U.S. productivity is growing slower than in the past. Meanwhile, sales have become increasingly concentrated in the largest businesses. Analysis suggests that IT innovation may have facilitated the rise in concentration by reducing the cost for large firms to enter new markets. This contributed to booming productivity growth from 1995 to 2005. Though large firms are more profitable, their expansion may have increased competition and reduced profit margins within markets. Lower profit margins in a given market could have deterred innovation, eventually lowering growth.

Recent productivity growth in the United States is slower than the postwar average. Meanwhile, sales and production in U.S. industries have become more concentrated in a few large firms (Autor et al. 2019). Some people contend that the high level of concentration discourages innovation and has contributed to the slowdown in productivity growth. This concern has been behind several recent proposals to break up large firms or limit their further growth.

This Economic Letter argues that the relationship between productivity growth and concentration is more subtle. We show that the initial rise in concentration was accompanied by a burst of productivity growth and that concentration in local markets may actually have declined. These two patterns are consistent with our theory with coauthors in Aghion et al. (2019), in which we argue that rising concentration was a byproduct of the information technology (IT) revolution, with effects on productivity growth that vary over time.

Comparing trends in concentration and productivity growth

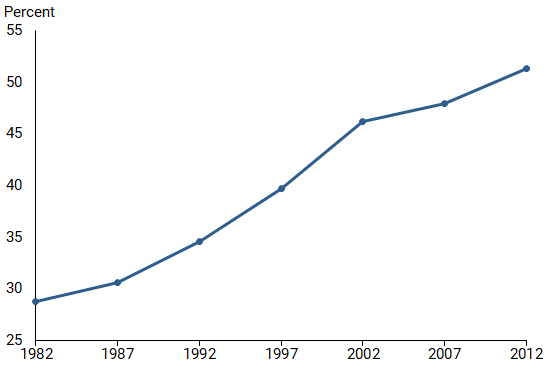

Market concentration is the degree of competition among businesses within a certain industry; a high concentration reflects that a few businesses dominate the market. One intuitive way to measure this concentration is by calculating the share of overall sales among the largest companies. Figure 1 displays publicly available data for the top 20 retail firms’ market share over time. In the early 1980s, their share accounted for less than 30% of sales each year. This steadily increased to over 50% by 2012. Using confidential firm-level data, Autor et al. (2019) found similar increases in concentration across all sectors of the U.S. economy; thus, Figure 1 can be considered broadly representative of economy-wide trends.

Figure 1

Market concentration in retail trade, 1982–2012

Source: Census of Retail Trade, average sales share of top 20 firms in 3-digit industries classified by SIC codes for 1987.

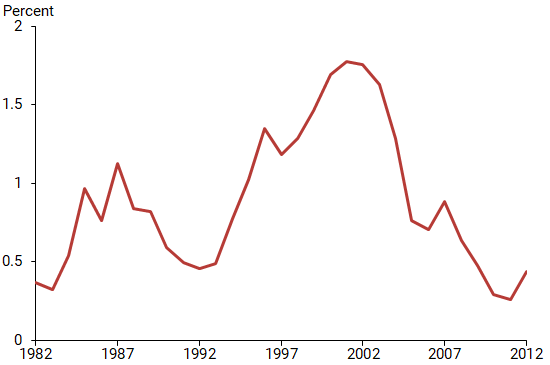

While concentration has increased steadily, productivity growth has fluctuated. Figure 2 is based on the San Francisco Fed’s total factor productivity (TFP) growth data, which measures the difference between output growth and growth in inputs such as capital and labor. Productivity growth is positive when output grows at a faster pace than the growth of physical inputs used in production. This can happen when technology improves. In the figure, we average the raw TFP data over eight-year periods to remove short-term fluctuations and highlight the slower significant technological improvements.

Figure 2

U.S. business productivity growth rate, 1982–2012

Source: Authors’ calculations of 8-year moving average based on Federal Reserve Bank of San Francisco’s Total Factor Productivity series.

Comparing Figures 1 and 2 suggests that the relationship between concentration and productivity growth is not straightforward. While the most recent data show concentration at an all-time high and productivity growth at a historical low, from 1995 to 2005 productivity growth accelerated in tandem with rising concentration. That is, while earlier data suggest concentration may have encouraged productivity growth, recent data suggest concentration may now be hampering productivity growth. To understand the full implications, we need a framework that explains the relationship between concentration and productivity growth over the entire period.

The IT revolution: Concentration and productivity links

To address this puzzle, Aghion et al. (2019) argue that the concentration and U.S. productivity growth patterns as seen in Figures 1 and 2 are driven by a common factor: the IT revolution. New technologies that increased computing power and connectivity reduced the cost for businesses to operate in multiple markets. This enabled large retailers like Walmart to manage distribution networks more efficiently. For example, Holmes (2011) provided evidence that an efficient distribution plan was important for Walmart’s expansion; similarly, Crouzet and Eberly (2019) and others provided evidence that large companies invested a higher share of their revenue in IT. To the extent that businesses qualify as large because they are more productive on average within each market or product category, the expansion of such firms should have contributed to the burst of productivity growth from 1995 to 2005.

