Thomas M. Mertens, senior vice president and associate director of research at the Federal Reserve Bank of San Francisco, shared views on the current economy and the outlook from the Economic Research Department as of July 16, 2026.

The U.S. economy continues to expand at a solid pace. Despite a softer-than-expected employment report in June, the labor market has seen robust job gains over the past few months and appears broadly in balance. Meanwhile, elevated energy prices have pushed inflation further from the Fed’s 2% goal but appear to have had little impact on overall economic activity. A partial normalization of oil prices over recent weeks lowered retail gas prices and provided some relief to consumers’ budgets, though geopolitical developments led to another price increase amid renewed volatility. Looking ahead, risks to inflation remain mainly on the upside. In contrast, the outlook for the real economy is two-sided: Overall uncertainty could weigh on consumer spending, while investment in artificial intelligence could further raise productivity and economic growth.

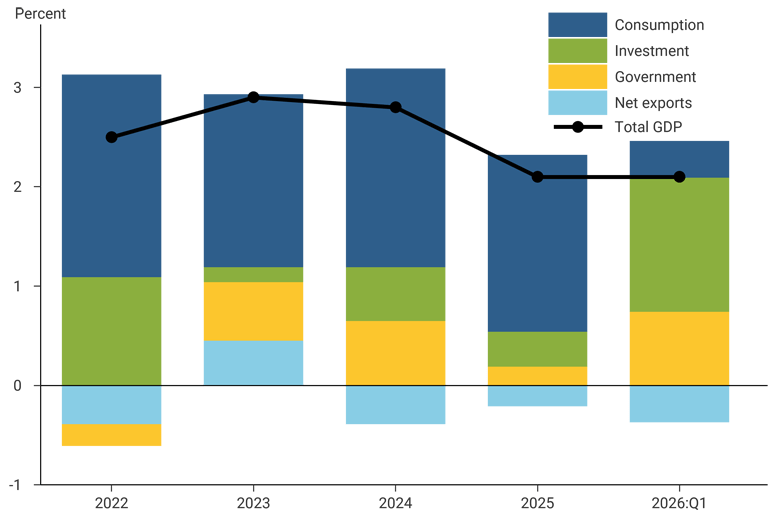

Strong business investment driving solid economic growth

The U.S. economy expanded at an annualized rate of 2.1% in the first quarter of 2026. The solid quarterly growth was driven primarily by strong business investment in technology equipment and software. At the same time, consumer spending rose only slightly, growing at its slowest quarterly pace since 2022.

Solid economic growth driven by strong investment

Real GDP growth, contributions by category

Incoming second-quarter data suggest strong activity in industrial production and moderate growth in consumer spending. Economic expansion for 2026 overall is expected to be similar to last year’s pace, when the economy grew at a rate of 2.0%. Risks around this forecast run above their historical norms.

Labor market remains stable, while inflation above goal

Headline personal consumption expenditures (PCE) inflation, the Federal Reserve’s preferred measure of inflation, rose notably in recent months from an already elevated level following disruptions in energy markets. The most recent PCE data in May show inflation at 4.1%, well above the Fed’s 2% goal. Expected normalization in energy markets and global supply chains later this year is projected to bring inflation back to a downward trajectory that will return it to goal by 2028. However, a high degree of uncertainty clouds this forecast.

Inflation above goal; labor market stable

12-month headline PCE inflation and unemployment rate

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, and FRBSF staff.

