The chaotic aftermath of India’s recent demonetization shows how crucial cash remains to daily life in developing countries. The disruption also exposed the technological barriers to the transition to a less cash-dependent economy. As the Indian government announces further incentives for cashless payments, the demonetization shock may also jumpstart existing policy efforts to develop a more digital economy.

Cash or…Cash?

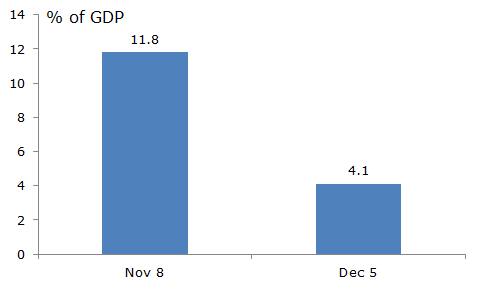

Following the Indian government’s decision to demonetize outstanding INR 500 and 1000 ($7.50 and $15.00) notes on November 8, people rushed to their banks to swap existing currency. Without adequate circulation of new bills to replace the demonetized notes, the result was huge shortages of cash. As of December 5, a month later, the effective cash in circulation had fallen from 11.8 percent of GDP to 4.1 percent, dropping by nearly two-thirds (see Figure 1). Meanwhile, cash equivalent to 2.5 percent of Indian GDP had been exchanged, creating a huge logistical challenge over such a short period. An equivalent scenario in the United States would involve every American exchanging roughly $1,400 in cash with one month.

The demonetization policy disrupted economic activity for the majority of Indians who exclusively use cash in their daily lives (98 percent of transactions are cash based according to one estimate). Recent surveys indicate roughly 90 percent of Indian citizens receive their wages in cash, for example, while nearly two-thirds hold cash savings at home. It follows that much of their spending is also conducted in cash, as they pay each other for goods and services, or even send money home (much of India’s domestic remittance payments involve cash). The dramatic decline of cash in circulation has even forced some Indian businesses to resort temporarily to a barter system and, in some cases, use hand-written IOUs.

As a result of the shock, a number of analysts expect a significant drag on near-term growth, with some estimating as much as one percentage point (roughly $200 billion) could be shaved off India’s current year growth. One notable countervailing effect has been a dramatic fall in India’s interbank interest rates, notable as rates in other emerging market countries have generally increased since the U.S. presidential election. The rapid increase in bank liquidity created by the surge in deposits following demonetization has contributed in part to the RBI’s latest decision to hold its policy rate steady amid prior expectations for a rate cut.

One justification for the government’s implementation of an unexpected and rapid demonetization was to curb illegal activity and corruption, typically funded in cash. As of December 3, 82 percent of the old bills had already been deposited at banks, with one month to go before banks stop accepting the bills. The rapid return of so many old bills implies the extent of illegal activity may be more limited than previously estimated, as depositors of old bills have de facto declared their previously hidden savings. Of course, those seeking to avoid government detection and taxation also likely have more sophisticated techniques for laundering their ill-gotten gains and storing their wealth in alternative assets like gold, foreign currency, and real estate. The rapid exchange of old bills also reflects the large role of India’s informal cash-based economy, the so-called “grey market” which is neither tracked nor taxed by the government.

“Less Cash” on the Long Road to a Cashless Economy

Following demonetization, Prime Minister Narendra Modi emphasized a near-term shift to a “less-cash economy” as the country eventually transitions to truly “cashless.” Over the past decade the Indian government and Reserve Bank of India have undertaken a number of policies to make the economy less reliant on cash transactions. This has included improvements to the electronic payments infrastructure, the provision of hundreds of millions of new payment-capable accounts to the unbanked, and the encouragement of new payments technology and innovation by non-traditional firms. The government has clearly tied efforts to move beyond cash to broader financial inclusion goals, instituting clever programs like direct benefits transfers—which deliver government benefits payments electronically—to encourage citizens to use their newly created accounts.

A common challenge to efforts to digitize economic activity in developing countries is underutilization of new infrastructure. People receive new digital accounts but simply use them to cash out and then conduct cash-based transactions as usual. With hundreds of millions of Indian citizens only just receiving new digital accounts, many of them continue to prefer cash. Indeed, as of August 2016, roughly 25 percent of new government-provided accounts held a zero balance, a number likely understated given allegations that bankers pad accounts with a single rupee to avoid detection. The preference of Indian consumers for cash is only natural given many small businesses are unable to conduct electronic transactions or unwilling to do so given a desire to evade tax payments.

To give electronics payments an additional push, the government has long considered providing additional incentives to digital payments. With the roll-out of demonetization showing how vulnerable many are to cash shortages, the government has recently announced a series of subsidies for those making cashless payments for purchases like gasoline, train tickets, government services, and even life insurance. Separately, it will indefinitely waive service taxes on digital card transactions up to INR 2,000 in value (equal to the highest-denomination new note). Meanwhile, as of the first nine days of December, more people had used a new government-backed, smartphone-based cashless payments system than in all of November. Digital payments providers are also seizing the opportunity to market their services.

Even with these good intentions, any immediate pick-up in digital payments is most likely to be seen in urban areas, where ownership of mobile phones is widespread and merchants more readily accept non-cash payments. Indeed, the countryside has been hardest hit by demonetization. With an estimated 50 percent of rural residents still lacking a mobile phone, the government will rely on payment cards—delivered through new bank accounts—and the roll-out of so-called microATMs, mobile point-of-sale terminals, but the progress will be slower.

All of these efforts will take years to unfold. While the Indian government is building a robust infrastructure for non-cash payments and reinforcing its use with broader financial inclusion efforts, uneven access to technology and old habits will make the transition challenging. It may take jolts like the demonetization policy to overcome these hurdles and push India into the digital era.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.