MSCI’s decision to include Pakistan but not China and Vietnam in its Emerging Market Index has led to no small amount of confusion. However, for more careful observers of these three countries, MSCI’s rationale is more understandable. Although imperfect, Pakistan’s reforms, which include privatizations that deepen financial markets, serve as a counterpoint to Vietnam’s recent experience of greater macro stability but ambivalence toward privatization. Pakistan expects the promotion to prompt significant inflows from a new class of investors. Still, other recent experiences suggest that immediate market appreciation may moderate in the mid-term as investor enthusiasm inevitably wanes.

What Surprise?

When the initial shock of MSCI’s decision not to include Chinese local currency A-shares into its Emerging Market Index had worn off, the country suffered another indignity: Pakistan had made the cut. While the contrast between the two countries is self-evident, MSCI’s promotion of Pakistan from Frontier to Emerging Market status was not entirely surprising given Pakistan’s recent financial market and macroeconomic successes. Pakistan has attracted the attention of global investors—many of whom MSCI consults before making its decision—for some time. Interest grew after Pakistan signed an Extended Fund Facility (EFF) with the IMF in September 2013, guaranteeing the country more than $6.6bn in loans over three years. The Karachi Stock Exchange 100 Index has experienced a compound annual growth rate of about 25% since then and is up roughly 19.5% year to date.

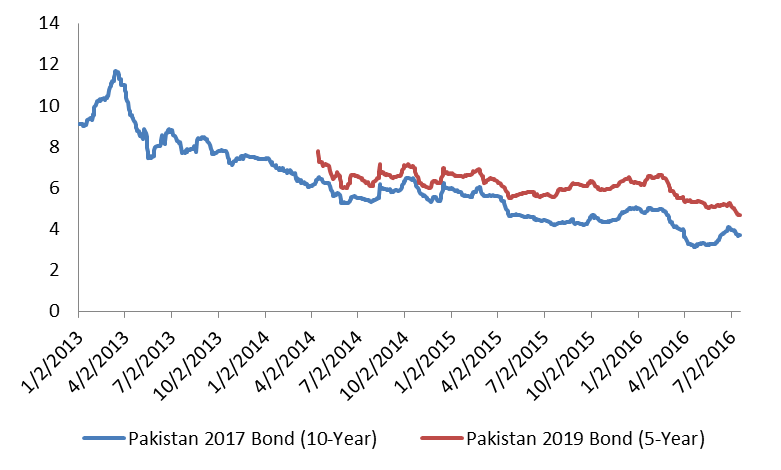

Yields on the country’s 10-year year sovereign bonds have also dropped below 4%, after hitting highs of more than 11% before the EFF program (Figure 1). Program participation also likely allowed Pakistan to issue additional debt at improved levels and to increase its foreign reserves.

No Coincidence

It was no coincidence that MSCI promoted Pakistan just as the country is completing its IMF program. Rather it demonstrates international investors’ willingness to reward Pakistan’s adherence to international financial norms and, to a lesser extent, its efforts to reform its sclerotic economy. While EFF program performance varied and the country still has work to do implementing broader reform, Pakistan has improved many headline metrics. GDP growth has inched up gradually, from 3.7% to 4.5%. The country has reduced its fiscal deficit-to-GDP from 8.5% to 4.3%; and it has accumulated reserves, nearly tripling its import cover to 4.2 months. (All figures are estimates for the end of June 2016 and are compared to figures from the last full fiscal year before the program began.)

Not All Frontier Markets Are Created Equal

In addition to MSCI’s decision on China, some observers expressed surprise that Vietnam, another Emerging Market Index aspirant, was not upgraded from Frontier Market status. After all, the country has grown rapidly at 6.5% per year since 2012 and tamed inflation. It has also been attracting ever-increasing levels of foreign direct investment thanks to productivity gains in manufacturing, and liberalizing foreign trade agreements.

But for all of its progress, reforms particularly integral to Emerging Market Index inclusion like elimination of foreign ownership limits and expanding privatization efforts have lagged. Specifically, plans to privatize state-owned enterprises often fail to meet their goals. The State Capital Investment Corporation (SCIC) recently announced it would renege on a late 2015 decision to divest from shares in 10 major Vietnamese companies, including Vinamilk, one of the country’s corporate champions. While Vinamilk does not have any foreign ownership limits in place, SCIC’s ownership stake of 45% effectively caps liquidity. Similarly, a 2014 initial public offering of Vietnamese Airlines in which only 4% of the company was sold fell short of market expectations. Even with a recent sale of 8.5%, state holdings of the company remain high. Notably, MSCI did not put Vietnam on watch for a future re-classification, a sign that it is aware of these trends and that a move may still be some time off.