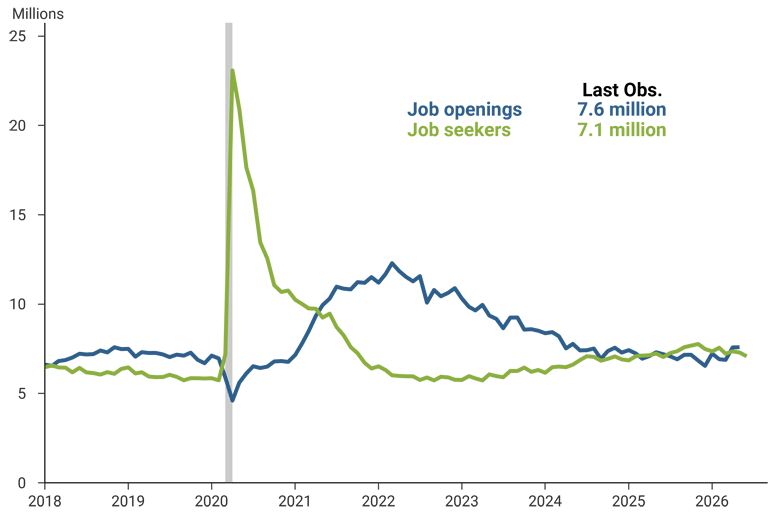

The view that the labor market is broadly balanced is supported by a comparison between the number of job seekers and job openings, which serve as proxies for labor supply and demand. The most recent data for the number of job openings across the U.S. economy stood at 7.6 million, only slightly exceeding the number of people actively looking for work.

Number of job openings and job seekers in balance

Job openings and number of people actively looking for work

Source: Bureau of Labor Statistics via FRED.

Over the recent past, these two measures have tracked each other closely. Nevertheless, the risk of a more pronounced slowing in the labor market with a sharper rise in unemployment remains.

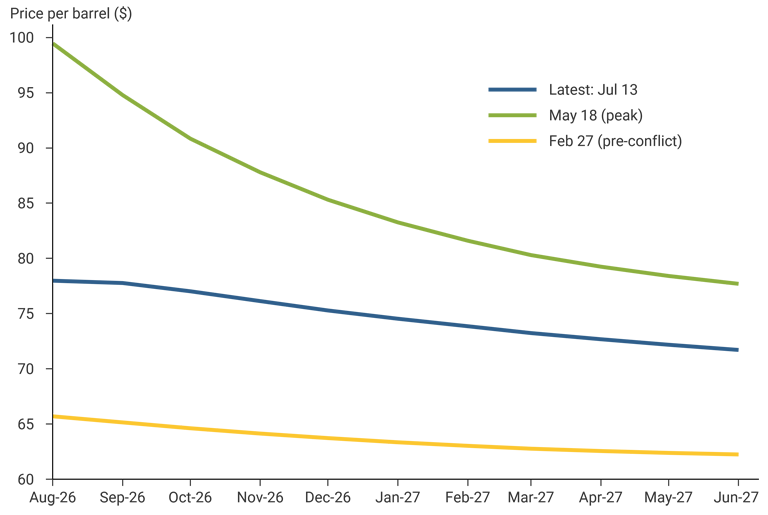

Volatile energy prices

Energy prices have been highly volatile since the outbreak of the conflict in the Middle East. Oil futures prices rose sharply between March and mid-May, particularly at shorter horizons, which led to a downward-sloping curve.

Already elevated oil prices have risen recently

West Texas Intermediate oil futures curve

Source: Bloomberg.

Starting in early June, oil futures prices trimmed most of those gains, and their decline spilled over to lower gas prices at the pump. However, recent events raised oil futures prices again and added renewed volatility.

