Many credit line agreements contain restrictive covenants and other contingencies that may limit the ability of borrowers to draw on their lines, which is a particular concern to small firms. This Economic Letter reviews recent empirical studies that suggest that private firms’ access to credit lines is much more sensitive to changes in bank lending standards than is access by publicly traded firms.

During the current credit crisis, borrowing under lines of credit has been an important source of corporate liquidity, according to company regulatory filings. For example, Ford Motor Company notified its lenders in January that it intended to borrow the total unused amount under its secured revolving credit facility “due to concerns about the instability in the capital markets, (and) with the uncertain state of the global economy,” according to its 10-K annual report filed with the Securities and Exchange Commission in March. Early in February, lenders advanced Ford $10.1 billion.

Concerns about capital market conditions have prompted even some investment-grade borrowers to draw on credit lines. For example, Computer Sciences Corporation, rated A- by Standard & Poor’s, reported in its February 2009 10-Q quarterly filing that it “recently responded to the dislocation in the commercial paper market by drawing down $1.5 billion under its committed revolving credit facility.”

This drawdown of credit lines may help explain the apparent paradox that bank commercial and industrial (C&I) lending increased last fall at the same time that borrowers and bankers were reporting extremely tight credit market conditions. C&I loans held by U.S. domestic banks increased from $1.514 trillion in August 2008 to $1.582 trillion by year-end, while the Federal Reserve’s Senior Loan Officer Opinion Survey on Bank Lending Practices found that a record net 83.2% of respondents reported that their institutions had tightened loan standards for large and medium borrowers in the fourth quarter.

This Economic Letter reviews recent empirical evidence on the use of credit lines as a source of corporate liquidity and the relationship between credit line usage and credit market conditions. The Letter addresses three questions:

- How do credit lines serve as liquidity sources for corporate borrowers?

- What conditions do banks place on using credit lines and how do those conditions affect access to credit?

- How do the use and availability of credit lines vary with credit market conditions?

Lines of credit as sources of liquidity

A line of credit is a commitment in which a borrower receives a promise from a bank or other financial institution to provide a loan over a set period at predetermined terms. As of February 2009, according to the Federal Reserve Survey of Terms of Business Lending, 77.6% of all C&I loans were made under such loan commitments, roughly the same as the percentage immediately before the credit crisis began.

The interest rate on most credit lines is based on a fixed markup over a benchmark, such as the prime rate or the London interbank offered rate (Libor), according to Loan Pricing Corporation’s DealScan database. As a result, although the cost of credit-line borrowing varies with changes in the benchmark, the fixed markup protects the borrower from rate increases caused by widening of marketwide credit spreads, as well as changes caused by declines in the borrower’s credit quality. Because credit-line loans are available on relatively more attractive terms when marketwide risk spreads increase and other types of credit become less available and more expensive, borrowers would typically be expected to draw down their lines during such periods.

Credit-line commitments protect borrowers against decreased credit availability, as well as borrower-specific and marketwide changes in credit risk premiums, but the insurance is not complete. One obvious contingency is that the lender may not be able to advance funds when the borrower needs liquidity. For example, Ford reported that it was unable to access its entire credit line due to the bankruptcy of Lehman Brothers, one of the members of Ford’s lending syndicate. Thus, concerns about the financial health of lenders may prompt borrowers to draw on their lines.

Conditions banks place on lines of credit

Other potentially limiting contingencies have to do with the financial health of the borrower. For example, most credit lines have material adverse condition clauses. Although rarely invoked, such clauses permit lenders to withhold funds if a borrower’s credit quality deteriorates significantly. A far more important potential limitation is the requirement that borrowers comply with cash flow, coverage, liquidity, and other covenants specified in the credit agreement (see Demiroglu and James 2009). Cash flow covenants restrict borrowing if cash flow, or EBITDA (earnings before interest, taxes, depreciation, and amortization), drops below a preset minimum, or the ratio of debt to cash flow exceeds a preset maximum. Coverage covenants require that a borrower’s coverage ratio (typically the ratio of EBITDA to fixed charges or interest expenses) remain above a minimum. Liquidity covenants require borrowers to maintain liquidity, typically defined as cash and cash equivalents plus the unused portion of the credit line, above a particular level. From January 2007 to March 2009, 84% of credit lines of publicly traded companies and 88% of lines of privately held companies contained at least one of these covenants, according to DealScan.

Credit-line availability will also vary depending on how tightly covenant threshold levels are set. For example, if a borrower’s maximum debt-to-EBITDA is set at 4.5 and the ratio is already 4.25 when the commitment takes effect, then even a small EBITDA decline may violate the covenant threshold.

Overall, such loan covenants in effect make credit availability contingent on borrower operating performance. If a firm’s performance deteriorates, as it may during an economic slowdown, credit availability will be reduced. Lenders typically react to violations of financial covenants (so-called technical defaults) by reducing or limiting additional borrowing under the line. Thus, for lenders, credit lines provide a contingent form of insurance against liquidity shocks.

