Monitoring and controlling risks in the shadow banking system is one of the most important tasks facing financial regulators around the world. Prior to the financial crisis, data on activities in the shadow banking system were murky as best. As part of its efforts to address this problem, the Financial Stability Board (FSB) began releasing an annual monitoring report on shadow banking starting in 2011.

In November, the Financial Stability Board issued its fifth Global Shadow Banking Monitoring Report. The report covers economies accounting for 80% of global GDP and 90% of global financial assets, making it the most comprehensive review of trends in shadow banking available.

In the report, shadow banking is broadly defined as credit intermediation involving entities and activities outside of the regular banking system. The FSB looks at the entire universe of non-bank credit and then classifies activities that pose bank-like systemic risks to the financial system as shadow banking. Using this method, the FSB identifies $36 trillion in financial assets as shadow banking as of the end of 2014.

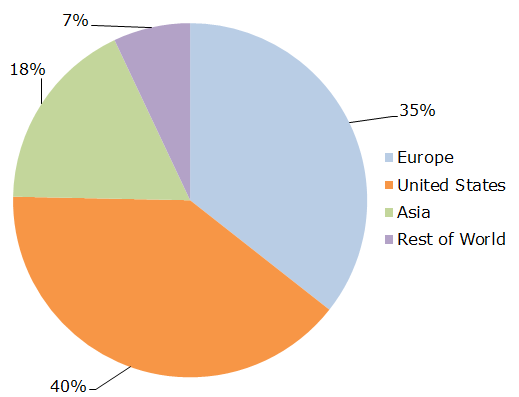

Much of the attention with respect to shadow banking is focused on Europe and the United States. As Figure 1 shows, in 2014 Europe and the United States accounted for 75% of the world total.

Figure 1 – Share of Total Shadow Banking Assets (2014)

Source: FSB, Author

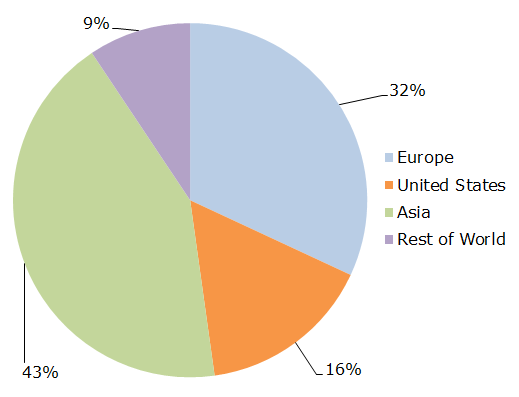

However, the sources of growth within the global shadow banking system are significantly different. As Figure 2 shows, much of the growth in shadow banking has been in Asia. As a result, Asia contributed to the growth rate of shadow banking at a level disproportionate to its share of total assets. In fact, Asia added more to the increase in global shadow banking than either Europe or the United States.

Figure 2 – Share of Shadow Banking Growth (2014)

Source: FSB, Author

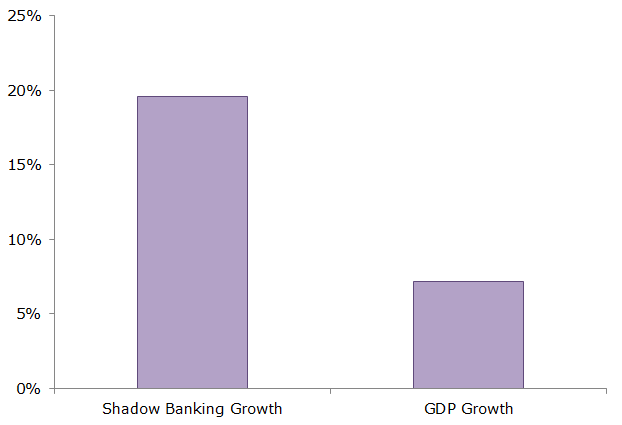

Another interesting comparison available from the data in the FSB report is the growth rate of shadow banking relative to the growth rate of GDP in Asia. As Figure 3 reveals, for the Asian economies included in the study, shadow banking has on average grown significantly faster than GDP over the past four years.

Figure 3 – Shadow Banking vs. GDP Growth in Asia (2011-2014)

Source: FSB, Author

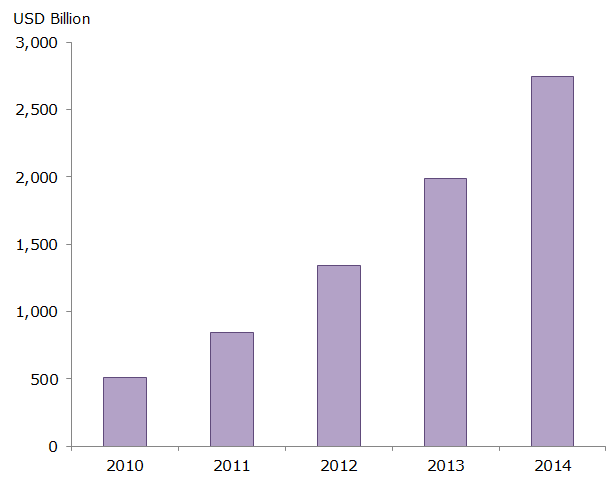

Among all countries included in the report, China stands out as the single largest source of shadow banking growth. By itself, China accounted for nearly 30% of total shadow banking growth in 2014. Figure 4 shows that the aggregate amount of shadow banking assets in China is now approaching $3 trillion.

Figure 4 – Shadow Banking in China

Source: FSB

Interpreting the numbers for China in this report requires a bit of context. Chinese authorities did not agree with the classification of certain entity types as shadow banking (see footnote 10 in the report for more details). As a result, the numbers reported by China do not adhere to the most recent classification of shadow banking by economic functions and instead rely on an older approach that measures non-bank financial institutions engaged in credit intermediation. The result of this difference is that shadow banking in China would likely be somewhat higher if the newest methodology was used.

Within the total universe of shadow banking assets, the two fastest growing asset categories, trust companies and money market mutual funds (MMMFs), have strong links to China. Trust companies, of which China accounted for 80% of the global total, manage assets on behalf of wealthy clients, investing in bonds, equities, and making loans. The growth of MMMFs stem largely from the tremendous growth of the funds industry in China, particularly new internet-based funds such as Alibaba’s Yu’e Bao.

The FSB’s Global Shadow Banking Monitoring Report is a useful source of data in the otherwise opaque world of shadow banking. The findings in this year’s report clearly show that Asia is becoming an increasingly important player in shadow banking. As such, developments in Asian shadow banking are likely to receive greater attention from the FSB in the coming years.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.