Mark M. Spiegel, senior policy adviser at the Federal Reserve Bank of San Francisco, shared views on the current economy and the outlook from the Economic Research Department as of February 26, 2026.

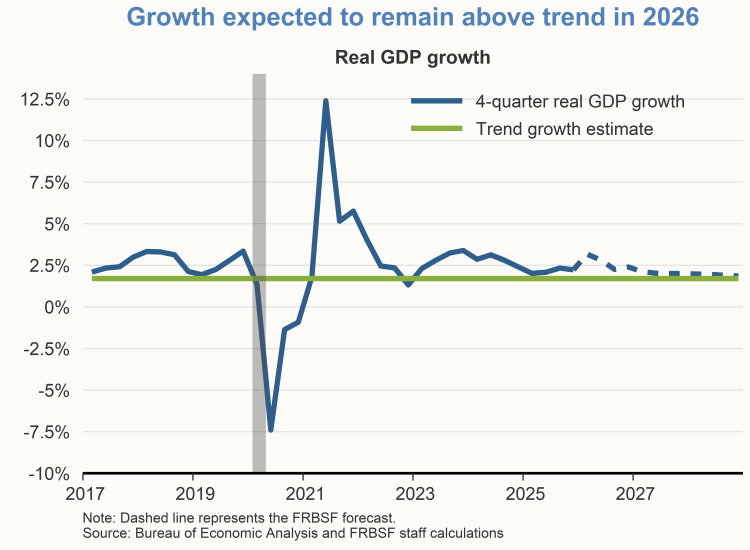

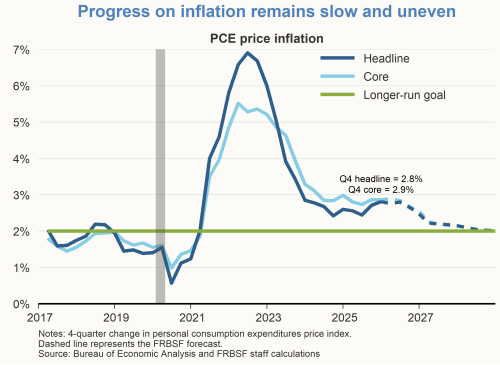

Despite the fourth quarter slowdown in growth, which was driven in part by the federal government shutdown, the U.S. economy continues to advance at a robust pace, and output growth is expected to remain solid in the first half of the year. The labor market appears to be stabilizing after cooling over most of 2025, although risks appear tilted to the downside. There has been little progress on inflation over the past year. The 12-month change in the headline personal consumption expenditures (PCE) price index for December 2025 was 2.9%, above its December 2024 value. The 12-month core PCE inflation rate, which excludes the volatile food and energy categories, was 3.0%, unchanged from its year-ago value. Inflation readings for 2025 were likely influenced by the imposition of new tariffs. The effects of existing tariffs should wane going forward as producers complete the process of passing tariffs through to goods prices, fully or partly. Real GDP growth slowed in the fourth quarter of 2025 to 1.4% on an annualized basis, far below the third quarter, 4.4% pace. We expect growth to rebound during the first half of 2026. The prospects for knowledge-intensive industries and activities related to artificial intelligence (AI) are a source of uncertainty around the 2026 outlook. They appear to have played an outsized role in driving real GDP growth in 2025.

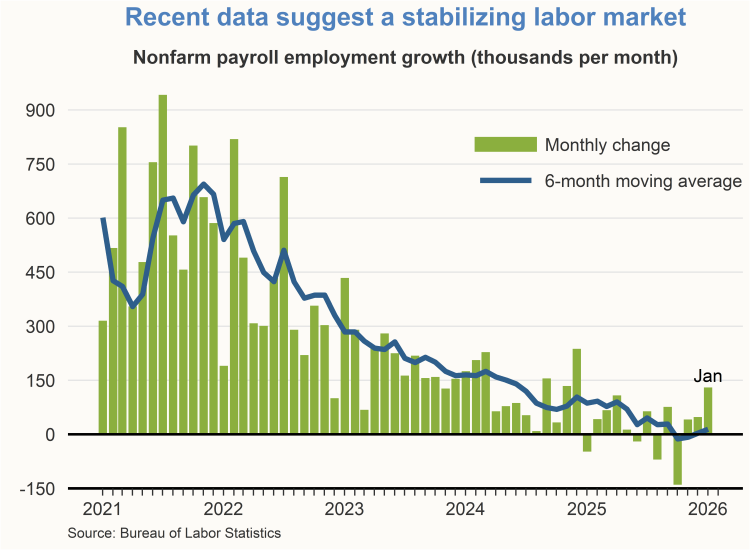

Strong January employment report stabilizes labor outlook

Despite a robust January employment report which showed an increase in nonfarm payroll employment of 130,000 new jobs, prior jobs data show that that the labor market has cooled. Private-sector employment gains in January were particularly strong, adding 172,000 jobs. Federal government employment fell by 34,000 jobs, influenced by continued separations associated with deferred resignation programs that were initiated last year.

