Following a slowdown in credit growth and weakening corporate sector performance, nonperforming loans (NPLs) in China started to grow rapidly in 2011. While this has led to renewed concerns over financial stability, according to official figures the pace of bad loan creation has actually slowed recently. Banking sector NPL growth decelerated notably from 51.2 percent in 2015 to 18.7 percent in 2016. The NPL ratio stood at 1.74 percent as of Q1 2017, nearly unchanged from the previous two quarters. Special mention loans—those in the pipeline that can potentially become nonperforming—now represent 3.77 percent of total loans, down from 4.10 percent in Q3 2016.

Cleaning up banking sector stressed loans

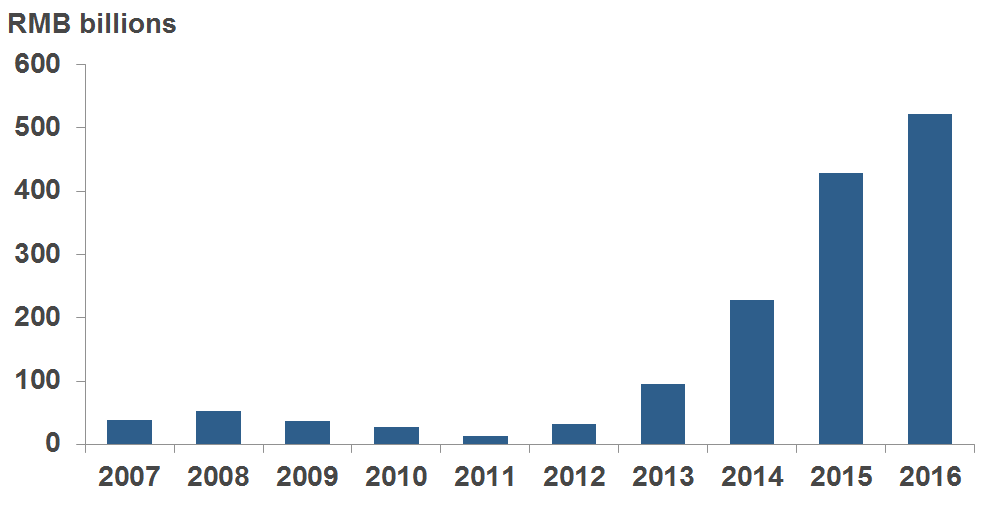

The moderate improvement in the bank asset quality metric partly reflects recent efforts to resolve distressed loans in the banking sector.1 China’s Ministry of Finance (MoF) relaxed rules regarding loan write-offs in 2010 and 2013 that removed some barriers (mainly due to tax treatment reasons) for timely NPL disposal. From 2014 to 2016, publicly listed large and joint-stock banks collectively wrote off RMB 1.18 trillion (US$ 183 billion) in bad loans, compared to only RMB 258 billion in the six years from 2008 to 2013, according to SNL data (Figure 1). Looking at a sample of 762 institutions, UBS estimates that Chinese banks raised a total of RMB 1.8 trillion between 2013 and 2015 to strengthen their financial position.

Beyond loan write-offs, authorities have launched a series of new programs to encourage banks to repair their balance sheets. The most important such program so far is the licensing of local asset management companies (AMCs), often dubbed “bad banks” by industry analysts. Previously, China established four large AMCs in 1999 to takeover problem assets from the four largest state-owned banks. In January 2012, a notice jointly issued by the MoF and the China Banking Regulatory Commission (CBRC) allowed for the creation of new province-level AMCs to resolve bad loans in their respective provinces. In 2013, Jiangsu Asset Management Company became the first such local “bad bank.” According to UBS, China has a total of 35 local AMCs as of January 2017, with another five awaiting approval. These AMCs collectively have RMB 94 billion in registered capital. Assuming capital adequacy ratios of 12.5 percent, the local AMCs have an initial capacity large enough to purchase roughly RMB 750 billion in bad assets from banks, or roughly half of outstanding banking sector NPLs (and more if one assumes they can recycle capital after resolving an initial batch of bad loans).

Another program, much smaller in magnitude, is NPL securitization, which allows banks to transform a diversified pool of NPLs into securities that qualified investors can purchase. A pilot NPL securitization program was established in early 2016 with an aggregate quota of RMB 50 billion. In 2016, six participating large banks issued RMB 15.6 billion in nonperforming asset-backed securities. Chinese news media reported that some joint-stock banks and city commercial banks will join this program in 2017. NPL securitization offers banks the flexibility to quickly dispose of small amounts of their most problematic loans (such as credit card loans) that they are not able to sell to the AMCs, as these companies typically prefer large loans with relatively high recovery rates in order to control servicing costs.

Debt restructuring programs

Meanwhile, in view of the persistent corporate debt overhang, Chinese authorities formally launched the Debt-to-Equity Swaps (DES) program in October 2016 after several months of heated public debate. By design, these appear to be essentially debt restructuring arrangements for viable companies with a high debt burden, whereby banks transfer loans to special purpose vehicles (SPVs) to be converted to equity. DES deals already announced differ from each other in timeline, deal structure, and risk sharing arrangements. In some already announced deals, banks reportedly have issued wealth management products (WMPs) to fund their subsidiary SPVs, channeling household and corporate savings to invest in underlying problem assets. According to the CBRC, participating banks have announced a total of RMB 767.2 billion in DES contracts as of April 2017. But of this amount, only a small fraction—roughly RMB 59.2 billion in debt—has been converted to equity and the rest is still in process.

The CBRC has also attempted to address potential problem loans in the pipeline through the widespread establishment of creditor committees, which consist of multiple bank lenders to coordinate credit extension and debt restructuring of troubled corporates with high debt burdens. According to a senior CBRC official, China had established 12,836 creditor committees by end-2016, to help manage credit of RMB 14.85 trillion, or more than 15 percent of banking sector loans.

Industry analysts suspect that banks will end up doing a lot of the heavy lifting in most debt restructuring programs. The priority of these programs is to relieve debt burden for viable corporate borrowers. Banks can potentially benefit when borrowers are able to achieve successful turnarounds, but will also likely experience losses and face higher capital requirements for their involvement in these programs compared to simply disposing of the bad loans.

Challenges for Chinese banks

Tackling stressed loans in a swift and decisive manner and encouraging corporate sector deleveraging will help stem systemic risks in China. Conversely, the failure to take prompt action will likely result in higher clean-up costs down the road, as shown by the experience of many other economies. In China’s case, the magnitude of the new NPL resolution and debt restructuring programs conveys a sense of urgency felt by the authorities. While these programs aim at strengthening the banking sector in the long run, they will likely further weigh on bank earnings and capital levels in the near-to-medium term. Given lackluster corporate sector performance and persistent overcapacity, new NPL formation will also remain a substantial challenge for China’s banking sector going forward.

1. However, stressed assets held by the so-called shadow banking sector remain a significant concern for many industry analysts.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.