Remittances exceeded $600 billion worldwide in 2015, with more than two-thirds going to developing countries. Developing Asia receives more remittances than any other region—roughly $200 billion—and in some countries remittances even exceed foreign direct investment inflows. Meanwhile, innovations in payment systems can reduce remittance fees dramatically, increasing the earnings sent back to migrants’ friends and families—and supporting economic growth in Asia.

Remittances are Big in Developing Asia

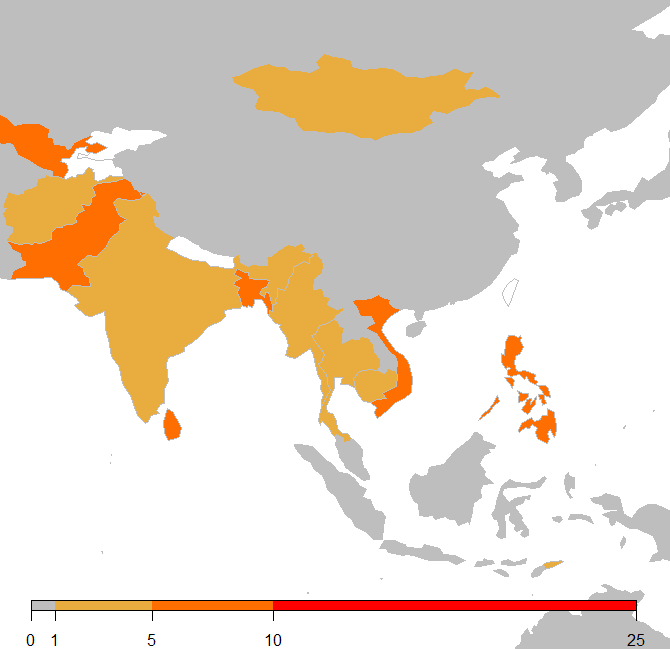

Remittance inflows represent a substantial source of income for emerging Asian economies (see Figure 1 and Table 1). Countries like India and the Philippines receive larger flows from remittances than foreign direct investment, bringing in foreign currency to improve the balance of payments. The Philippines is perhaps the country most famous for its emigrant workers and nearly 10% of its GDP is composed of remittances. Nepal, a low income country with a large proportion of overseas workers, gets nearly 30% of GDP from remittances, the largest share in Asia. In 2014, India had the highest gross level of remittance flows in the world at over $70 billion, and China was not far behind at over $62 billion, although remittances play a smaller role in its larger economy.

Table 1: Asia’s Remittance Inflows

| Country | US$ Billions | % GDP |

|---|---|---|

| India | 70.4 | 3.4 |

| China | 62.3 | 0.6 |

| Philippines | 27.3 | 9.6 |

| Bangladesh | 15.0 | 8.7 |

| Vietnam | 12.0 | 6.4 |

| Sri Lanka | 7.0 | 8.9 |

| Nepal | 6.6 | 29.2 |

| Korea, Rep. | 6.6 | 0.5 |

| Thailand | 5.7 | 1.4 |

| Japan | 3.7 | 0.1 |

| Myanmar | 3.1 | 4.8 |

| Malaysia | 1.6 | 0.5 |

| Mongolia | 0.3 | 2.1 |

Source: World Bank

High Fees Add Up, but Alternative Payment Methods Can Lower Costs

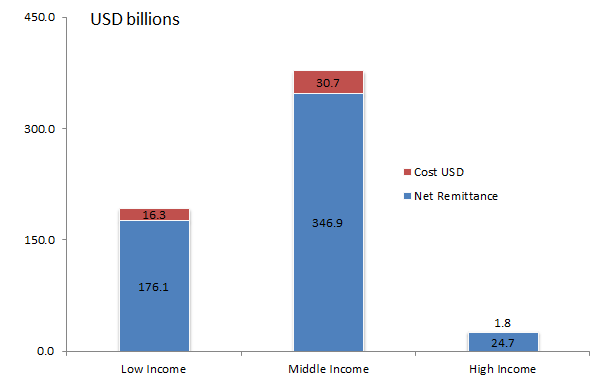

While remittances contribute substantially to Asia’s economy, they typically generate high transaction costs that reduce the benefit to recipients. Across all low and middle income countries, 2015 remittance costs totaled roughly $47 billion (see Figure 2). According to World Bank data, on average remittances to East Asia cost 8.5% of transaction value as of the second quarter 2016. Remittance fees to South Asia are notably less expensive at 5.6%.

Commercial banks offer the most expensive form of remittance payment with an average total cost of 11.3%, and fees on remittances to Asia remain high in part because of continued dominance of bank-based transfers. In contrast, mobile payment services charge roughly 4.1% transaction fees according to World Bank data, more than 50% cheaper than the average rate in East Asia.

More notably, while mobile and other digital payment methods receive increasing attention—often under the guise of “fintech” innovations—the cheapest form of remittance measured by the World Bank relies on basic pre-paid cards. Using this method, an overseas worker typically funds a pre-paid card for a friend or family member back home. As of the latest period, transaction fees for pre-paid cards were only 1.69%, nearly 60% cheaper than the next best mobile option.

Some new fintech firms charge even less for international transfers with flat fees of several dollars. However, these rates are frequently offered to gain market share and may be unsustainable over the long run. Either way, the fact that more conventional pre-paid card transactions already save users so much shows significant room for fee reductions and implies existing financial technology already has the potential to have a major impact.

For now, average remittance fees remain high in part because many of the world’s poorest lack access to even basic non-cash financial services that make cheaper options like pre-paid cards useful. This underscores the need for broader coordination of financial inclusion efforts as part of economic development to assist the poor. As more people in developing countries gain access to basic non-cash financial services, opportunities to reduce cost should expand.

Of course, there are a number of regulatory and legal reasons why some international payments are more expensive. For example, commercial bank transfers require banks to verify that parties are not remitting funds for illicit reasons (e.g. to launder money, finance terrorism, or conduct other criminal activity). Still, regulators can craft similar rules for issuers of pre-paid cards, and the U.S. Treasury Department’s Financial Crimes Enforcement Network created new regulations in 2011 to ensure such issuers implement anti-money laundering programs, report suspicious transactions, and track customers that purchase large volumes of cards. Whether such regulations materially increase costs of this remittance method is unclear, but the existing cost differential is so great that pre-paid cards are almost certain to remain far cheaper than bank-based transfers.

Lower Fees, More Income

If transaction fees on remittances could be reduced to 1.5% (roughly the rate for pre-paid card transactions), the gains for emerging Asia would be significant. In the Philippines, reducing remittance fees by several percentage points could put nearly $1.5 billion more in recipients’ pockets, roughly 0.5% of GDP and double the level of development assistance the country received from the World Bank in 2015. India could save over $3 billion, again more than its development assistance from the World Bank. As remittances frequently go to a country’s poorest citizens, who stand to benefit the most from each marginal dollar, the potential impact of reduced transaction costs is even larger.

With remittance flows to developing Asia expected to grow 4% over 2016-2017, lowering transaction costs by expanding the use of less expensive payment methods is low-hanging fruit for Asian policy makers that want to boost welfare, increase consumption, and improve financial inclusion. Innovations in fintech promise to drive traditional competitors to lower prices, but even if start-ups cannot sustain minimal transaction fees, the reasonable costs of conventional payment methods like pre-paid cards offer a realistic way forward.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.