China’s money market is growing rapidly and playing an increasingly important role in the financial system. It serves as both a key channel for monetary policy and as a source of funding for a variety of financial institutions. In the past, smaller banks have been net borrowers in the interbank market while large banks have provided funding. However, recent data reveals a shift underway as non-bank financial institutions have emerged as the largest borrowers. This change has important implications for the development of China’s financial system.

The money market is part of the interbank market, which also includes a large bond market. Operation of the interbank market is managed by the National Association of Financial Market Institutional Investors (NAFMII), a self-regulatory organization which operates under the supervision of the People’s Bank of China (PBoC) and whose members are financial institutions. Trades are matched via the electronic order system operated by the China Foreign Exchange Trading System (CFETS).

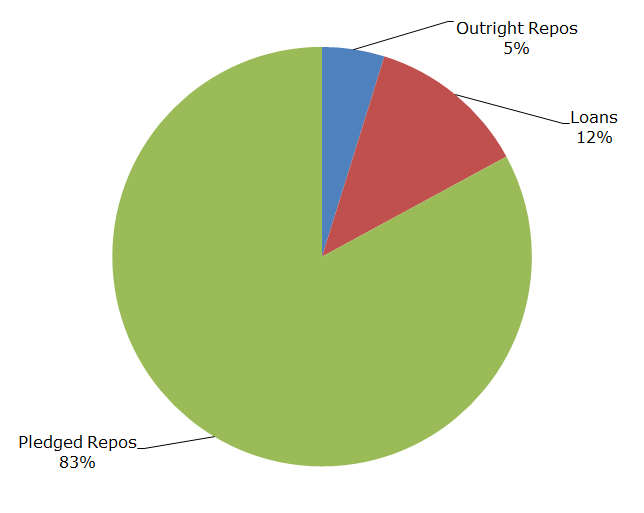

As Figure 1 below shows, the primary instruments traded in the money market are pledged repurchase agreements (repos), followed by interbank loans and outright repos.1 The repo market dwarfs the lending market because a wider variety of financial institutions and entities are allowed to participate. Instruments with overnight and seven-day maturities account for 96 percent of the total market.

Liquidity management within the money market is a work in progress. In the summer of 2013 interbank rates spiked dramatically. At one point, overnight rates soared to 30 percent, compared to rates that are typically in the low single digits. The spike in rates was due to a variety of factors, including seasonal liquidity fluctuations, growing reliance of medium and small-sized banks on short-term funding, and a reported decision by the People’s Bank of China to withhold liquidity in order to discipline excesses in the money market. The spike in rates and rumors of interbank defaults contributed to a general panic that persisted until the PBoC reassured the market via a series of strong public statements.

Following the 2013 interbank credit crunch, the level of volatility in the money market has been lower. This is due to a mixture of greater awareness of banks of the potential risks of reliance upon wholesale funding, a switch to reserve averaging for the calculation of bank required reserves, as well as active use of an expanded tool set by the PBoC to manage liquidity conditions. Table 1 shows the range of tools the PBoC now employs to add or subtract liquidity from the market:

Table 1 – PBoC Liquidity Management Tools

| Name | Description | Date Introduced |

|---|---|---|

| Short-term Liquidity Operations (SLO) | 1 to 7 day direct lines of credit to select banks. | 2013 |

| Standing-Lending Facility (SLF) | 7 day to 3 month loans to banks contingent upon the provision of high quality collateral. | 2013 |

| Medium-term Lending Facility (MLF) | Medium-term loans to banks contingent upon the provision of high quality collateral. | 2014 |

| Pledged Supplementary Lending (PSL) | Long-term loans provided to policy banks that are directed towards specific sectors. | 2014 |

| Daily Open Market Operations (OMO) | Repos and reverse repos sold in the money market. | 2016 |

Following the removal of controls on deposit rates, the central bank has frequently intervened in the money market to guide rates. The PBoC has established an “interest-rate corridor” with the floor being the rate paid on excess bank reserves and the ceiling set by the SLF. This represents a significant step towards a more market-based interest rate formation mechanism.