The Bureau of Labor Statistics’ annual benchmark revisions, which were first announced last summer and implemented in the January report, reduced estimates of monthly 2025 job gains by about 35,000 per month, leaving current estimates for average monthly job gains for the year at 15,000. The revisions highlighted ongoing compositional changes in the U.S. labor force, as health-care employment continued to grow rapidly, while manufacturing employment declined.

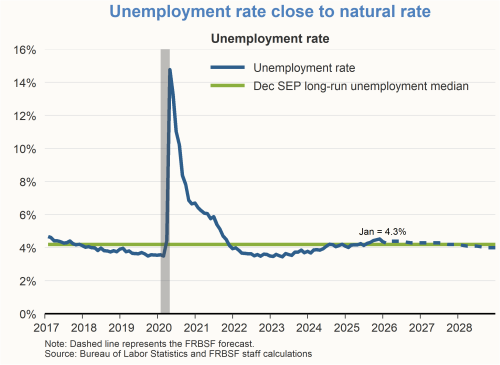

The unemployment rate in January ticked down to 4.3% from 4.4% in December and now hovers just above the median longer-run projection of 4.2% from the FOMC’s December 2025 Summary of Economic Projections (SEP). The downward movement in the unemployment rate was partly driven by a large drop in unemployment for teenage and young adult workers. Given that unemployment rates for these categories tend to be volatile, more data is needed to confirm the trend in the overall unemployment rate. At the same time, indications that risks to the labor market are tilted to the downside continued to emerge. For example, the January report issued by the firm Automated Data Processing (ADP) showed only 22,000 new private-sector jobs created, well below the consensus forecast of 44,000.

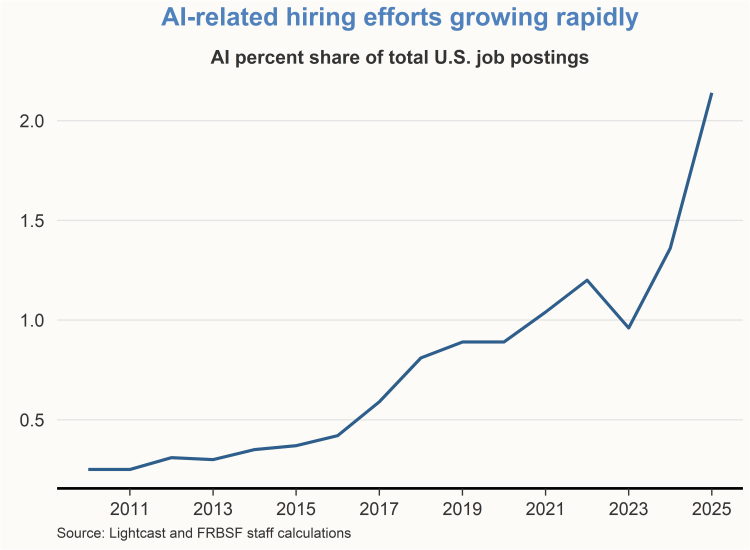

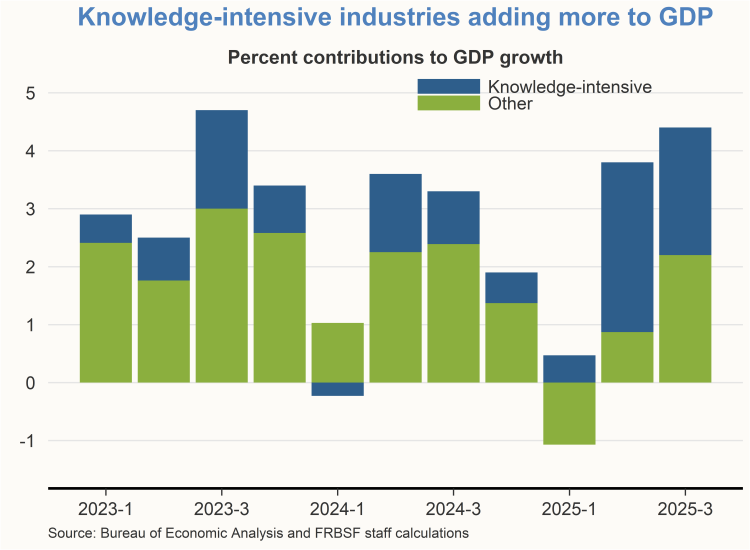

AI and information-related activity grew rapidly in 2025

AI and information-related job postings accelerated rapidly in 2025. Job-posting data from the tracking firm Lightcast show the share of postings for information-related jobs, including those associated with AI. Textual analysis is used to identify this category of job postings following the methodology of Acemoglu, et al. (2002). The share of such job postings has accelerated rapidly since the pandemic, and this pattern ramped up during 2025.

