Japanese investors have long been known for their overseas investments. Following the 2013 onset of the Bank of Japan’s extraordinary monetary policy, the country’s pace of overseas investments has accelerated even further. While Japanese investors have been buying assets around the world, several Asia-Pacific countries have experienced particularly large capital inflows, exposing them to future changes in Japan’s economy and monetary policy. Among them, Thailand and Australia stand out as having high exposure to Japan.

The World’s Creditor

Japan has been the world’s largest creditor for 26 years, with net foreign assets in excess of $3 trillion—roughly 75 percent of GDP—as of the end of 2016. Historically a country with a high savings rate, Japan has tended to export excess savings in many forms. Its banks, which have yen deposits in excess of domestic loan demand, turn to overseas markets with stronger economic growth and higher interest rates. Other institutional investors like insurers and mutual funds also look abroad for more attractive yields in their portfolios, particularly in the face of negative domestic interest rates. Meanwhile, Japanese corporations have established complex global supply chains over the past several decades, increasing Japan’s large stock of foreign direct investment (FDI).

Thailand Banks on Japan

As previously covered in Pacific Exchange, over the past five years Japan’s banks have re-taken the global lead in cross-border lending with a focus on the Asia-Pacific. Several countries in the region are now particularly reliant on Japanese loans among their various international bank borrowings. Most prominent is Thailand, where Japanese lending represents nearly two-thirds of all foreign bank lending and 20 percent of GDP (see Table 1). Japan’s large share reflects its strong economic ties to Thailand, a major base for overseas Japanese manufacturing, but it also makes Thailand sensitive to future changes in Japan’s economy. Thailand’s reliance on Japanese banks increased notably in 2013 as Mitsubishi UFJ Financial Group, Japan’s largest bank, acquired a 75 percent stake in Thailand’s fifth largest bank, the Bank of Ayudhya (now renamed Krungsri Bank).

Table 1: Japan’s Share of Foreign Bank Claims in the Asia-Pacific (% of Global Total)

| Country | Japanese Claims/Total Foreign Claims | Japanese Claims/GDP |

|---|---|---|

| Thailand | 64.74% | 19.19% |

| Australia | 26.92% | 8.91% |

| Philippines | 25.97% | 3.21% |

| South Korea | 23.36% | 4.23% |

| Indonesia | 22.01% | 2.57% |

| Taiwan | 16.62% | 5.55% |

| Vietnam | 16.62% | 2.87% |

| Malaysia | 16.38% | 7.90% |

| India | 15.61% | 1.64% |

| Singapore | 15.54% | 19.49% |

| China | 10.62% | 0.63% |

| Hong Kong | 9.67% | 21.28% |

Roughly half of Japanese banks’ local claims on Thai borrowers are denominated in foreign currency.1 While full data is not available on the currency composition of such borrowing, it is almost certainly primarily in the form of Yen and US dollars. Any movement in overseas interest rates and foreign exchange rates could have an outsized impact on Thailand vis-a-vis other regional peers. Of course, Thailand has substantial foreign exchange reserves, with coverage of external debt in excess of 100 percent. This compares to a figure under 25 percent in 1997, when a sharp depreciation of the Thai Baht helped trigger the Asian Financial Crisis as indebted Thai borrowers found it difficult to re-pay foreign currency-denominated loans.

Other Asia-Pacific countries with large shares of Japanese lending include Australia, the Philippines, South Korea, and Indonesia, each with more than 20 percent of foreign borrowing from Japan. Like Thailand, Australia relies heavily on foreign borrowings, which represent roughly one-third of GDP.

