Download PDF (pdf, 182 kb)

Download Chart Data (Excel document, 82 kb)

Introduction

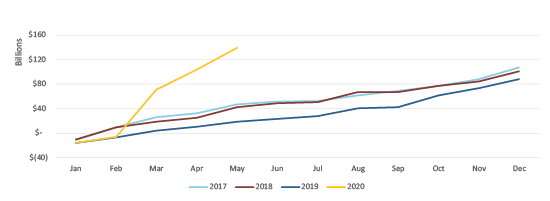

In October 2019, the Federal Reserve conducted the sixth Diary of Consumer Payment Choice (Diary)1. Approximately two months later, the first case of COVID-19 was identified in China, and the virus has since spread to create a global pandemic. As the number of COVID-19 cases increased worldwide, U.S. cities and states began issuing stay-at-home orders in March 2020, and global demand for U.S. currency increased at record rates. Since March 1, the Federal Reserve has issued approximately $130 billion of currency into circulation (Figure 1). Because the 2019 Diary was conducted before the spread of COVID-19, it does not reflect payment behavior changes caused by the pandemic. Given the dramatic increase in demand for currency, along with anecdotal evidence of changing consumer payment practices during the pandemic2, the Cash Product Office (CPO) sought to capture data regarding how the pandemic may have affected individuals’ payment behavior.

Figure 1

Yearly Cumulative Growth of Currency in Circulation (CIC)

To better understand potential payment behavior changes, the Federal Reserve sent a supplemental survey to Diary participants in May 2020. Of the 3,016 individuals who participated in the 2019 Diary, 2,737 completed the supplemental survey. While the Diary requires participants to record their daily transactions, the supplemental survey required only recollection of past behavior. As such, the 2019 Diary is more comprehensive and contains the most up-to-date Diary data, while information from the supplemental survey gives us insight into how payment behavior is evolving in the midst of the crisis.

The CPO asked 10 COVID-19 survey questions3, which participants answered between April 15 and May 12, 2020. The questions focused on three general themes: cash holdings, changes in payment behavior, and cash avoidance. In general, participants reported holding more cash on their persons and especially as a store of value in their homes, compared to trends reported in the 2019 Diary. The questions focusing on changing payment behavior show approximately 20 percent of participants have switched to paying online or over the phone, with most of the switching taking place at restaurants, fast food locations, and big-box stores. Individuals were asked whether they were avoiding cash and 70 percent indicated they were not. Additionally, participants were asked whether they had conducted any in-person payments, and nearly two-thirds reported they had made no in-person payments since March 10. While this is not necessarily a deliberate avoidance of cash usage, it implies people are not spending their extra cash holdings.

Section 1. People are holding more cash

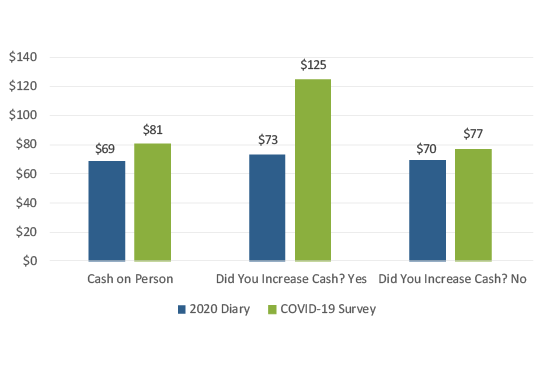

Survey participants were asked whether they increased their cash holdings as a result of the pandemic and to report the total dollar value of cash generally carried in their pocket, wallet, or purse. On average, the amount of cash people carry increased from $69 to $81, a 17 percent increase from the pre-pandemic amount reported in the 2019 Diary (Figure 2). Holdings increased by 71 percent to $125 for individuals who withdrew extra cash and by 10 percent to $77 for those who did not withdraw extra cash.