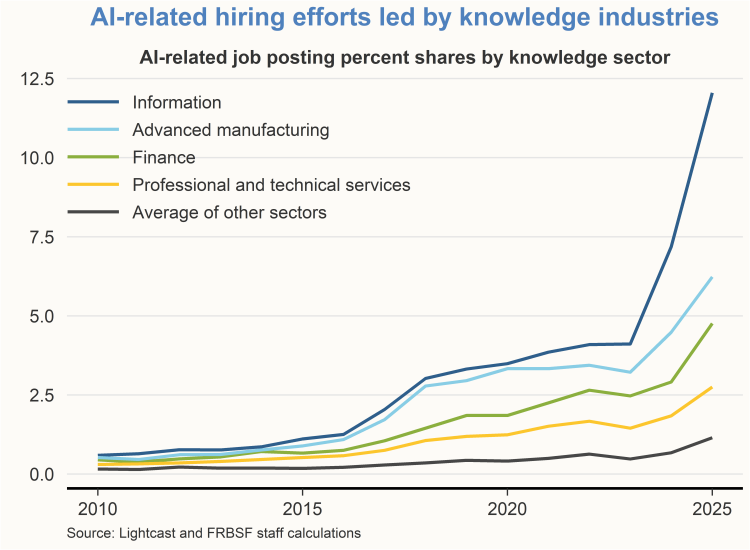

AI and knowledge-related job postings were unevenly distributed across industries in 2025. Such postings are concentrated in the areas of information, advanced manufacturing, finance, and professional and technical services. These sectors comprised a little over a quarter (26.3%) of U.S output in the third quarter of 2025, reported in the most recent sectoral release by the Bureau of Economic Analysis. On average, the share of AI postings in 2025 was 6.5% for the four knowledge-intensive industries. This is far above the average of other sectors in the economy, which is 1.2%.

The rapid growth in AI-related job postings suggests an increased implementation of AI in the production and distribution of goods and services throughout the economy. Indeed, the same knowledge-intensive industries that show a surge in AI-related job postings also show outsized contributions to real GDP growth in the second and third quarters of 2025, the most recent quarters with industry-level growth readings. While these sectors in total only represent just over a quarter of total output, they accounted for 50% of output growth in the third quarter. Developments in these knowledge-intensive industries are likely to be influential in the near-term growth outlook as well.

We expect solid, above-trend growth during the first half of 2026 as the economy rebounds from the sluggish growth induced by the federal government shutdown in 2025.

Slow, uneven progress on inflation continues

Inflation, as measured by the 12-month change in the headline PCE price index, remains elevated relative to the FOMC’s 2% longer-run goal. Quarterly headline inflation relative to a year earlier was 2.8%. The quarterly annual change in the core PCE price index, which excludes the volatile food and energy categories, was 2.9% for the year ending in 2025 Q4. Goods price inflation during 2025 was pushed up by the imposition of new tariffs. These effects should wane going forward, as producers complete the process of passing tariffs through to goods prices.

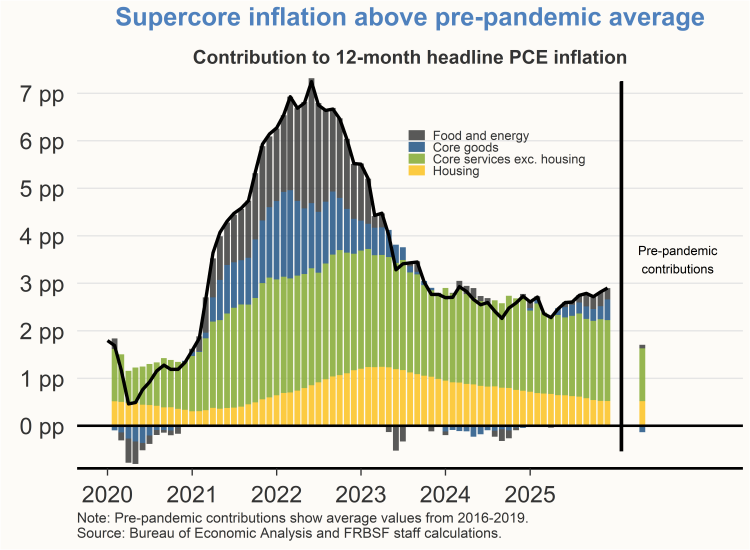

Among the inflation components, inflation in core services excluding housing, also called “supercore” inflation, remains stubbornly elevated relative to pre-pandemic levels. Housing inflation has eased over 2025. We expect inflation to slow gradually over 2026 but still end the year above 2%. The implications for inflation of the recent Supreme Court ruling on tariff authorization remain unclear at this time.