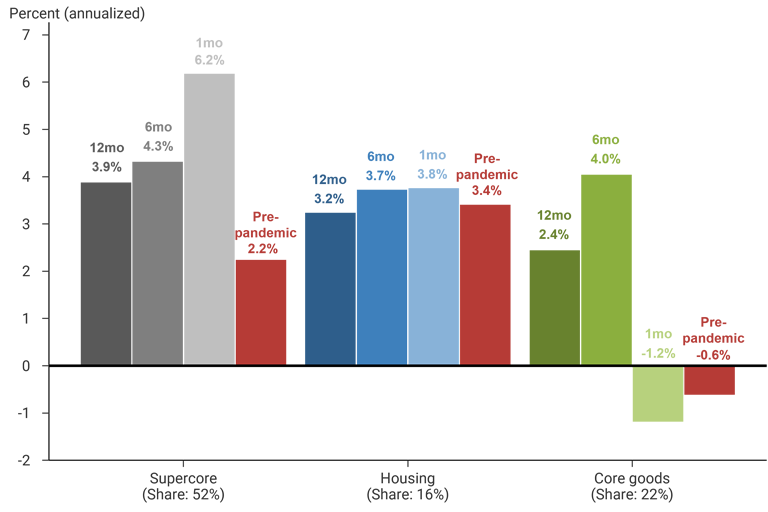

Upward momentum in core PCE inflation categories

But not all inflation stems from energy prices. Core PCE inflation, which strips out the volatile food and energy categories from the headline figure, has also been elevated. According to the latest data from May of this year, core PCE prices rose at an annualized rate of 3.9% in May and by 3.4% year-over-year.

Upward momentum in core PCE inflation categories

Core PCE inflation trends, by spending category

Source: Bureau of Economic Analysis and FRBSF staff calculations.

The 12-month changes in all three major components of core inflation—nonhousing core services, also known as supercore, housing services, and core goods—have been elevated relative to the 2% inflation goal. The price increase over the past six months in each category exceeded the price change in the prior six-month period. Supercore and core goods inflation have also been running higher than their pre-pandemic 2016-2019 averages over the past year. Core inflation has thereby generally been on the rise recently.

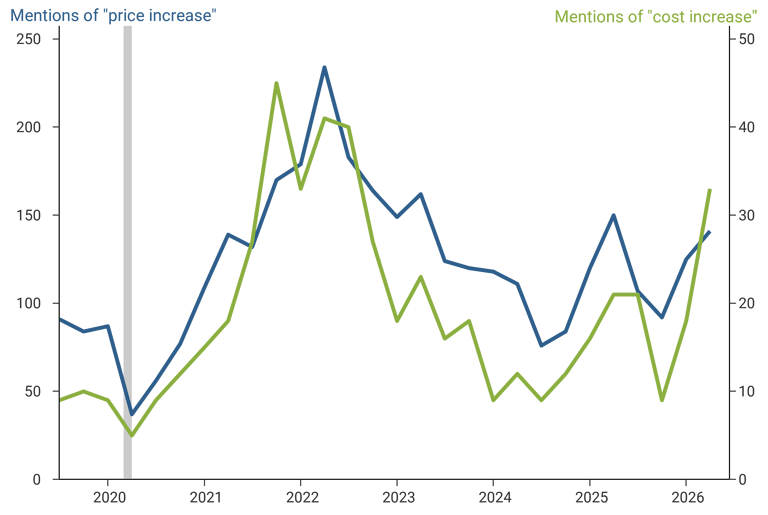

In line with these trends, businesses seem to be putting greater emphasis on inflation. The number of times price and cost increases and related words are mentioned in earnings calls by companies in the S&P 500 stock market index has increased substantially: The reading from the second quarter of 2026 far exceeds levels observed in recent years.

Businesses cite price and cost increases

Mentions in earnings call transcripts of companies in S&P 500

Source: Bloomberg and FRBSF staff calculations.

