Jackelyn Hwang

As housing has become increasingly unaffordable in the Bay Area, anecdotal accounts abound of people living in crowded conditions, with individuals and families doubling up and sharing spaces. Overcrowded housing has various negative health implications1 and is of particular relevance in the context of COVID-19, as early evidence suggests greater spread within households where people are in sustained contact for extended periods of time.2

As we work on a forthcoming report on gentrification and housing instability in the Bay Area, we sought to explore the issue of overcrowding given its current salience in the COVID-19 pandemic. Data from the Federal Reserve Bank Consumer Credit Panel / Equifax Data allows us to see how many adults live in the same household and how this number changes after a person moves residences within the Bay Area.3 Using these data, we examined the extent to which people who moved within the Bay Area over the past decade and a half ended up with more adults in their household (approximating more crowded conditions4) and how moving to more crowded conditions varied based on socioeconomic status (SES), whether people move from gentrifying areas, and over time. Though we could not assess the race/ethnicity of movers with these data, it is important to note that people of color are generally more likely to experience overcrowded housing compared to white people.5

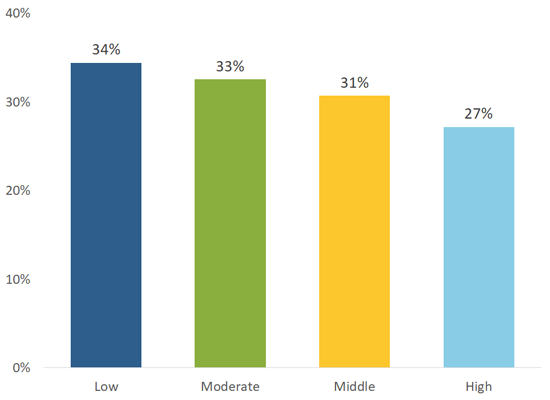

Overall, we found that from 2002-2017, 30% of people who moved within the Bay Area ended up in households with more crowded conditions (from 1-2 adults to 4 or more adults). Moves to more crowded conditions were most likely among low-SES residents (34%) (Figure 1), and the likelihood of moving to more crowded conditions declined as SES increased. (Note that our measure of SES is based on Equifax Risk Scores, a type of credit score, so SES in our analysis approximates financial stability rather than income or wealth.)

People Who Are Least Well-Off Are Most Likely to Move to More Crowded Conditions

Movers within the Bay Area whose household size increases from 1-2 adults to 4+ adults, by socioeconomic status, 2002-2017

Source: Federal Reserve Bank of New York Consumer Credit Panel / Equifax Data

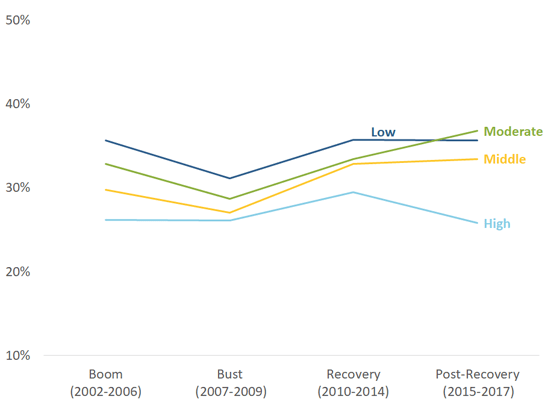

When we looked across four different time periods (defined based on Bay Area market trends), we found that moves to more crowded conditions were generally consistent over time for low-SES movers except when housing costs were declining during the housing bust (Figure 2). For moderate- and middle-SES residents, there was an upward trend in moving to more crowded conditions since the bust, with levels for the most recent period exceeding boom levels and notably higher for moderate-SES residents than low-SES residents. In contrast, the share of high-SES movers in 1-2 person households moving to more crowded conditions declined during the most recent period.

Moves to More Crowded Conditions Have Been Increasing since the Housing Bust for Everyone except Those Who are Most Well-Off

Movers within the Bay Area whose household size increases from 1-2 adults to 4+ adults, by socioeconomic status, over four housing periods

Housing Periods: Boom=2002-2006, Bust=2007-2009, Recovery=2010-2014, Post-Recovery=2015-2017

Source: Federal Reserve Bank of New York Consumer Credit Panel / Equifax Data

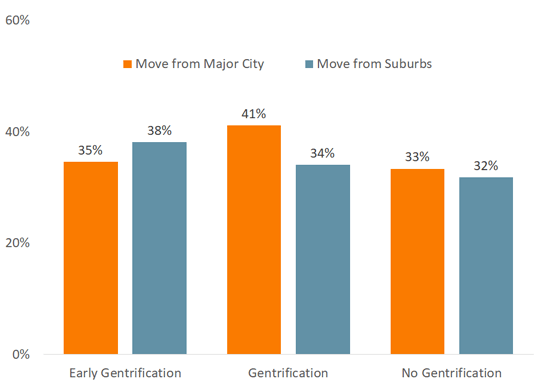

To understand how dynamics of gentrification and displacement affected overcrowding, we also examined patterns of low-SES people in 1-2 person households who moved from areas experiencing early gentrification, gentrification, and those not experiencing gentrification6 and assessed whether there were differences for those moving from major cities (San Francisco, San Jose, or Oakland) compared to those moving from suburban areas.

