Korea has some of the most supportive policies for startups and small businesses, including an abundant supply of government-backed loans, due to their role as an employment engine. Support for small and medium-sized enterprises (SMEs) is poised to remain strong as the country undergoes a strategic shift toward inclusive and innovation-led growth. However, critics point to data suggesting government programs are enabling poor performance among companies. In response, policymakers have introduced a slate of measures to diversify financing, increase the role of capital markets, and improve productivity.

Davids and Goliaths

Korean SMEs are often over-shadowed by their larger counterparts—and for good reason. Korean chaebol—large conglomerates with household names like Samsung and Hyundai dominate the economy. The market cap of the top five chaebol represent more than 50 percent of the Korean stock market; by some estimates, the ten largest chaebol generate annual revenues equivalent to more than 40 percent of Korea’s GDP. But SMEs and start-ups are important engines of job creation, accounting for 82 percent of total employment according to data from the National Statistics office.1

In recent years, there has been a growing perception that South Korea would benefit from greater diversification and less reliance on large conglomerates. Most prominently, a series of scandals at chaebol (Samsung’s de facto leader was jailed for his participation in a national scandal that brought down the former president in 2017 and the chairman of Lotte was convicted in a bribery scandal in 2018; both sentences were suspended) have stoked the perception they are above the law. Lawmakers and economists have also criticized the conglomerates’ heavy industry- and export-oriented focus as ill-equipped to adapt to the emerging digital economy. A report in the Financial Times in August 2018 summed up criticism simply: “South Korea’s economic model is no longer competitive.”

Across Korea’s last three decades of economic expansion, growth has steadily slowed, from an average of 7-plus percent between 1990 and 2002, to 3.5 percent over the past 16 years. Much of this slowdown was anticipated as Korea’s economy matured. However, as chaebol have struggled to compete with Chinese counterparts, a chorus of voices have concentrated on policy initiatives that aim to increase innovation and prepare Korea for a fourth industrial revolution and the role that SMEs and startups should play. Recently proposed measures focus on increasing productivity and innovation by promoting alternative funding schemes and creating an ecosystem for funding startups through all phases.

Korean SMEs: The Good, the Bad, and the Ugly

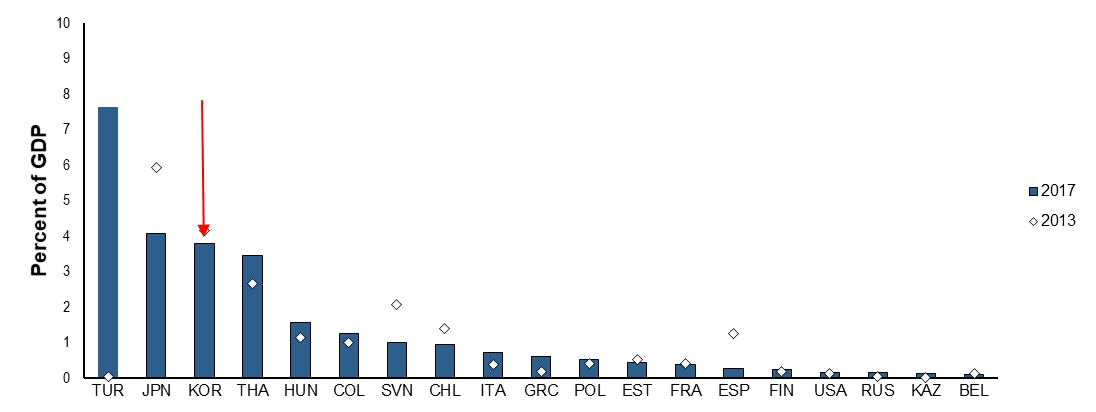

SMEs around the globe tend to suffer from a lack of adequate financing. In Asia, a severe mismatch exists between the economic impact of SMEs and their share of just 19% of banks loans. SMEs typically have less collateral, and are more costly to finance given their usually small loan size. Korean SMEs share some of these characteristics, but they benefit from more financing than foreign peers because of strong government support, by way of loans and guarantees, which account for more than 90 percent of SME financing.2 In 2017, the Korean government provided loan guarantees equal to 3.8 percent of GDP, second only to Turkey and Japan among OECD countries (Figure 1). According to the Korea Development Institute, as of 2014, three large public finance institutions specializing in SME financing had loans and guarantees totaling more than 80 trillion won (about US$ 67 billion). In addition, Korea’s government subsidizes utilities for SMEs and prioritizes SMEs for government procurement as part of a program that represents 3 percent of annual government expenditures.