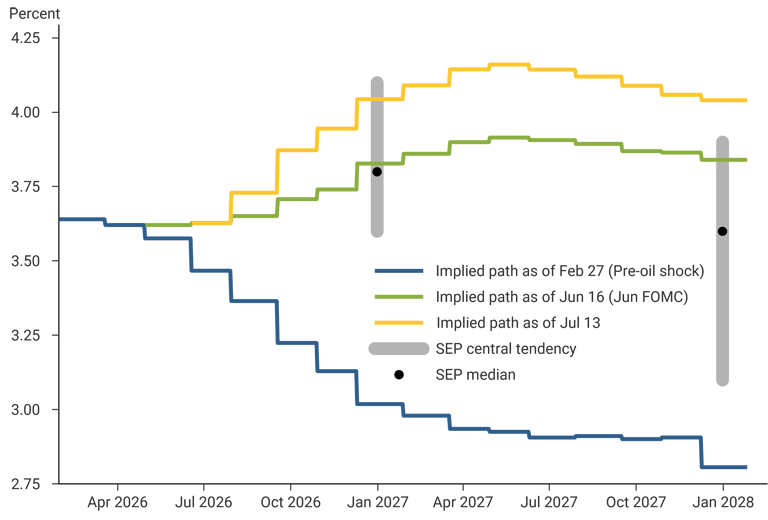

Markets expect interest rate hike in the second half of 2026

In their latest meeting, the Federal Open Market Committee (FOMC) kept the target range for the federal funds rate unchanged at 3.50–3.75%, where it has stayed since December 2025. Market expectations for future interest rates have shifted considerably over the course of this year.

Markets expect rate hike later this year

Markets-implied federal funds rate path

Source: Bloomberg and FRBSF staff calculations.

Financial market participants had priced in two rate cuts by the end of this year before the onset of the Middle East conflict. This expectation reflected in part the softer labor market conditions that prevailed late last year and early this year. Following the onset of the Middle East conflict and associated disruptions in energy markets and supply chains, markets now instead expect a rate hike, and potentially a second, by late 2026. This expectation is somewhat above the median of the FOMC’s Summary of Economic Projections from the June meeting.

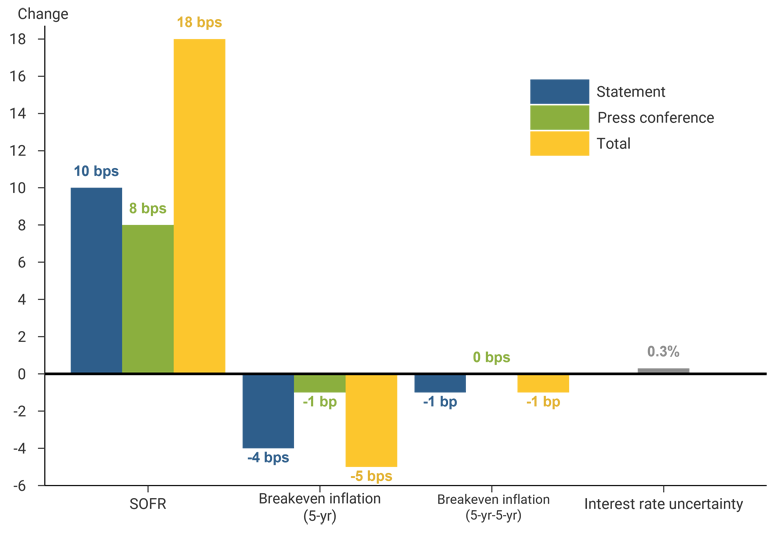

Recent FOMC communication surprised markets

Communication by the FOMC following its most recent meeting led to a repricing in several markets. SOFR futures, which are closely tied to expectations about the policy rate, rose substantially both around the release of the FOMC statement and during Fed Chairman Kevin Warsh’s press conference. Shorter-term breakeven inflation expectations declined during that time, while long-term inflation expectations were largely unchanged.

Recent FOMC communication perceived as hawkish

June FOMC announcement effects on market pricing

Source: Bloomberg, SF Fed Center for Monetary Research, and staff calculations.

This market reaction constitutes one of the largest repricings following scheduled monetary policy announcements in decades. At the same time, the market-implied uncertainty around policy rates 10 years in the future did not change materially.

Charts were produced by Wesley Wasserburger.

The views expressed are those of the author with input from the Federal Reserve Bank of San Francisco forecasting staff. They are not intended to represent the views of others within the Bank or the Federal Reserve System. This publication is edited by Kevin J. Lansing, Karen Barnes, and Hamza Abdelrahman. SF FedViews appears eight times a year. Please send editorial comments to Research Library.