As previously covered in Pacific Exchange, many Asian borrowers increased their U.S. dollar-denominated debt in recent years amid the extraordinarily low global interest rate environment. Recent volatility in global markets has been characterized in part by capital outflows from Asian economies where such debt accumulated, headlined by China, Malaysia, and Indonesia. While emerging Asia remains vulnerable to further capital flight with a majority of its external debt denominated in foreign currency, its bond issuances, which have driven a substantial amount of cross-border credit since the 2008 crisis, are largely in local currency. The further deepening of Asian bond markets combined with borrowers’ ability to issue bonds in their own currencies can insulate them from further volatility in currency and capital markets. Indonesia is going against trend, however, with a declining share of local currency bonds that warrants monitoring.

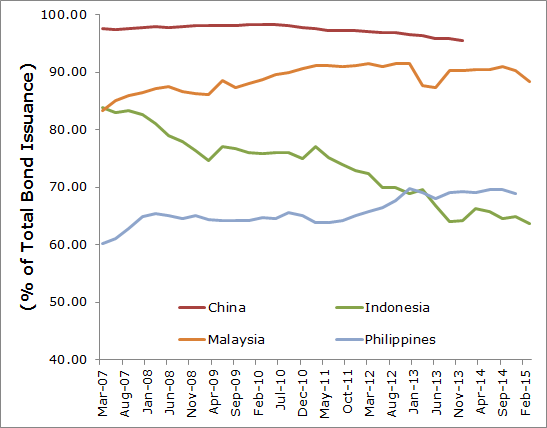

Data on total external debt levels typically releases on a lag—an ongoing issue that the G20 Data Gaps Initiative aims to resolve—and is not readily available for cross-country comparison for the most recent period, but the Asian Development Bank’s (ADB) data on Asian bond issuance does cover activity into the first quarter of 2015. The ADB data indicates that the vast majority of emerging Asia’s bonds have been issued in the currency of the local jurisdiction over the past decade, especially in China (see Figure 1). Indeed, recent analysis from the International Monetary Fund (IMF) indicates China’s issuance of local renminbi bonds has contributed to an increasing share of local currency bond issuance across emerging markets since the global financial crisis (and despite a substantial increase in foreign currency issuance in countries like Indonesia). The ability of Asian economies to tap bond funding in their own currencies reflects the continued development of their financial systems, attractive economic fundamentals, and perceived improvements in macroeconomic management. Combined with the extraordinarily low interest rate environment of the past decade, increased confidence in emerging Asia has led investors to emerging Asian local currency bonds.

Figure 1: Local Currency Bonds in Select Asian Economies

Source: Asian Development Bank

Local currency bonds can insulate an economy from volatility in exchange rates, maintaining the real cost of debt servicing for domestic borrowers even amid a rapidly depreciating local currency. During the 1997-98 Asian Financial Crisis, many countries suffered from a sharp increase in debt servicing costs on foreign currency debt when their national currencies depreciated. While local currency debt provides some insulation from volatility, the IMF does recommend including local currency debt held by foreigners in calculating external debt given the potential for foreign investors to sell such debt and convert to foreign currency (decreasing foreign exchange reserves).

Deeper local currency bond markets offer other advantages to emerging Asia. The development of local bond markets diversifies funding for borrowers historically dependent on bank financing while also giving depositors an alternative savings vehicle. Emerging East Asia’s local currency bond markets represent roughly 58 percent of regional GDP as of March 2015, a reflection of their continued development, but also room for further growth. Developed Asian economies like Korea and Japan have local bond markets valued at over 100 percent of GDP, as do many other OECD countries.

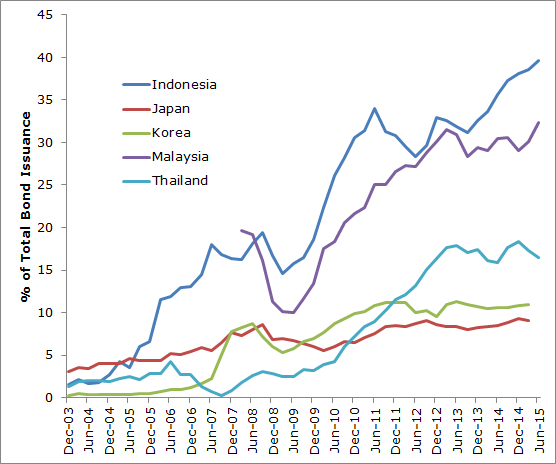

While Asia as a whole has a high proportion of local currency bonds, Indonesia, which has made headlines for capital outflows in 2015, has had a pronounced increase in foreign currency bonds since the global financial crisis. As the IMF notes in its recent analysis, emerging Asia ex-China has actually shown an increase in share of foreign currency bond issuance since the crisis, and this increase is largely explained by Indonesia. Foreign currency bonds now account for 36.3 percent of all Indonesia’s bonds outstanding as of March 2015. This is despite a rapidly growing share of foreign investors in its local currency bond markets—nearly 40 percent, up from less than 5 percent a decade earlier (see Figure 2). According to Bank Indonesia data, bonds represent roughly 23 percent of Indonesia’s external debt.

Figure 2: Foreign Holdings of Local Currency Bonds

Source: Asian Development Bank

Increasing global demand for Indonesian bonds over the past decade indicates growing confidence in the country’s economy, but the larger role of foreign investors coupled with a growing proportion of foreign currency bonds makes Indonesia more vulnerable to global capital market volatility than peers with deeper local bond markets. Indonesia’s private sector is particularly exposed, with 86 percent of externally held bonds issued in foreign currency. Including bank credit, which still provides the vast majority of financing, 96 percent of Indonesia’s external private sector debt is denominated in foreign currencies, and Bank Indonesia has mandated hedging on short-term external borrowings because of this increasing exposure. According to recent analysis by the ADB, 66 percent of a sample of large Indonesian corporate borrowers had no foreign currency revenues to support their foreign currency debt. Among foreign creditors, Singapore is most exposed to Indonesia’s external debt, with $59.1 billion in credit extended to Indonesia’s private sector as of June 2015, roughly 39 percent of the total.

Given the rapidly evolving global monetary policy environment, foreign currency bonds, particularly in Indonesia, warrant further monitoring. Overall, the development of emerging Asia’s local currency bond markets will be positive for the region, providing greater insulation from volatility and also promoting broader financial market development. Increasing the number of foreign investors in local currency bond markets does increase emerging Asia’s exposure to external volatility, but it also helps deepen local bond markets, providing alternatives to the bank financing that dominates many Asian economies.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.