Michael Bauer, senior economist at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of August 11, 2016.

- Recent data support our view of continued moderate growth in the U.S. economy, with the labor market at or very close to full employment, and inflation increasing towards the Federal Open Market Committee’s 2% target.

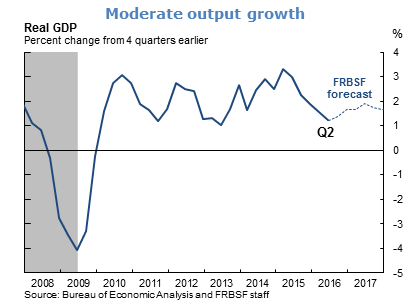

- Growth figures for the first half of this year have been weak. First quarter real GDP growth was recently revised down to an annualized rate of 0.8%. However, in recent years, first quarter growth estimates have tended to be understated because of incomplete adjustment for seasonal effects. Second quarter output also grew slower than expected at 1.2%, but the sizable negative contribution from inventory investment, a very volatile component of GDP, is likely to be transitory. In contrast to the weak headline figures, household spending remains strong, bolstered by low energy prices, strong balance sheets, and rising incomes. Real final sales of domestic goods have exhibited healthy growth, increasing 2.4% annualized in the second quarter.

- We forecast moderate output growth for the second half of this year and 2017 at a rate slightly below 2%. Inventory investment is expected to increase as companies rebuild their stocks. While the outlook for investment remains weak, particularly for the energy sector, we anticipate that it will gradually improve as business profitability increases. Foreign growth remains anemic, but the passage of the United Kingdom’s “Brexit” vote to leave the European Union has not led to a noticeable downgrade in our forecast for the U.S. economy.

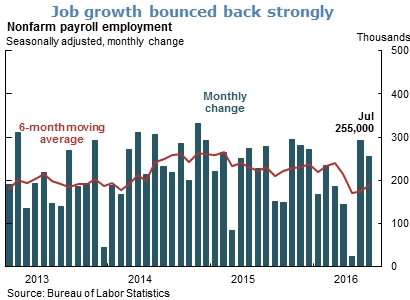

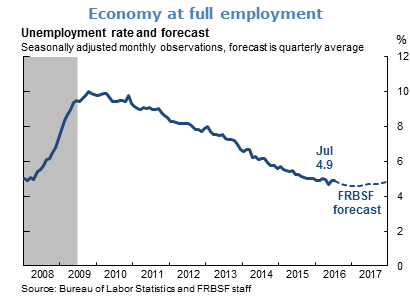

- U.S. job growth remains strong, with gains in nonfarm payroll employment exceeding 250,000 jobs for two months in a row, and the 6-month moving average around 190,000 jobs. The unemployment rate is at 4.9%, a level consistent with full employment, and other indicators also suggest little if any slack remaining in the labor market. Wage growth has accelerated and labor market participation is near our estimate of its long-run trend.

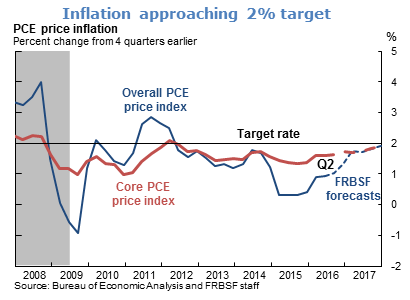

- The rate of inflation has increased over the first half of this year, with growth in the price index for core personal consumption expenditures (PCE) over the last month at 1.6%. We expect these increases to continue, though in smaller increments, and for PCE inflation to reach the FOMC’s 2% target in the next year or two.

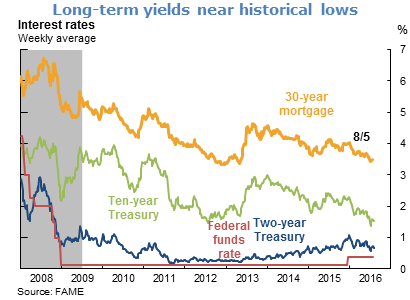

- Financial conditions remain highly accommodative and are supporting growth in aggregate demand. Long-term interest rates are near historical lows, with the 10-year Treasury yield reaching the lowest level on record in early July. In addition to domestic factors, such as accommodative monetary policy and a low long-run level of interest rates, international factors are at play as well. In particular, monetary easing by foreign central banks and low interest rates abroad support demand for higher-yielding Treasury securities and continue to put downward pressure on interest rates in the United States.

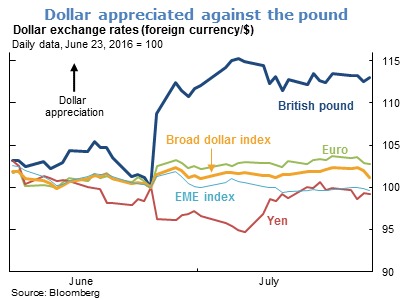

- The Brexit vote led to a pronounced initial reaction in financial markets, lowering equity prices and interest rates globally, and increasing market volatility. However, these effects proved short-lived and U.S. stocks have since reached new highs. While the dollar has appreciated substantially against the British pound as was expected, it has moved little against other major currencies. Due to the absence of lasting effects on financial market conditions or the overall value of the dollar, we anticipate the impact on the U.S. economy to be limited.

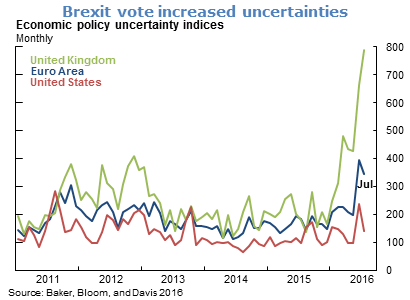

- However, while the Brexit vote resolved some near-term uncertainty, measures of long-term policy uncertainty in Europe suggest that it has increased further. In particular, the level of economic integration that will prevail between the U.K. and the European Union after Brexit is unclear. Moreover, the vote was followed by a pronounced drop in prices of European bank stocks, raising concerns about the health of the European banking system. Many European banks are suffering from low profitability, nonperforming loans, and difficulties in raising capital. Furthermore, recently released stress test results from the European Banking Authority indicate that some large banks in peripheral countries could be vulnerable in stress scenarios.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.