Figure 2

Cash Held in Pocket, Purse, or Wallet

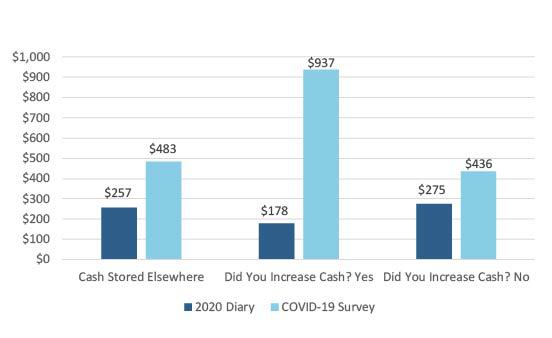

In addition to reporting cash held on their person, participants were asked to report the value of cash stored elsewhere (e.g. home or office). The value of cash stored elsewhere was far greater for all respondent groups compared to pre-pandemic amounts. On average, cash stored elsewhere nearly doubled, rising from $257 to $483 (Figure 3). Those who withdrew extra cash increased their holdings by 426 percent, jumping from $178 to $937, and those who did not withdraw extra cash increased their holdings by 58 percent, rising from $275 to $436.

Figure 3

Cash Stored Elsewhere

The degree to which individuals who withdrew extra cash increased their storage may point to the relief cash can offer in times of uncertainty and to its role as a contingency payment method. Rising values of cash holdings have been observed in the Diary of Consumer Payment Choice for the past few years. Whether the COVID-19 pandemic serves to accelerate this trend is yet to be seen.

Section 2. Many people did not make in-person payments

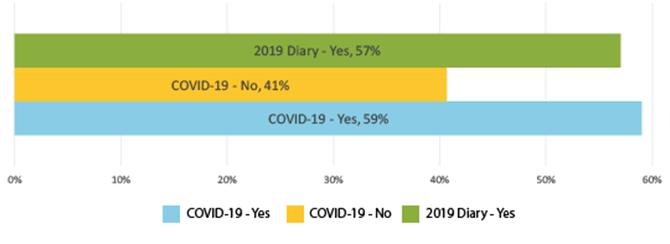

The majority of survey respondents reported not making any in-person payments since March 10, 2020 (Figure 4). Of the individuals who reported making in-person payments, 59 percent used cash at least once, a similar rate to the 57 percent of individuals who used cash at least once in the 2019 Diary (Figure 5). The similar rate at which cash is being used in person suggests that stories on the erosion of payment preferences during the pandemic may be overstated.

Figure 4

Did you make any in-person payments since March 10, 2020?

Figure 5

Did you use cash to make an in-person payment?

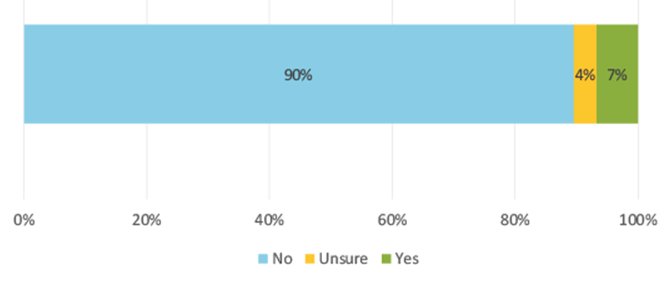

Individuals who made in-person transactions reported having little difficulty paying with cash. On average, 90 percent of in-person payees claimed cash was accepted at the merchant they visited (Figure 6).

Figure 6

Did the Merchant Refuse Cash?

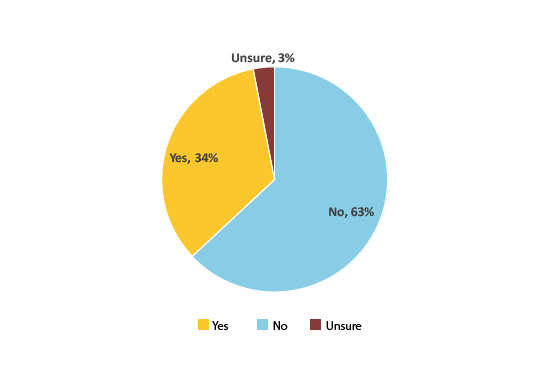

Section 3. Most people are not avoiding cash

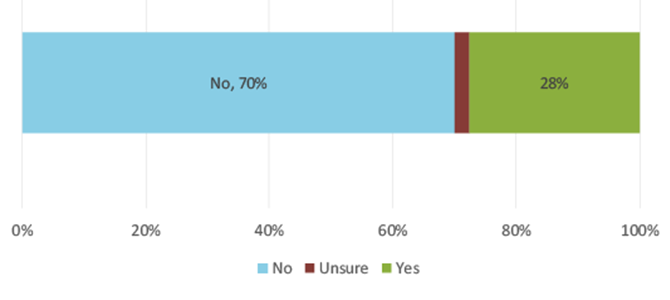

The majority of survey respondents claim they are not avoiding using cash (Figure 7). Although 28 percent stated they are avoiding using cash, they continue to hold more of it during the pandemic.

