Across the world, women face a variety of hurdles to reaching their full economic potential. Challenges associated with educational and financial access, structural economic factors, and culture can all pose impediments to women’s economic participation. In prior posts, the Pacific Exchange blog has explored trends in the nature of women’s professional activities in Asia, ranging from a discussion of women’s labor force participation in the world’s most populous economies—China and India—to female participation in entrepreneurship across the region. Against that backdrop, this blog turns to the question of finance: Do women have access to the financial services as well as the decision-making roles that enable them to prosper in economic terms?

At the moment, we know that women’s access to and inclusion in the financial system in Asia faces a persistent gender gap, as it does in other parts of the world. Data suggests that women are disproportionately under-represented, and despite recent improvements, parity in access remains far off. This issue warrants more attention, as bringing more women into the financial system historically leads to financially stronger families, communities, and business sectors—which together catalyze and sustain a stronger overall economy.

Women Are a Large Majority of Asia’s Unbanked

The World Bank estimates that more than 1 billion people in Asia are “unbanked”—defined as no access to formal financial services. According to the 2017 Global Findex Database, Asia’s most populous countries account for the vast majority of the unbanked, with an estimated 225 million people in China and 190 million people in India lacking a bank account. On a global scale, the unbanked are highly concentrated in Asia: China, India, Indonesia, and Bangladesh contain roughly one third of the global total. Measured as a share of the total population, the lack of financial inclusion is particularly acute in a few Asian economies: in the Philippines and Vietnam, less than one in three adults have access to financial services; in Cambodia, less than one in five holds an account.

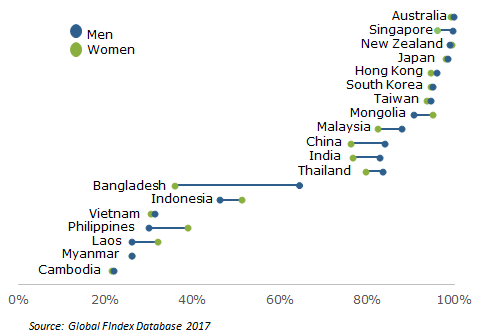

Across the globe, women are overrepresented among the unbanked, accounting for 56 percent of all adults without a financial account. This trend is starker in Asia: women represent 60 percent of unbanked adults in China and India, despite relatively high levels of financial access in both countries (approximately 20 percent of both countries’ populations remain unbanked). The imbalance in access as measured by gender is equally prevalent in places with lower levels of financial development, including Bangladesh, where half of the population is unbanked, 65 percent of which are women. Account ownership statistics portray the issue in clear terms (Figure 1). The gap in access between gender groups is largest in Bangladesh (where the share of banked women trails the share of banked men by an astonishing 29 percentage points), China (8 percentage points), and India (6 percentage points).

Despite these gaps, there has been some recent improvement. India’s Jan Dhan Yojana scheme, a government policy launched in 2014 to increase financial inclusion through biometric identification, helped raise account ownership among adults up from 35 percent in 2011 to 80 percent in 2017. The most significant improvement occurred in rates of female account ownership, which jumped from 26 percent to 77 percent, and helped close the gender gap by more than 10 percentage points.1

Account Ownership by Gender

Elsewhere, the picture is a bit more balanced, particularly outside of South Asia. In Asia’s developed economies, for example, the vast majority of women hold accounts, and the gender gap is either negligible or reversed. Interestingly, the gender gap is also small in the region’s least developed economies. In Cambodia, Vietnam, and Myanmar (where at least two-thirds of the population remains unbanked), account ownership rates are identical among men and women. In Indonesia, Laos, and the Philippines, women are in fact more likely than men to own an account.

In several places, greater female financial inclusion is a relatively recent phenomenon resulting from positive gains over the past few years. In Indonesia, account ownership among the adult population more than doubled between 2011 and 2017, while female account ownership climbed from under 20 percent to over 50 percent. In line with broad gains in financial inclusion in Malaysia, where now 85 percent of the population receives financial services versus 66 percent in 2011, women have benefitted from Bank Negara Malaysia’s pioneering work on financial inclusion as well as microfinance programs, including the Women Entrepreneur Financing Program, targeted at female financial inclusion.

The Benefits of Female Financial Inclusion

Financial inclusion is a broadly held goal of expanding access to financial services across the population and a pathway to reducing poverty and improving economic outcomes. Access to financial services enables individuals to accumulate savings, increase financial resilience, and raise productive capacity. At a macro level, these services contribute to faster economic growth and lower inequality and poverty.

