Commercial banks play an important role in the financial system and the economy. As a key component of the financial system, banks allocate funds from savers to borrowers in an efficient manner. They provide specialized financial services, which reduce the cost of obtaining information about both savings and borrowing opportunities. These financial services help to make the overall economy more efficient.

Imagine a World Without Banks

One way to answer your question is to imagine, for a moment, a world without banking institutions, and then to ask yourself a few questions. This is not just an academic exercise; many former eastern-block nations began facing this question when they began to create financial markets and develop market-oriented banks and other financial institutions.

If there were no banks…

- Where would you go to borrow money?

- What would you do with your savings?

- Would you be able to borrow (save) as much as you need, when you need it, in a form that would be convenient for you?

- What risks might you face as a saver (borrower)?

How Banks Work

Banks operate by borrowing funds-usually by accepting deposits or by borrowing in the money markets. Banks borrow from individuals, businesses, financial institutions, and governments with surplus funds (savings). They then use those deposits and borrowed funds (liabilities of the bank) to make loans or to purchase securities (assets of the bank). Banks make these loans to businesses, other financial institutions, individuals, and governments (that need the funds for investments or other purposes). Interest rates provide the price signals for borrowers, lenders, and banks.

Through the process of taking deposits, making loans, and responding to interest rate signals, the banking system helps channel funds from savers to borrowers in an efficient manner. Savers range from an individual with a $1,000 certificate of deposit to a corporation with millions of dollars in temporary savings. Banks also service a wide array of borrowers, from an individual who takes a loan of $100 on a credit card to a major corporation financing a billion-dollar corporate merger.

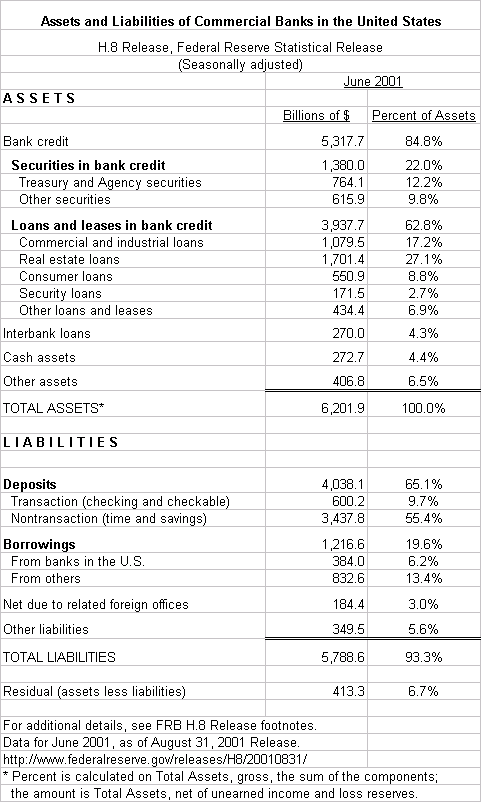

The table below provides a June 2001 snapshot of the balance sheet for the entire U.S. commercial banking industry. It shows that the bulk of banks’ sources of funds comes from deposits – checking, savings, money market deposit accounts, and time certificates. The most common uses of these funds are to make real estate and commercial and industrial loans. Individual banks’ asset and liability composition may vary widely from the industry figures, because some institutions provide specialized or limited banking services.

Banks Are Only One Type of Financial Intermediary

Finally, the U.S. financial services industry and financial markets are highly developed. In recent decades, many new products and services have been created, as well as new financial instruments and institutions. Today, in addition to banks, there are several other important types of financial intermediaries. These include savings institutions, credit unions, insurance companies, mutual funds, pension funds, finance companies, and real estate investment trusts (REITS).

Banks’ assets have grown in recent decades in absolute terms; however, banks have tended to lose market share to even faster growing intermediaries such as pension funds and mutual funds. Still, banks continue to account for a significant share-over 23 percent-of the assets of all financial intermediaries at the end of year 2000, as the chart below shows.

Let me also suggest some more advanced reading materials:

What’s Different about Banks–Still? Milton Marquis.

Federal Reserve Bank of San Francisco. FRBSF Economic Letter. No. 2001-09. Apr. 6, 2001. (8-22-01)

/publications/economics/letter/2001/el2001-09.html

Are Banks Special? A Revisitation. E. Gerald Corrigan.

Federal Reserve Bank of Minneapolis. The Region. No. v. 14, no 1. Mar, 2000 , p. 14-17. (8-22-01)

http://www.minneapolisfed.org/pubs/region/00-03/corrigan.cfm

Personal Financial Education, FederalReserveEducation.org, 2003