This week’s FOMC decision was not an easy choice. Our goals are in conflict. Inflation is above target, the labor market is softening, and there are risks to both sides of our mandate—maximum employment and price stability.

Two charts explain why I ultimately favored a rate cut.

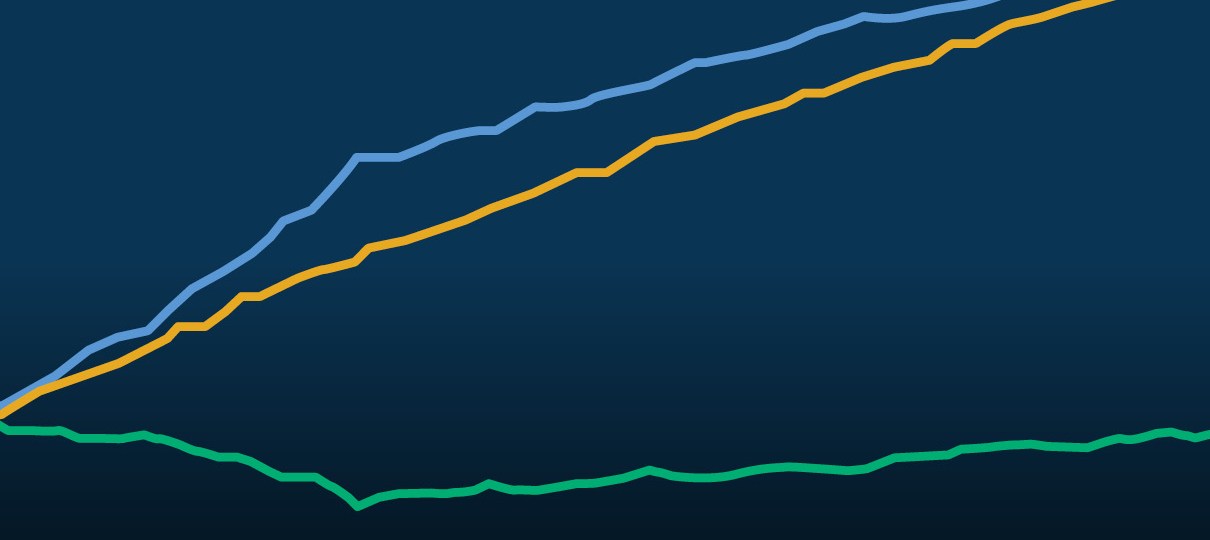

The first shows the damaging cost of high inflation. It has chipped away at real earnings and weakened household purchasing power. Many Americans are still trying to catch up.

Figure 1.

So, the FOMC must continue to bring inflation down. Anything other than 2% is not an option. But it matters how you get there. This means we cannot let the labor market falter.

Real wage gains come from long and durable expansions. And the current expansion is still relatively young, as shown in the second chart. Holding policy too tight can cause undue harm to American families and leave them with two problems: above-target inflation and a weak labor market.

Figure 2.

Congress gave us two goals. And our job is to meet both of them. The recent policy decision puts us in a good place to achieve that.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.