We found that moves to more crowded conditions were highest among movers from gentrifying neighborhoods in cities (41%), but also more common in suburban neighborhoods showing early signs of gentrification (38%) during the post-recovery period (Figure 3). This finding suggests that while gentrification is traditionally seen as an issue primarily putting pressure on residents in urban areas, it is also affecting suburban areas of the Bay Area.

Among the Least Well-Off Residents, Those Moving from Gentrifying Areas in Major Cities and Early-Gentrifying Areas of Suburbs are Most Likely to Move to More Crowded Conditions

People with low-socioeconomic status moving within the Bay Area whose household size increases from 1-2 adults to 4+ adults by level of gentrification, 2015-2017

Figure 3.

Moving from area experiencing early gentrification

- 35% move from major city

- 38% move from suburbs

Moving from area experiencing gentrification

- 41% move from major city

- 34% move from suburbs

Moving from area experiencing no gentrification

- 33% move from major city

- 32% move from suburbs

Source: Federal Reserve Bank of New York Consumer Credit Panel / Equifax Data

The implications of the housing affordability crisis cut across many dimensions of well-being and raise new concerns given the current crisis of COVID-19. For households that may be more likely to rely on face-to-face contact and others who have greater exposure or susceptibility to COVID-19, our findings have implications not only for their own health, but that of their household, and ultimately for the health of communities on the whole. The COVID-19 crisis has increased a sense of urgency around our collective health, recognizing that our well-being as a region depends on creating the conditions for each of us to be healthy. As measures recently taken to limit the spread of COVID-19 are creating additional pressures during the current housing crisis, we must continue to identify strategies to increase availability of safe and affordable housing.

Stay tuned for our full report on Gentrification and Housing Instability in the Bay Area, forthcoming.

Acknowledgment: The authors thank Brooke Ada Tran for her research assistance.

1. World Health Organization, “Crowded Housing” in WHO Housing and health guidelines. Geneva: World Health Organization; 2018.

2. Jack Lee, “Coronavirus: Who gave you COVID-19? It’s not who you think. Here’s what we know about how it spreads,” The Mercury News, May 14, 2020; Qifang Bi et al., “Epidemiology and transmission of COVID-19 in 391 cases and 1286 of their close contacts in Shenzhen, China: a retrospective cohort study,” The Lancet Infectious Diseases, April 27, 2020; Wi li, et al., “The characteristics of household transmission of COVID-19,” Clinical Infectious Diseases, April 17, 2020.

3. The Federal Reserve Bank of New York Consumer Credit Panel is a nationally representative 5% anonymized random sample of adult consumers with Social Security numbers (SSNs) and a credit history, collected quarterly by the credit bureau Equifax. These data include the number of adult consumers (which includes anyone with a public record or closed or authorized accounts) who live in the same household, where residents live and move, and credit information including Equifax Risk Scores (a type of credit score). We analyze residents aged 25 to 84 years old who move beginning on June 1st of one year and ending on June 1st of the following year within the nine-county Bay Area from 2002 to 2017. There are approximately 240,000 adult residents in the Bay Area in our sample in each year. We approximate socioeconomic status using Equifax Risk Scores, defined as follows: low-SES < 580 or no Equifax Risk Score (too few accounts or new credit to estimate a score), moderate-SES: 580-649, middle-SES: 650-749, and high-SES: 750 or higher. Because our data lack individual demographic information on race and ethnicity, we were unable to examine moves by race/ethnicity in our analyses.

4. We define a move to more crowded conditions as an increase in adult household members from 1-2 per household to 4 or greater. While the typical threshold for household crowding is when the number of occupants exceeds the capacity of the dwelling space available, we are unable to assess dwelling size or presence of children.

5. Based on authors’ calculations using data from US Census Bureau, American Housing Survey, 2017.

6. Our analysis groups gentrifiable neighborhoods (median household income in 2000 subregion’s 50th percentile (median) of % increases in either median rent or home values and (2) % increase in college-educated population or median household incomes subregion’s 50th percentile (median) of % increases in either college-educated residents or median household incomes, Early Gentrification = (1) % increase in median rent or home value > subregion’s 25th percentile of % increases in either median rent or home values or (2) % increase in college-educated population or median household incomes > subregion’s 25th percentile of % increases in either college-educated residents or median household incomes, Nongentrifying: Gentrifiable and does not meet any of the criteria for gentrifying or early gentrification. Subregions account for the variation in housing affordability dynamics across the Bay Area. We define them in the following way: East Bay = Alameda and Contra Costa Counties, North Bay = Marin, Napa, Solano, and Sonoma Counties, San Francisco = San Francisco County, South Bay = San Mateo and Santa Clara Counties.