There are both upside and downside risks to inflation depending on the degree of further pass-through from tariffs to goods prices and the possible imposition of replacement tariffs in response to the Supreme Court ruling.

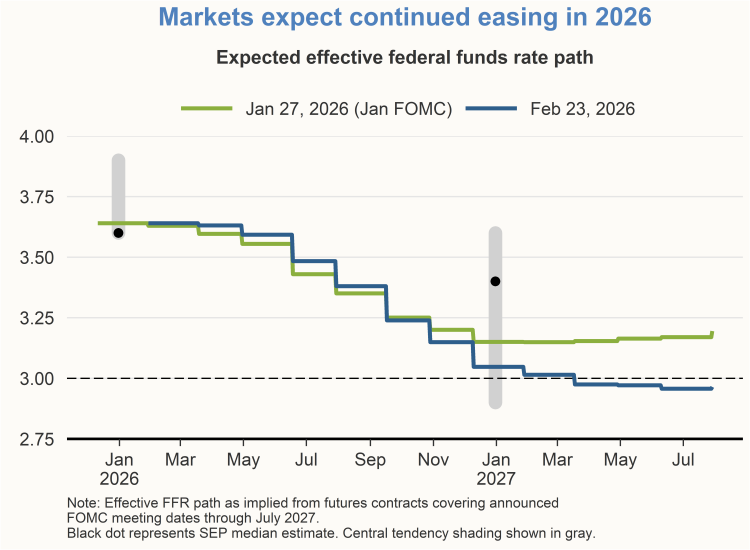

Monetary policy expected to ease further in 2026

At the conclusion of the January FOMC meeting, the Committee announced its decision to maintain the target range for the federal funds rate at 3.5% to 3.75%. This decision followed monetary policy moves in the three previous FOMC meetings that lowered the funds rate by 75 basis points. During the post-meeting press conference, Chair Powell noted that the policy stance was now within a range of plausible estimates of neutral, and that the FOMC was “well positioned to determine the extent and timing of additional adjustments to our policy rate based on the incoming data, the evolving outlook, and the balance of risks.”

The current range of the federal funds rate remains above the median longer-run projection of 3.0% from the FOMC’s January Summary of Economic Projections (SEP). This longer-run projection can be viewed as an estimate of the neutral policy rate, one which is neither restrictive or accommodative. Given the modestly restrictive stance of current policy, market participants expect further easing in 2026 towards neutral.

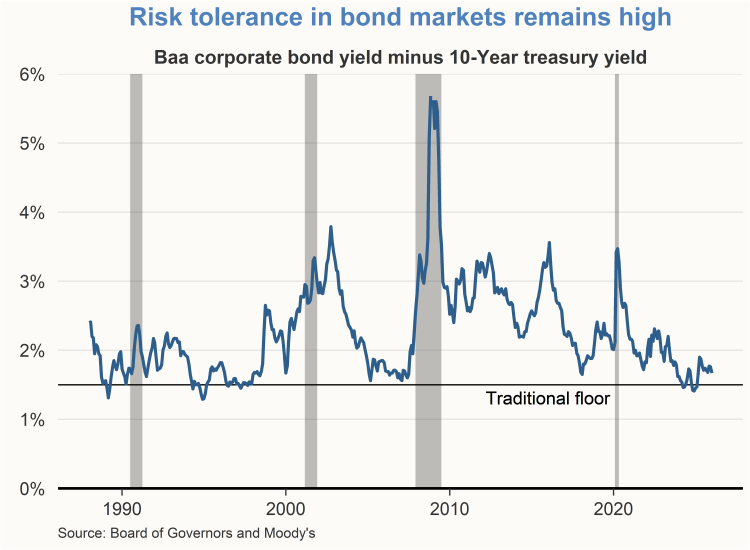

Financial conditions have tightened a bit this year. Nevertheless, overall levels of risk tolerance appear elevated by historical standards. For example, spreads between Baa corporate bond yields and yields on 10-year U.S. Treasury bonds remain below 2%. In recent history, yield spreads this low were often followed by increases in market volatility, including the major disruptions associated with the 1997 Asian Financial Crisis and the 2008 Global Financial Crisis. Hence, the current degree of elevated risk tolerance is a sign of potential market vulnerability going forward.

Charts were produced by Naomi Halbersleben.

The views expressed are those of the author with input from the Federal Reserve Bank of San Francisco forecasting staff. They are not intended to represent the views of others within the Bank or the Federal Reserve System. This publication is edited by Kevin J. Lansing, Karen Barnes, and Hamza Abdelrahman. SF FedViews appears eight times a year. Please send editorial comments to Research Library.