Figure 7

Are you avoiding using cash?

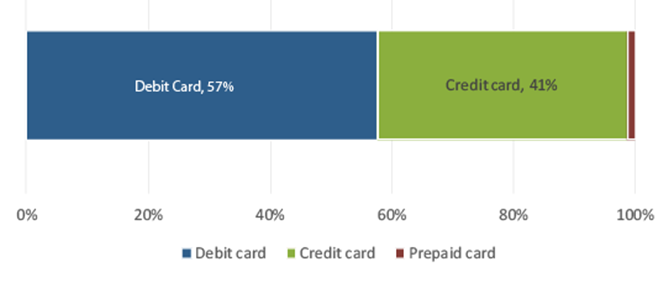

When asked what payment method they switched to when avoiding cash, respondents listed debit or credit cards 98 percent of the time (Figure 8).

Figure 8

What payment method did you use when avoiding cash?

Section 4. Online payment behavior does not appear substantially different

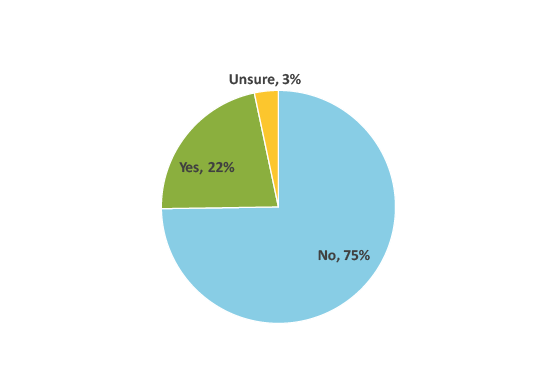

When asked if they had switched to paying online or by phone instead of paying in person, 75 percent of respondents claimed to have made no switch (Figure 9). This does not mean individuals made no online purchases, but that their previous online shopping habits did not change. A possible reason why participants may not have increased their online purchases may be that they are making less purchases overall due to financial stress.

Figure 9

Did you switch from in-person to online or phone payments?

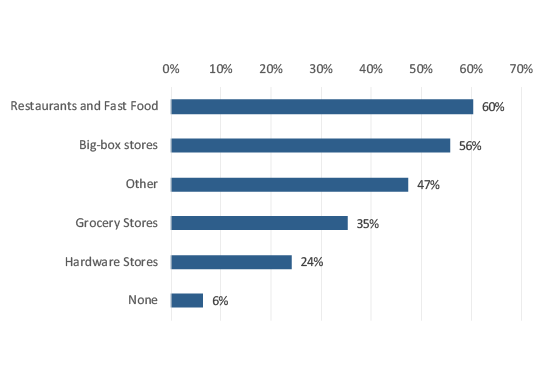

The individuals who claimed to switch to online and phone purchases did so primarily for restaurants, fast-food, and big-box stores, although other merchants also saw relatively high switching rates (Figure 10).

Figure 10

For which merchant type did you switch?

Conclusion

The 2019 Diary of Consumer Payment Choice was the last consumer payments study conducted by the Federal Reserve before the world was exposed to COVID-19. It is unknowable whether consumers’ payment behaviors will change permanently as a result of the pandemic. Our current information demonstrates that transactional use of cash has decreased and its role as a store of value has increased, while domestic and international demand continues to substantially increase. However, future studies are needed to determine the full extent and duration of any observed and undetected changes. Supplemental survey findings give us some insight into how people are responding, but Diary data collected in October 2020 will provide more detail on the magnitude of change resulting from the pandemic. Future Diary studies beyond 2020 will further resolve whether any observed changes are temporary or enduring.

Reference

Kim, Laura, Raynil Kumar, and Shaun O’Brien. July 2020. “Findings from the 2020 Diary of Consumer Payment Choice.” Federal Reserve Bank of San Francisco.

Footnotes

1. Refer to the “2020 Findings from the Diary of Consumer Payment Choice” paper for details on the survey conducted in October 2019.

3. The 10 questions were part of a larger questionnaire administered to the Understanding America Panel by the University of Southern California Dornsife Center for Economic and Social Research.