

- Real GDP expanded at an annual rate of 4.2% in the second quarter, according to the latest Bureau of Economic Analysis estimate in late August. This was similar to the initial estimate in July, and confirms that the economy bounced back sharply from the first-quarter dip.

- Recent data suggest that economic momentum was largely sustained entering the second half of this year, although growth is likely to slow somewhat from the strong second quarter. Overall consumer spending in recent months has been disappointing, but motor vehicle sales have been robust. Housing market activity has been encouraging, and overall construction spending has risen. Industrial production also continued to expand in recent months. The July durable goods report was mixed but generally consistent with ongoing growth in the manufacturing sector. On balance, we expect real GDP to grow at about a 3% pace over the remainder of this year and next year.

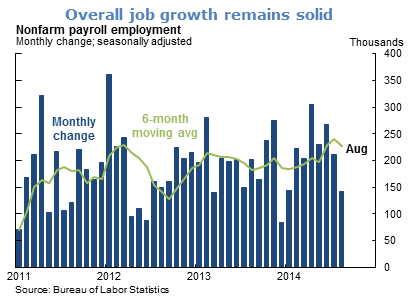

- Labor market conditions continue to improve, although more slowly than earlier in the year. Nonfarm payrolls rose by 142,000 in August, which was well below expectations. Total payroll employment in June and July were revised downward. Despite the August disappointment, the overall labor market improvement over the past year remains solid.

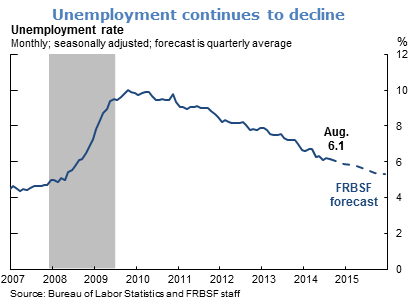

- Solid employment growth this year has helped lower the unemployment rate, which fell slightly from 6.2% in July to 6.1% in August. Moreover, the labor force participation rate, which had been steadily declining since 2008, was largely stable in recent months. Among other indicators of labor market improvement, a broader measure of underemployment, including people who are unemployed, marginally attached to the labor force, and working part-time for economic reasons, has declined significantly since the beginning of this year. The share of long-term unemployed—those who have been without jobs for 27 weeks or more—has also declined substantially over the past few months. Despite this sustained improvement, the broad array of labor market indicators suggest continued slack.

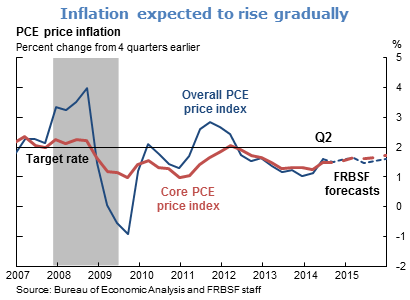

- Although inflation stepped up in the second quarter of this year, it remains below the Federal Open Market Committee’s objective of 2%. In July, both the overall and the core personal consumption expenditures price index (PCEPI) rose at a very modest pace, suggesting that the second-quarter pressures have ebbed. Recent declines in oil prices are also likely to further constrain the rise in the overall PCEPI. We expect inflation to continue to rise slowly towards the 2% target.

- The improving labor market has been a key factor underlying the steady reduction this year in the pace of monthly asset purchases by the Federal Reserve. However, with substantial economic slack and inflation below the FOMC’s target, monetary policy remains highly accommodative.

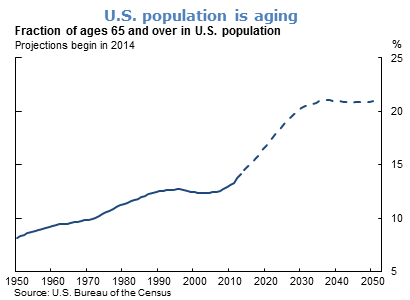

- Looking ahead to longer-term growth in the U.S. economy, population aging may be a significant headwind. In the next two decades, the share of individuals age 65 and older in the total U.S. population will increase sharply according to projections from the U.S. Census Bureau. This demographic change will be driven mainly by the aging of the baby-boom generation—the 76 million people born between 1946 and 1964.

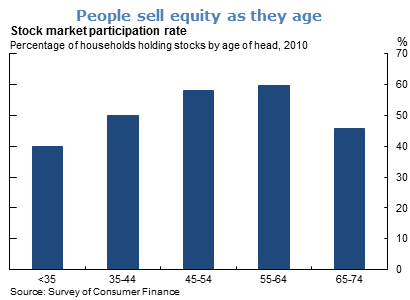

- An aging population may have an adverse impact on the U.S. equity market and the macroeconomy in general. Evidence suggests that an investor’s risk tolerance changes over the life cycle. As the boomers transition from work into retirement over the next 10 to 15 years, they are likely to switch from buying to selling stocks. Since the boomers represent a large fraction of the population, changes in their investment behavior can have a meaningful effect on the U.S. stock market.

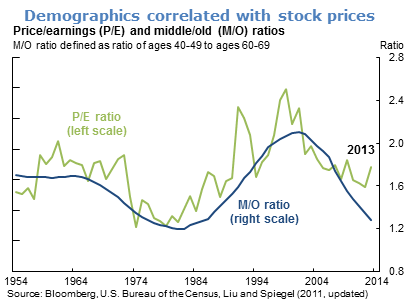

- Recent research shows that the long-term swings in the price-to-earnings (P/E) ratio of the U.S. stock market are highly correlated with the evolution of the population’s age structure during the post-World War II period. A substantial fraction of the fluctuations in the stock market’s P/E ratio can be explained by changes in the ratio of people ages 40 to 49 years to those ages 60 to 69.

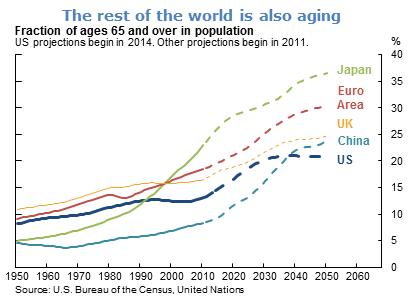

- As U.S. boomers approach retirement and decide sell their equity holdings, the number of sellers relative to buyers will increase, putting downward pressure on stock prices. This pressure can be partially offset, in principle, if foreign investors are willing to buy U.S. equities. However, the rest of the world is also aging, so other countries may face similar challenges, dimming that hope.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.