Government Loan Guarantees as a Percentage of GDP

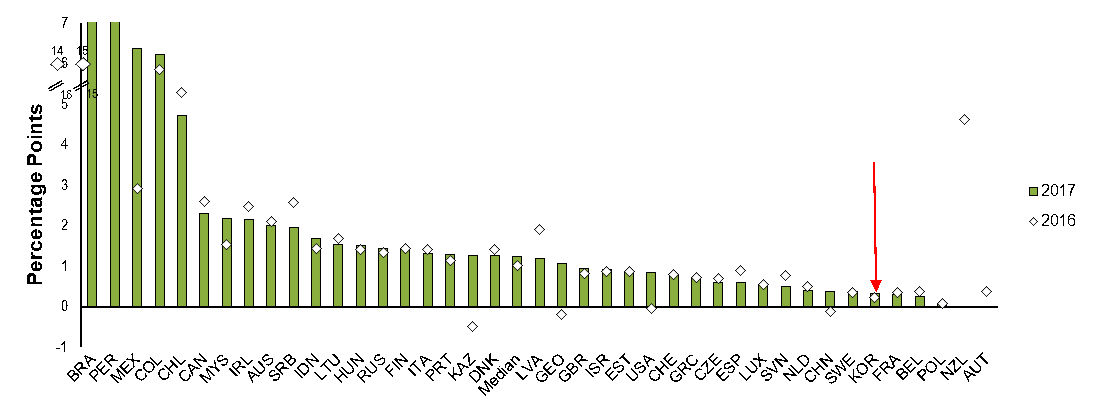

Moreover, Korean SMEs’ access to funding has improved over time. According to the OECD, the interest rate differential between loans to large Korean firms and SMEs is one of the narrowest among OCED economies (Figure 2). According to another study, the funding gap for SMEs — described as the shortage in funding for SMEs due to market failures — is a relatively low at 5 percent of all SME loans.3

Interest Rate Difference Between SMEs and Large Enterprises

Globally, SMEs are not as productive as large firms, and Korea is no exception. Despite favorable financing, Korean SMEs in manufacturing are, according to one OECD study, a third as productive as their conglomerate counterparts. The fact that SMEs are less productive than larger ones is not surprising given limitations of economies of scale, spending on research and development, and sector focus, among other (often universal) reasons. However, somewhat surprisingly, research indicates that Korean SMEs accessing government support are on average less productive than SMEs that did not receive public financing.

While it is not uncommon for national governments to promote SMEs’ important economic role, Korea’s combination of SME efficiency challenges and potential distortions caused by public finance stands out as a policy case study. In historical instances, an abundance of financing has led to failures, such as promoting inefficient or “zombie” companies and/or curtailing private financial institutions’ underwriting data and methodology. One 2016 Korea Development Institute study noted public funding leads “to market distortion and undermines the market’s efficiency-enhancing mechanism,” with an emphasis on “survivability” rather than productivity.

Coming Policy Changes

In keeping with its dedication to SMEs and start-ups, the Korean government has announced intentions for a range of new measures to diversify SME financing. While these plans are broad and involve encouraging more bank lending by way of easing collateral requirements, a host of other schemes—such as creating a viable ecosystem for venture capital investment in startups; and improving the KONEX, a stock exchange for smaller companies—focuses on improving capital market funding.

As part of the push, the Financial Services Commission (FSC), Korea’s financial policymaker and regulator, has taken initiatives to improve venture capital financing for start-ups. The FSC has established the Innovation Venture Capital Fund with the aim of raising 3.7 trillion won (roughly US$ 3.1 billion) in 2019 and a total of 10 trillion won by 2020, 60 percent of which will come from private investors. The fund will support innovation as well as startups in different stages of development.4 Policy makers hope venture capital financing can apply market discipline to SMEs and start-ups. Moreover, according to reporting by the Financial Times, fund managers, not bureaucrats, will take the lead in assessing promising start-ups unlike earlier funds. Ensuring that funding is allocated to early-stage companies seems key to this scheme, as these firms are historically least likely to get funding.

The FSC also announced plans to breathe new life into the KONEX, founded in 2013 to serve SMEs too small for the KOSDAQ—the Korean version of the NASDAQ. The measures permit crowdfunding and expand so-called “small offerings,” which reduce regulatory burdens of an IPO. In addition, the government plans to relax initial capital requirements with the goal of fostering a pool of professional investors and brokerage companies specializing in SMEs.

More Work Ahead

As Korea continues to settle into a period of lower growth, Korean SMEs and startups will be expected to pull their weight in improving productivity. Public financing is abundant, to the point of enabling inefficiencies. In response, the government is promoting alternative market-based funding that may encourage the most competitive and productive SMEs, and evolve government policy beyond loans and guarantees.

Going further will require creativity, forcing the government to cut red tape and tackle entrenched norms, including cultural stigma regarding entrepreneurial failure and workers’ preference for employment at large institutions (government and chaebol). Diversifying funding sources and focusing more attention on productivity will be good steps to achieving the government’s stated desire of promoting a future of inclusive growth and innovation.

1. Other estimates put this figure at as high as 90 percent.

2. Jones, R. and M. Kim (2014), “Promoting the Financing of SMEs and Start-ups in Korea”, OECD Economics Department Working Papers, No. 1162, OECD Publishing, Paris. http://dx.doi.org/10.1787/5jxx054bdlvh-en, p. 8.

3. Lee, J. and H. Lim (2017), “Does Credit Rationing Really Exist in Korea? Evidence from the SME Loan Market”, Korea Journal of Financial Studies, Vol. 46, No. 3, Korean Securities Association, Seoul.

4. The Innovation Venture Capital Fund consists of a Growth Support Fund of 8 trillion won, and Innovation Startup Fund of 2 trillion won.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.