Nearly six months after India’s momentous demonetization, the government continues to expand options for digital payments to reduce the economy’s dependence on cash. While old habits die hard, recent data show that new digital payment methods are building momentum. These innovations offer simple, universal tools that may help India leapfrog older technology to reach a less cash-intensive future.

Non-cash Payments Resilient after Demonetization Surge

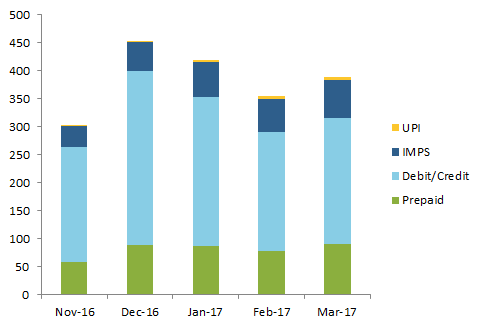

Non-cash payments saw a surge immediately following the demonetization policy enacted in November 2016, when cash in circulation fell by two-thirds. Digital transaction volumes grew 43 percent between November and December 2016, driving hopes that the shock would kick-start India’s transition to a cashless economy. Still, with roughly 98 percent of consumer transactions reliant on cash prior to demonetization, it was inevitable that most Indians would return to cash once new bills were in wide circulation. Growth in digital payments did indeed slow in the first two months of 2017, but the latest March data indicates that the shift from cash is still underway, with an overall increase in digital transactions of 33 percent by volume and 59 percent by value since November 2016. The government will likely fall short of a targeted 25 billion cashless transactions over the coming fiscal year ending March 2018, but if robust monthly growth over 7 percent continues, India could see 2 billion monthly transactions by this time next year.

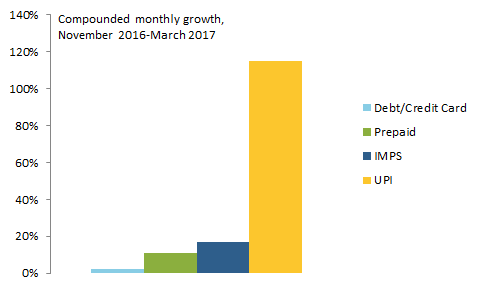

The data illustrate a decisive move towards new mobile-based payment methods, with older forms of non-cash payment, like debit and credit cards, showing less uptake (see Figure 1). Card payments spiked 51 percent in December 2016 before declining in the following months, with latest data showing them up a modest 10 percent overall since demonetization. Recent financial inclusion efforts have substantially increased payment cards to 869 million as of the end of February, yet monthly card transactions averaged 244 million over the past few months. This means the vast majority of cards are dormant. By comparison, according to 2015 data from the Federal Reserve, Americans made an average of 8.6 billion card transactions per month, more than 40 times the recent Indian average despite a U.S. population roughly one-quarter India’s size.

Payment cards, long ubiquitous as cash alternatives in the developed world, have had uneven success in India due in part to the limited number of point-of-sale (PoS) terminals that make cards useful. Such payment infrastructure is particularly lacking in the countryside because, at least according to payment operators like Visa, their cost is greater than the transaction fees the market can support. India’s Secretary for Information Technology stated the government is targeting the addition of 2 million new PoS terminals by September 2017. However, even if this goal is met, newer digital payment tools offer a cheaper, simpler alternative.

Newer Digital Payments May Leapfrog Cards in Replacing Cash

The most notable surge in cashless payments has taken place over infrastructure introduced over the past several years. Both the Immediate Mobile Payments System (IMPS) and the United Payments Interface (UPI), which support instant payments using mobile phones, have grown substantially since demonetization, even as cash has returned to the economy (see Figure 2). Though a full account of demonetization’s impact on digital payments will require more data over a longer time period, the early results suggest the policy could be providing a well-timed catalyst for non-cash payments growth.

IMPS and UPI themselves provide the infrastructure for a variety of promising new payment applications. The recently launched Bharat Interface for Money (BHIM) is a government-sponsored app for digital transactions that leverages the UPI to provide a uniform option for anyone in India with a bank account and smartphone. It eliminates the need for proprietary bank apps and intermediary transfers between a user’s bank and third-party mobile wallets, saving time and lowering transaction fees. It also allows users with Aadhaar cards—India’s universal identification—to pay a recipient with an Aadhaar number, offering an additional synergy with hundreds of millions of new Aadhaar-enabled bank accounts. As with India’s array of other digital payments options, a challenge for BHIM will be to establish a broad network of users, including vendors that accept payments using the system.

To complement BHIM, in February 2017 the National Payments Corporation of India launched BharatQR Code, an intermodal system for payments that eliminates the need for point-of-sale terminals in consumer transactions and moves the country beyond proprietary Quick Response code systems previously operated by card and mobile wallet companies. Under instruction from the RBI, the National Payments Corporation of India (which runs the national RuPay card network), Mastercard, Visa, and American Express collaborated on the system. It allows customers to pay participating merchants by scanning a unique QR code with their smartphone camera, with no technology required on the seller’s end.

What makes both BHIM and BharatQR programs promising is their interoperability. Users can pay for goods or services using the new BHIM app, other UPI-enabled apps and mobile wallets, or debit and credit card accounts, which can all link to the system. On the seller side, merchants need only register with a bank to receive payments.

The constraining factor for BHIM and BharatQR will be the still incomplete adoption of smartphones, since both systems require cameras and up-to-date operating systems. As of mid-2016, India was the second largest smartphone market in the world with an estimated 275 million devices, but penetration is still low at less than 30 percent of the population. The country is expected to add an additional 350 million smartphone connections by 2020 according to the GSM Association. To fill the gap for now, India has launched a separate system, popularly known as *99#, which allows residents to make payments using SMS with their basic mobile phones. While still small in overall volume, this system has also seen dramatic growth since demonetization.

Only time will tell, but these innovations could be the glue that brings together an effective digital payments system in India. Leading international technology firms seem to agree, with Alibaba a major investor in Indian mobile wallet firm Paytm and Facebook’s WhatsApp planning to launch its own digital payments service.

India’s Experiment Could Lead the Way for Other Markets

In the long run, the roll-out of these new programs could move India beyond not just cash, but also older payment technologies like debit and credit cards. With the introduction of simple and interoperable tools like BHIM and Barat QR Code, India may have its best opportunity to develop a broad national network for digital payments that are cheap, convenient, and accessible to everyone, rich and poor, urban and rural. The light footprint of QR codes combined with the nudge of a government-sponsored interoperable app could even provide a model for other countries looking to stimulate digital payments.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.