Vietnamese ambivalence toward privatization contrasts sharply with Pakistan’s reform efforts. Despite the latter’s decision to cancel some privatizations due to political unrest, the country has made substantial progress on privatization. Pakistan’s sale of its minority stakes in Habib Bank Limited and United Bank Limited as part of the IMF program not only raised revenue used to hit deficit targets but also increased market liquidity and depth by releasing 41.5% and 19.8% of outstanding shares, respectively. Moreover, since the sale of those minority stakes, both companies have jumped to the top of the Karachi Stock Exchange by valuation. Both are also expected to be part of the contingent in MSCI’s Emerging Market Index when Pakistan is formally added in 2017. While Vietnam has eliminated some foreign ownership restrictions, byzantine regulations continue to confound investors and caps remain in various crucial sectors. Conversely, there are no foreign ownership limits in Pakistan.

What an Upgrade Means for Local Markets

Pakistan’s share of the Emerging Market Index will be tiny, just a fraction of a percent, compared to the 8.97% it represented in the Frontier Market Index. Still, the move is expected to increase inflows into Pakistan by about $400 million over the next year, according to an average of various investors’ expectations. Pakistan’s markets are changing in status from a big fish in a small pond to a small fish in a big sea. The country will begin attracting inflows from funds whose risk tolerance previously prohibited investment in frontier markets.

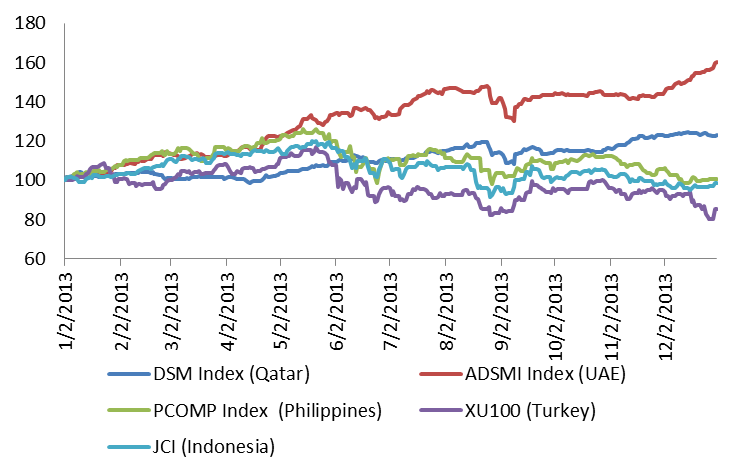

The reclassification is surely no guarantee of a sustained market ascent. For example, both the UAE and Qatari stock markets advanced after MSCI announced their reclassification from Frontier to Emerging Markets in June 2013, even as other emerging markets experienced a downturn during the so called ‘Taper Tantrum’ (Figure 2). However, the pace of increase moderated once the euphoria wore off. Pakistan may follow suit. The country will likely become more correlated with advanced markets as the reclassification allows conservative investors to treat Pakistan like other countries in their broader emerging market allocations.

Moreover, while the MSCI grouping may be indicative of how countries are aligned by various criteria like liquidity, it represents just one of many authorities. The Van Eck Vietnam ETF, which allows investors to bet on a broad range of investable securities in that country, is another metric. The Vietnam ETF has a market cap almost 50 times greater than a similar ETF dedicated to Pakistan. The disparity suggests that at least some investors are not restricted by formal designations and that they favor Vietnam over Pakistan.

Pakistan’s recent MSCI upgrade and its soon-to-be successful completion of an IMF program, therefore, highlight just one path for frontier financial market development. Apparent investor preference for Vietnam over Pakistan despite MSCI’s decision not to grant Vietnam a similar upgrade shows that stock index categorization may serve to legitimize a market and bestow prestige, but it is not necessarily the best indicator for investor sentiment. Global investors consider a broad range of indicators in considering where to deploy their capital. For frontier and emerging markets conducting financial market reform, the challenge is more complex than an index upgrade might imply.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.