In addition to its increased policy role, the money market continues to grow as a source of funding. Between 2014 and 2015, the renminbi value of transactions in the money market grew by 99 percent. Growth continued in the first half of 2016 as well, with transactions increasing by another 64 percent compared to the first half of 2015. In contrast, renminbi loans grew by about 14 percent during the same period.

Excluding the activities of the PBoC, the large banks2 are by far the most significant providers of liquidity in the interbank market. In the repo market, the large banks are the only net providers of funding, with a variety of other types of financial institutions acting as borrowers.

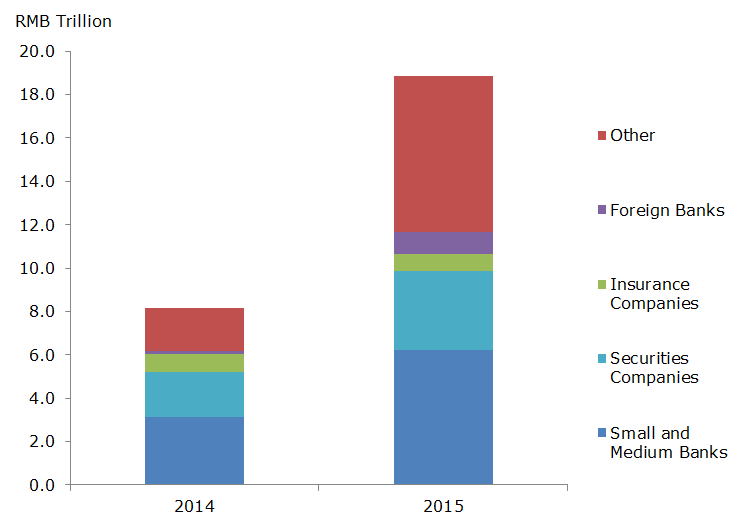

Amongst the borrowers, small- and medium-sized banks have traditionally been the biggest recipients of funds in the repo market. This changed last year, when there was a large increase in borrowing in the “Other” category (Figure 2). Between 2014 and 2015, “Other” grew from 24 percent to 38 percent of the total value of borrowing. This trend accelerated in the first half of 2016, with “Other” now accounting for more than 50 percent of total borrowing.

The “Other” category is a catch-all that includes credit cooperatives, finance companies, trust companies, financial leasing companies, asset managers, mutual funds, and off-balance sheet vehicles like trust and wealth management products. Many of these entities are using access to low cost and plentiful funding in the repo market to take on leverage and increase yield.

For example, asset managers can purchase bonds and then use those bonds as collateral in the repo market. Funds can then be borrowed from the repo market and used to purchase additional bonds. This use of short-term repo funding for longer-term and risky investments can be problematic. Short-term borrowing from the money market will need to be rolled over multiple times while it may take months or years to receive returns from longer-term investments.

This type of maturity mismatch can be a source of problems during periods of financial stress. Funding markets can quickly freeze up and non-bank borrowers lack access to the central bank as a lender of last resort. Events in the United States and other countries have shown the risks that can arise when non-bank borrowers are dependent on wholesale financing. The increase in leverage has also stoked fears that rapid growth in the bond market is unsustainable.

The growing importance of these non-bank entrants to the Chinese money market seems likely to increase given recent policy moves. In May 2016, the PBoC expanded the list of entities permitted to have their own independent trading accounts in the interbank market, adding housing provident funds, pension funds, charities, and all bank-sponsored wealth management products.

China’s rapidly developing money market is now playing a key role as both a source of funding and a channel for monetary policy. Concurrently, there has been a significant increase in non-bank borrowers in the money market. This presents new risks as non-banks are often less adept than conventional banks in managing the risks inherent in maturity transformation. This development is therefore worthy of close monitoring.

1. With pledged repos, borrowers register and pledge their collateral but maintain ownership over it. Outright repos involve a transfer in ownership of the collateral for the duration of the repo.

2. Industrial and Commercial Bank of China, Agricultural Bank of China, Bank of China, China Construction Bank, China Development Bank, Bank of Communications, and Postal Savings Bank of China.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.