Consumer input has long been an important part of the free market system. It allows businesses to change and adapt products and services based on what individuals want and need at the time. If the speakers on your new laptop break a few weeks after you bought it, you might go online and leave a negative review of the laptop. Ideally, this would cause the manufacturer to look into the issue and ensure that future laptops don’t have the same problem. If the Italian restaurant you went to last week had terrible service, you might give the place a poor rating. Hopefully, this would cause the restaurant to retrain its server staff so that future customers would have better experiences.

Consumer input is just as important to banks as it is to other types of businesses. Financial institutions want to ensure that their customers are treated with fairness and respect and government regulators want to ensure the same thing. With this in mind, the federal bank regulators set up a consumer help center where individuals can file complaints against banks if they feel that they have been mistreated in any way. These complaints will be officially investigated by a federal regulator, and the appropriate action will be taken. While most regulators don’t make data on complaints publicly available, the Consumer Financial Protection Bureau (CFPB), in an effort to promote transparency and accountability, published its consumer complaint database in 2012. In 2015, the CFPB added a feature where consumers could share the details of their complaints with others. This database provides information on certain consumer complaints against the nation’s largest financial institutions. Let’s take a look at some of the numbers.

As seen below, consumer complaints increased in a relatively consistent manner from late 2011 (the earliest data released by the CFPB) to the later part of 2015. The CFPB received the most complaints in July 2015, when 15,900 grievances were filed.

Monthly Consumer Complaints

December 2011-September 2015

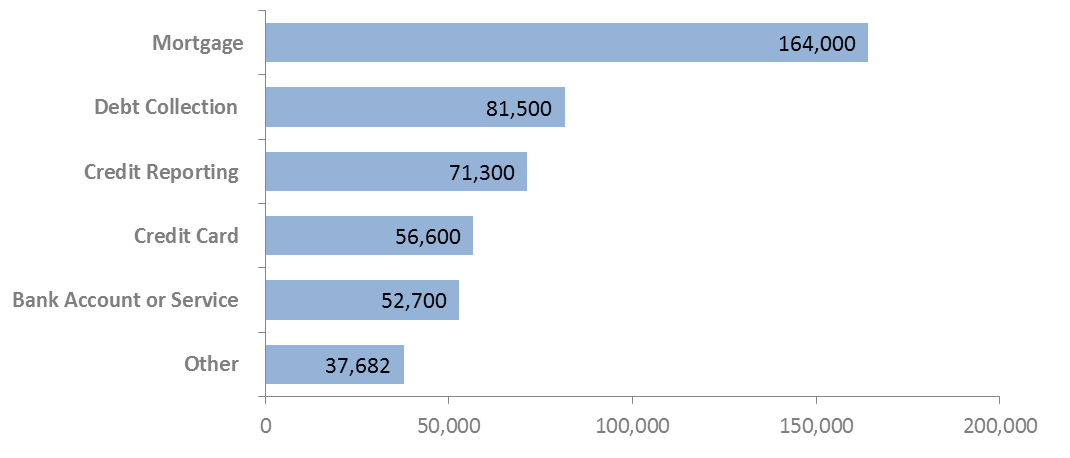

Since December 2011, 464,476 total complaints have been filed to the CFPB. The products identified most often in the complaints are outlined in the chart below.

Type of Product Identified in Complaint

December 2011- September 2015

Issues with mortgages were identified most often, comprising 35 percent of total complaints, with issues over debt collection and credit reporting following, comprising 18 percent and 15 percent of total complaints, respectively. The “other” category mostly represents complaints that have to do with student or consumer loans. When a complaint is submitted to the CFPB, the agency forwards it to the financial institution identified in the complaint. After the financial institution receives the complaint, it has 15 days to respond to the CFPB and the person who filed the complaint. Institutions are expected to close all but the most complicated complaints within 60 days. The individual who filed the complaint will be able to view the institution’s response to his or her complaint and give the CFPB feedback on that response.

While the number of complaints submitted to the CFPB is high, 98 percent of complaints received a timely response. Of these responses, 78 percent were not disputed by the consumer, while 22 percent were.1 As use of this database becomes more widespread, it will be interesting to see whether other federal regulators follow the CFPB’s model of publicizing complaints. The consumer complaint system is by no means perfect, but it is a promising step forward in building trusting relationships between consumers, banks, and regulators.

1. 337,000, or 78 percent, of consumers did not dispute the financial institution’s response, while 95,000, or 22 percent, did. 31,700 consumers of consumer who submitted a complaint did not provide an answer to this question, and these consumers were not factored into the percentages.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.