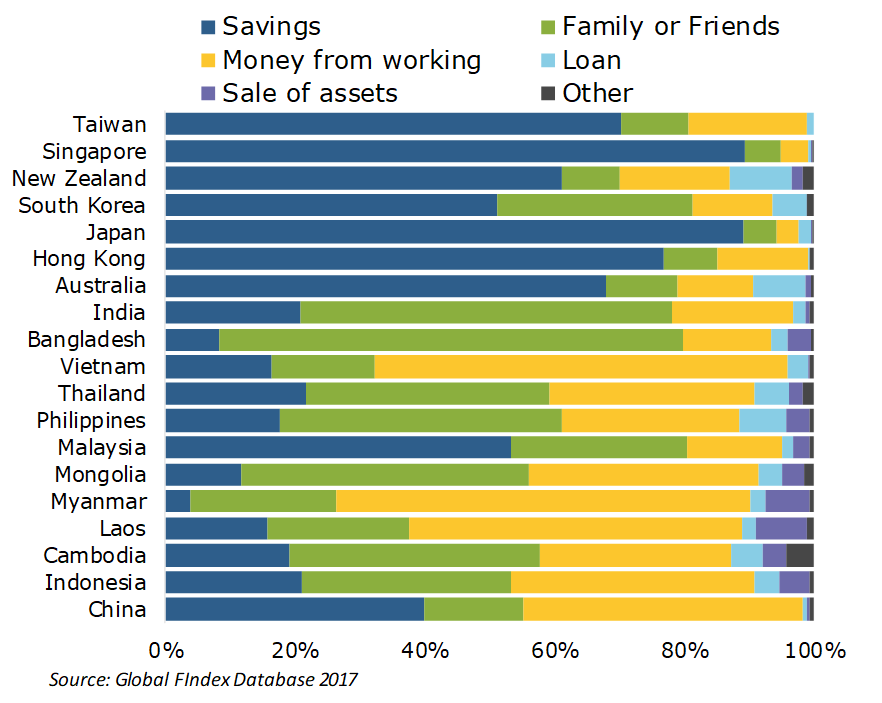

Access to financial services is particularly critical for women’s financial resilience and stability. The Global Findex Report found that women in developing economies are 11 percentage points less likely than men to say it is possible to come up with emergency funds (equal to 1/20 of gross national income) within one month’s time. In addition, women outside of the financial system are also more likely to be excluded from the labor force: while 68 percent of unbanked men globally are either employed or seeking work, only 41 percent of women are engaged in the labor force. Particularly in East Asia, women rely predominantly on earned income (43 percent) and savings (34 percent) to weather unexpected financial needs (Figure 2). Limiting access to savings, credit, and insurance products therefore serves to jeopardize women’s ability to navigate unforeseen developments, let alone nurture and expand entrepreneurial opportunities. Encouragingly, research has documented that once women gain access to baseline services (such as deposit accounts), they are more likely to gain access to other credit services.

Main Source of Emergency Funds (% Able to Raise, Women Age 15+)

Financial inclusion among women also has well-documented spillover benefits for the whole community—above and beyond the gains from raising financial inclusion more broadly. Indeed, the World Bank has documented country case studies where women used bank accounts to save a larger share of income, invest more in their businesses, and spend more on items that benefit the entire households. Additional research reinforces the finding that financially empowered women are more likely to improve their family’s welfare.

Financial inclusion can be thought of in broader terms than simple access to services; research suggests there is also a strong business case for higher female representation in leadership positions. The IMF reports that a higher proportion of women on bank and banking supervision boards is positively linked with bank stability through higher capital buffers and more robust profitability. Credit Suisse’s latest Gender 3000 report finds evidence that companies with a higher proportion of women in decision-making roles is correlated with higher returns on equity, as well as more conservative balance sheets. Among businesses where women account for a majority of top management, data show higher sales growth, high cash flow returns on investment, and lower leverage. Notwithstanding the current gap in access, Asia holds some other promising trends relating to female financial empowerment. According to Credit Suisse, Asia boasted the highest level of female CEOs at 4.6 percent. Gender diversity in the boardroom is climbing, with female representation jumping 60 percent between 2014 and 2016—albeit from a low base, as the total share of women remains below 10 percent.

The Future of Finance is Female

In summary, improving access to accounts and services helps women build resiliency—not only for themselves but also for their households and communities. Greater representation of women at the highest levels of the industry can usher in greater intellectual diversity that contributes to improved economic outcomes overall. Policies akin to those in India and Malaysia—raising financial inclusion broadly with the use of technology, and targeting funding toward women-led initiatives—can serve as a current model for the region. In the private sector, business leaders are likely to benefit from making more concerted efforts to mentor and promote women into more decision-making roles. Policymakers and business leaders in Asia and beyond would do well to think of female populations as arguably the most promising source of future financial growth.

1. Account ownership does not mean account use, however. Nearly half of India’s accounts are inactive—the highest in the world. The program brought an additional 310 million people into the formal banking system between August 2014 and March 2018, and the low utilization rate may reflect the fact that many have not yet had an opportunity to use their account.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.