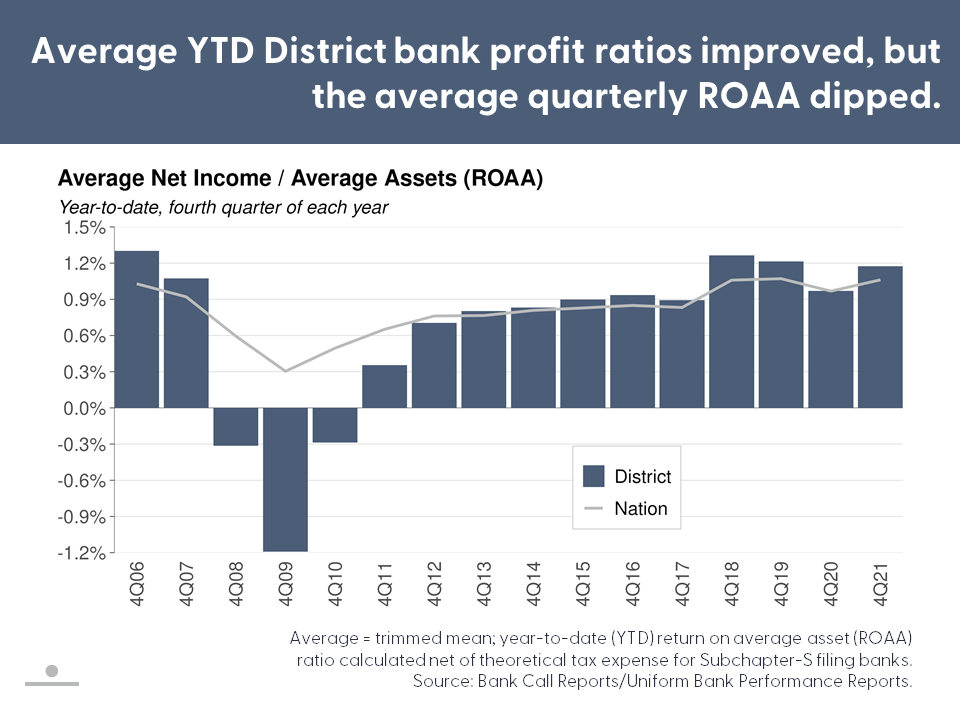

First Glance 12L provides a quarterly look at banking and economic conditions within the Federal Reserve System’s Twelfth District. During 4Q21, District bank loan growth accelerated — led by new commercial real estate (CRE) mortgages — more than offsetting declines in Paycheck Protection Program (PPP) balances. Although positive, net new lending continued to trail deposit growth. Consequently, on-balance sheet liquidity edged higher. Full-year ROAAs outpaced 2020 amid an improved credit outlook and the dilutive effect of asset growth on overhead ratios. Average 4Q21 profits benefited from PPP fees and low provision expense burdens, but not to the same degree as 3Q21. Meanwhile, noninterest expense ratios ticked up. Loan delinquencies and losses remained low but fading stimulus and developing geopolitical tensions may pose headwinds.

Unemployment rates declined in all District states in the fourth quarter and hiring continued steadily, with a notable jump in the transportation/utilities sector. Housing markets tightened further as sales remained strong and supply was limited, although Districtwide home-price growth cooled a bit. Housing affordability declined sharply, and housing insecurity remained elevated in some states as foreclosure protections expired. CRE transaction volumes recovered, and prices increased, but CRE fundamentals underperformed in some District markets—particularly in the San Francisco Bay Area. Looking ahead, geopolitical tensions may dent consumer confidence and business investment.