Australia Offers Shelter from Negative Rates

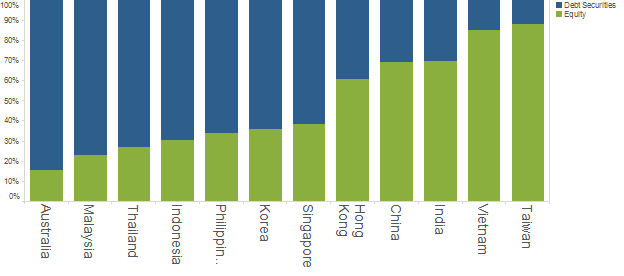

Australia warrants additional attention given its high share of Japanese portfolio investment from Japan. Though Japanese portfolio investments in equities and bonds flow across the region, Australia stands out for receiving roughly 16 percent of its investments from Japan (see Table 2), nearly twice the share of the next most popular destination, Singapore.2 Japanese investment is heavily weighted towards long-term bonds, roughly 85 percent of all its portfolio investment in Australia. Japan’s portfolio investments are also primarily in debt securities in developed economies like Singapore and South Korea and emerging markets like Indonesia and the Philippines. In other countries in the Asia-Pacific, they are more strongly weighted towards equity (see Figure 1). Australian government bonds are of particular interest to Japanese investors, accounting for roughly one-third of their fixed income investment in the country in 2016. This preference reflects Japanese investor interest in relatively safe, higher-yielding fixed income investments amid negative rates at home.

Table 2: Japan’s Share of Portfolio Investment in the Asia-Pacific (June 2016)

| Country | Japanese Portfolio Percentage of Global Investment |

|---|---|

| Australia | 16.20% |

| Singapore | 8.56% |

| Thailand | 8.30% |

| Korea | 6.23% |

| Indonesia | 6.22% |

| Malaysia | 5.67% |

| Hong Kong | 5.14% |

| Philippines | 4.10% |

| Taiwan | 3.33% |

| India | 2.51% |

| China | 2.05% |

| Vietnam | 2.00% |

Figure 1 – Japan’s Portfolio Weights in the Asia-Pacific (June 2016)

Though portfolio flows may offer attractive financing alternative to banks, they can have a downside for recipient countries. Foreign portfolio investors are generally the quickest to leave a market during times of volatility. In the lead-up to the global financial crisis, Japanese investors also held large positions in Australian debt in order to take advantage of yield differentials. These positions were un-wound during the crisis. The resulting outflows led the Australian dollar to fall nearly 50 percent against the Yen to its lowest point since the end of World War Two, prompting the Reserve Bank of Australia to intervene.

Japanese FDI is Substantial, but Sticky

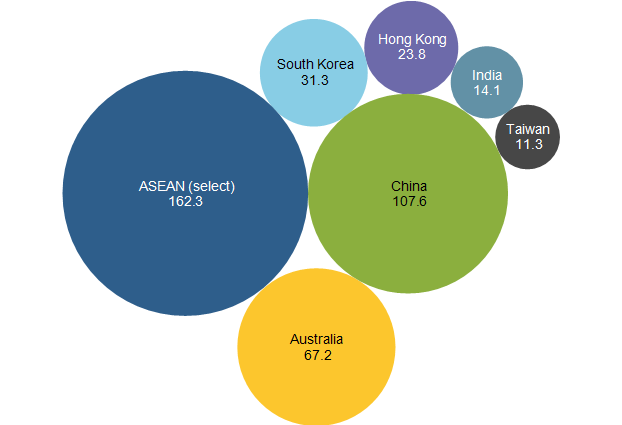

Japanese firms’ complex global supply chains lead them to make foreign direct investments in locations around the world. The Asia-Pacific is no exception, with countries like China, Australia, and the Association of Southeast Asian Nations (ASEAN) all receiving large investments from Japan (see Figure 2). In total, roughly 40 percent of Japanese FDI resides in the Asia-Pacific according to OECD data. FDI flows tend to be less volatile than banking and portfolio flows given their support of fixed assets and other long-term economic activity. Their value is also less tied to interest rates than investments like stocks, bonds, or loans. Still, long-term trends in FDI are influenced by exchange rates. In fact, as the Yen weakened following the onset of the BOJ’s unconventional policies, some Japanese manufacturers found manufacturing back in Japan more competitive (the United States has seen a similar trend in some technology-intensive industries).

ASEAN data reported for Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam

Monitoring Risks from Cross-border Exposure

Japan’s outbound capital flows are a source of growth for the country’s overall wealth and have helped finance a number of Asia-Pacific economies over the past several decades. Still, just as Japan’s overseas investment expanded amid extraordinary monetary policy at home, it can also contract, exposing the region to future changes in Japan’s economic environment. To paraphrase an old economic saying, if Japan sneezes, the Asia-Pacific may catch a cold.

End notes

1. According to Bank for International Settlements reporting conventions, local claims are a sub-set of foreign claims that exclude cross-border lending made by affiliates outside of the recipient (“local”) country.

2. The United States receives a similar share of Japanese portfolio investment as a proportion of overall foreign portfolio stocks.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.