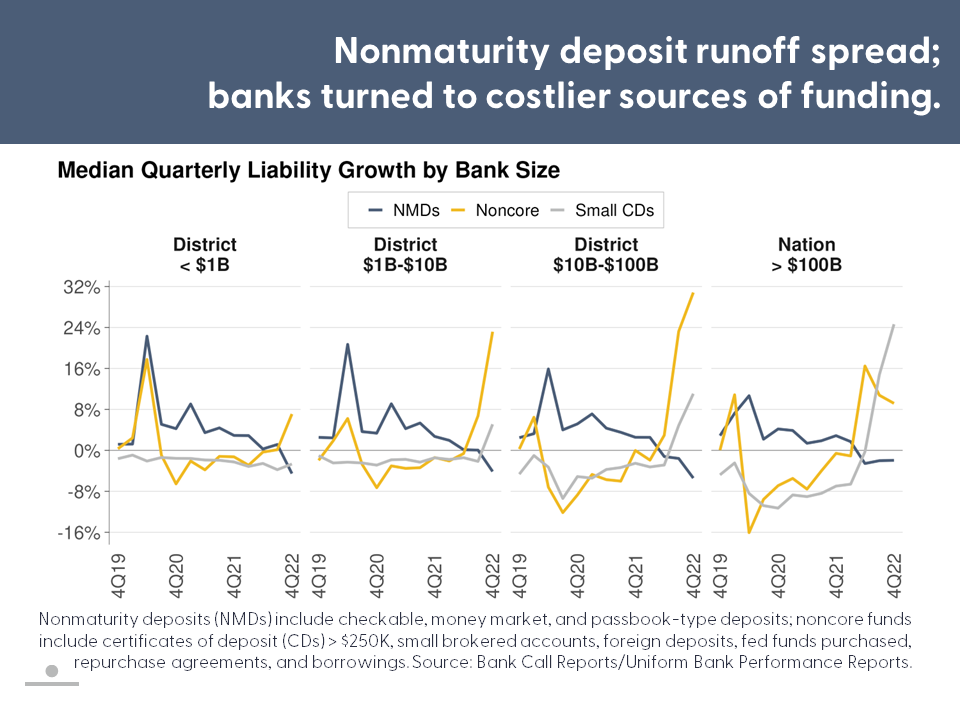

First Glance 12L provides a quarterly look at banking and economic conditions within the Federal Reserve System’s Twelfth District. Quarterly earnings improved among the District’s banks but liquidity tightened. Increases in asset yields outpaced higher interest expenses, overhead costs, and provisions for credit losses. However, funding cost ratios moved notably higher as nonmaturity deposit runoff became more widespread, deposit competition intensified, and banks shifted balance sheet funding towards pricier sources. Banks used liquid instruments to fund loan growth and/or deposit withdrawals, contributing to tighter on-balance sheet liquidity. Net unrealized losses among bond portfolios moderated but continued to constrain liquidity options and crimp “book” capital. Problem loan levels remained low. Still, surveys showed a growing share of bankers tightened standards and expected loan performance to weaken.

District job and real estate markets cooled further. In aggregate, the pace of District job growth slowed, and unemployment rates edged higher. Home price indices mostly declined, approaching or dipping below year-ago levels in Idaho, Washington, and California’s San Francisco Bay/Sacramento areas. In the West, December’s existing home sales reached the slowest pace since 1993 and one-to-four family permit activity continued to contract. Across several commercial real estate sectors, transaction volumes and/or price indices declined amid rising debt service and operating costs, slowing rent growth, and growing economic uncertainty.