Evidence on operating performance and use of credit lines

Two recent studies examine the relationship between credit-line availability and firm operating performance. Using information from 10-K annual reports, Sufi (2009) examines the relationship between line usage and operating performance for 300 publicly traded firms from 1996 through 2003. He finds that the better a company’s performance, the more likely it is have a credit line. More significantly, Sufi finds that the importance of credit lines as sources of corporate liquidity varies with the borrower’s operating performance. Sufi examines two basic sources of liquidity: cash and unused borrowing capacity under lines of credit. He finds that the relative importance of bank credit lines as liquidity sources increases with a firm’s operating cash flow. Sufi argues that one reason for this relationship is that firms with a higher cash flow are more likely to remain in compliance with credit line cash flow covenants.

In a recent working paper, Demiroglu, James, and Kizilaslan (2009) examine the determinants of credit line usage among a sample of private firms that either were sold to a public firm or held an initial public offering. These data provide insights into the importance of credit lines to smaller private firms that lack access to public debt and equity markets. The authors find that, for privately held firms, the relative importance of credit lines as liquidity sources is even more sensitive to operating performance than it is for publicly traded firms. These two studies suggest that the likelihood of using a credit line for liquidity depends significantly on the financial condition of the borrower. The poorer the borrower’s credit quality and the more limited its access to capital markets, the more contingent access to credit lines appears to be.

This suggests that market conditions might affect credit-line usage in several ways. First, as credit market conditions tighten and risk spreads increase, borrowers may draw down their lines because interest rates on commitment borrowing is lower than what may be available in the spot credit market. A potentially offsetting effect is that, during recessions, borrowers are likely to experience operating performance declines that limit their access to credit lines. Finally, tighter credit standards may prompt banks to restrict new lines and renew existing lines on stricter terms, potentially forcing businesses to rely on nonbank liquidity sources.

Credit market conditions and credit line usage

Demiroglu, James, and Kizilaslan also examine the relationship between credit market conditions and sources of corporate liquidity for public and private firms from 1997 through 2007. The authors measure credit market conditions using the net percentage of loan officers tightening credit standards based on data from the Federal Reserve’s Survey of Terms of Bank Lending. Tight credit conditions are defined as periods when the net percentage of loan officers tightening credit standards is above the median for the sample period. The authors examine three sources of corporate liquidity: cash, credit lines, and trade credit. Trade credit use is measured by the number of days that payables are outstanding. The longer payables are outstanding, the more trade credit is used to meet liquidity needs. Businesses that delay remittances to trade creditors forgo discounts for timely payment. Therefore, trade credit is generally viewed as an expensive credit source. Increased trade credit usage may indicate that additional credit is not available from such sources as commercial banks.

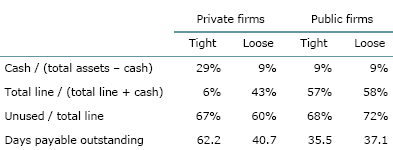

Figure 1

Credit market conditions and sources of corporate liquidity

Figure 1 provides information on liquidity sources under “tight” versus “loose” credit markets conditions, showing significant differences in the patterns of private and public companies. When lending standards are tighter, private firms hold more cash on their balance sheets and rely less on credit lines for liquidity. The increase in the relative importance of cash as a liquidity source during periods of tight credit reflects a reduction in credit-line availability for private firms. Figure 1 shows that line usage, as measured by a line’s unused amount relative to its total amount, does not vary much with credit market conditions. Moreover, privately held firms rely more heavily on trade credit when credit markets tighten. If line size declined because of a reduction in credit demand, then these private firms would not be expected to increase their use of relatively expensive trade credit.

In contrast, liquidity sources for public firms do not vary significantly with changes in bank lending standards. One explanation is that smaller private firms are subject to more restrictive covenants or are more likely to have credit rationed in tough economic times. This explanation is consistent with the finding that credit-line availability for public firms is much less sensitive to operating performance than it is for private firms.

Overall, these findings suggest that credit lines are a more contingent source of liquidity for private as opposed to public firms. It is too early to tell the extent to which this holds during the current credit crisis. On one hand, impaired access to public debt and commercial paper markets may lead public companies to rely more heavily on credit lines for liquidity. Alternatively, capital and liquidity concerns may lead banks to scale back lending to both large public and smaller private businesses during this period. A more intensive look at recent SEC filings may provide some answers.

Christopher M. James, University of Florida and Visiting Scholar, FRBSF

References

Demiroglu, Cem, and Chris James. 2009. “The Information Content of Loan Covenants.” University of Florida working paper.

Demiroglu, Cem, Chris James, and Atay Kizilaslan. 2009. “Credit Market Conditions and the Value of Banking Relationships for Private Firms.” University of Florida working paper.

Shockley, Richard, and Anjan Thakor. 1997. “Bank loan Commitment Contracts, Data, Theory, and Tests.” Journal of Money, Credit, and Banking 29(1), (November).

Sufi, Amir. 2009. “Bank Lines of Credit in Corporate Finance: An Empirical Analysis.” The Review of Financial Studies 22(3).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org