In 2017, natural disasters caused $306.2 billion of damage nationally. From raging wildfires in Northern and Southern California to mudslides along the Central Coast, let alone the persistent threat of earthquakes and drought, the West Coast is no stranger to natural disasters. Yet little is known about the impacts of natural disasters on small businesses, which are a critical engine of the American economy and are responsible for creating two out of three new private-sector jobs. A new report from the SF Fed in partnership with the Federal Reserve Banks of New York, Richmond, and Dallas fills this gap by examining data from the latest round of the Federal Reserve System’s Small Business Credit Survey and provides insight on the impact of natural disasters on small businesses and their related needs.

Report Findings

Access to small loans and grants is key to small business survival after a disaster. The report finds that revenue losses outweighed asset losses for small businesses in disaster-affected areas (FEMA-designated disaster areas) in 2017. Among affected firms:

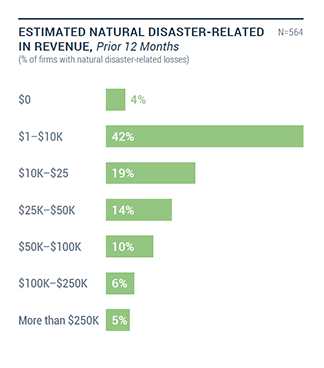

- 61 percent had revenue losses ranging from $1-$25,000, and 35 percent had revenue losses over $25,000.

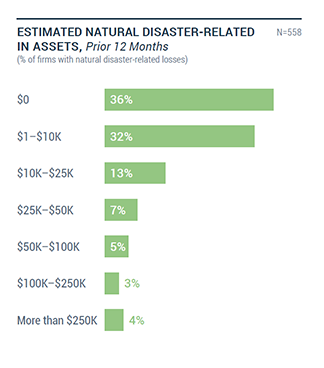

- 45 percent had asset losses ranging from $1-$25,000, and 19 percent had asset losses over $25,000.

Few small businesses had insurance to cover their losses from having to close during or after an event or to cover damage from the particular kind of disaster they experienced. Among affected firms:

- 65 percent cited loss of power or utilities as the source of their losses. Only 17 percent, however, had business disruption insurance at the time of the disaster.

- Flood damage (38 percent) and wind damage (36 percent) were also common sources of losses, but only 16 percent of affected firms had specific flood insurance coverage, and only 21 percent had wind insurance.

Small businesses that experienced losses in FEMA-designated disaster areas had a harder time getting access to capital than businesses with no losses, despite filling out more loan applications with large banks, community development financial institutions (CDFIs), and the Small Business Administration (SBA). Among affected firms:

- 66 percent that applied for financing experienced a funding gap, receiving less than the amount requested, compared to 55 percent of firms in affected areas without losses.

- 48 percent applied for credit, compared to 30 percent of unaffected firms.

There is a strong need for small-dollar loans and grants for small businesses in the immediate aftermath of a disaster. Among affected firms:

- 27 percent sought financing of $25,000 or less and 35 percent applied for financing of $25-$100,000.

What Can We Do?

The community development field can play a role in helping small businesses recover and become more resilient in the face of natural disasters. Lenders and the public sector can help make small dollar loans and grants available quickly after an event. This can make the difference between small businesses closing and getting back on their feet, which has ripple effects for wages and people staying in their homes after a disaster.

Including diverse stakeholders in planning ahead for the next natural disaster can help make disaster recovery more responsive to community needs. Organizations and agencies that already have relationships with small businesses can help them prepare for the next disruptive event. For example, helping small business owners assess their insurance needs and move their records online can minimize disruption to their operations when the next event occurs.

Spotlight on the 2017 California Wildfire Recovery

The report concludes with examples of cross-sector collaboration in the community development field from across the country. For instance, in the wake of the 2017 fires in California, the state partnered with the private sector to help facilitate small business lending. The California Infrastructure and Economic Development Bank (IBank) committed $10 million to the Disaster Relief Loan Guarantee Program. The fund, which operates on a rolling basis, helps small businesses secure loans in the immediate aftermath of an event, as well as over the long term when other sources of relief may have ended. The fund guarantees up to 95% of a qualified disaster relief loan, allowing small businesses to secure more favorable interest rates, and funding that might otherwise not be available, from private lenders on loans for repairs and economic losses. Local nonprofit financial development corporations in the state help connect small businesses with banks in their area.

For more detailed survey findings and examples of strategies for disaster resilience in the community development field, read the 2017 Small Business Credit Survey: Report on Disaster-Affected Firms. To learn more about the small business credit needs on the West Coast, check out the SF Fed’s 12th District Report.

The Small Business Credit Survey is a national survey conducted and analyzed by the Federal Reserve System. It collects information about business performance, financing needs and choices, and borrowing experiences of firms with 500 or fewer employees. It is not a random sample; therefore, results should be analyzed with awareness of potential methodological biases.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.