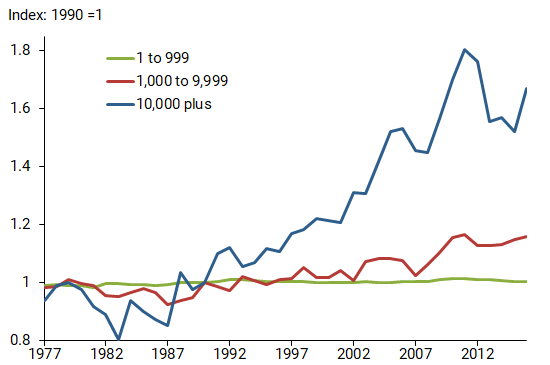

Figure 3 displays evidence that concentration climbed through the expansion of large businesses into more markets. The figure shows the number of establishments per firm by size, defining size as the number of employees listed in the Census Bureau’s Business Dynamics Statistics. The blue line represents firms with more than 10,000 employees. The number of establishments operated by each of these large firms has increased roughly 60% since the early 1980s. By contrast, the number of establishments for medium-sized firms (red line) grew slightly in the latter part of the sample, while the number of establishments for small firms (green line) remained stable throughout this period.

Figure 3

Growth in number of establishments per firm by size

Source: Business Dynamics Statistics by the Census Bureau.

Crucially, the average size of an establishment among large firms did not increase over this period. This implies that large firms expanded by adding establishments in new locales. To the extent that the number of establishments is connected to the number of products or markets, this evidence suggests that large firms increased their national sales share by adding new markets rather than increasing their sales share within existing markets. This is consistent with the rise in concentration coming from lower costs for managing many establishments as a result of the IT revolution.

A complex relationship between competition and innovation

If the initial rise in concentration benefited productivity growth, why did productivity growth eventually slow down? Aghion et al. (2019) link IT expansion to the current low pace of growth in two steps: first, IT expansion increased competition, and second, increased competition eventually deterred innovation.

For the first link, Aghion et al. (2019) argue that firms choose to innovate and introduce new products when the potential profit exceeds the cost of innovation. As a result, the costs of maintaining an additional product or market affect the degree of competition because such costs are akin to innovation costs. High costs discourage firms from innovating to enter new markets and shield existing businesses from competition. When the IT revolution first hit, it reduced the costs of adding new products and encouraged firms to innovate. As large firms expanded, however, they became more and more likely to compete with each other. For example, as Walmart and Target added new locations, they eventually became closer neighbors and competed more directly with each other. Similarly, as Amazon, Apple, and Netflix expanded innovations in video streaming, they began to compete with each other.

This idea that rising concentration in the U.S. economy occurred together with increasing competition is consistent with the findings of Rossi-Hansberg, Sarte, and Trachter (2019). They found that, while large companies have gained shares of national sales, concentration within local markets has actually declined. To the extent that markets are local and firms primarily compete with neighboring firms, concentration measured at the local industry level may be a better proxy for competition than concentration at the national industry level.

However, why does more competition reduce long-run growth? The second leg of the Aghion et al. (2019) hypothesis is that an increase in competition among efficient firms may have lowered how much profit could be gained from further innovation. This, in turn, may have resulted in a slowdown of innovation activities and productivity growth. Indeed, using firm-level data from the Census Bureau, Autor et al. (2019) find the rise in concentration was accompanied by decreasing profit margins within firms.

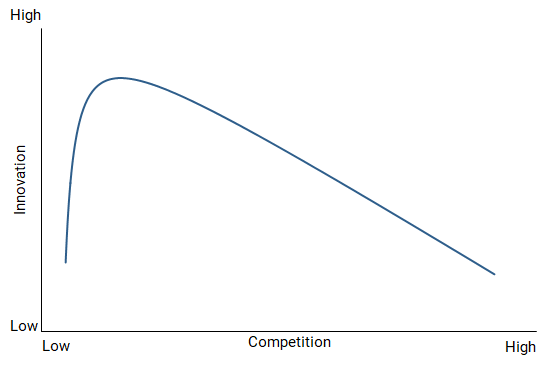

Figure 4 illustrates the relationship between competition and innovation discussed in Aghion et al (2019). The change in innovation with respect to competition depends on the initial level of competition. Innovation increases with competition when competition is low but declines with competition when competition is high.

Figure 4

Relationship between innovation and competition

Source: Aghion et al. (2019).

The reason for the changing relationship between innovation and competition is that they are both driven by changes in the cost of adding new products, which have two opposing effects on the incentives for firms to innovate. On one hand, lower cost directly reduces the cost of adding a new product and encourages firms to innovate. On the other hand, as firms expand, they become more likely to compete against each other through lower prices, which reduces their profit margins. Lower profits discourage innovation. The net impact on innovation depends on which effect dominates. When the initial level of competition is low and there are many untapped markets, the effect supporting innovation dominates. When the initial level of competition is high and there are few untapped markets, however, there is less support for innovation.

Of course, there are other theories for why competition and innovation may have a complex relationship. Aghion et al. (2005) originally theorized that firms competing neck and neck would have a high incentive to innovate to escape competition and earn monopoly profits. They provided evidence for such a relationship across industries. This theory contrasts with the classic hypothesis that higher existing monopoly profits encourage innovation. The bottom line is that the relationship between concentration, competition, and productivity growth is subtle: rising concentration does not necessarily imply declining competition, and more competition does not necessarily stimulate growth.

Conclusion

This Letter argues that the IT revolution contributed to the rise in U.S. market concentration over the past few decades. IT improvements may have enabled efficient firms to expand into new markets and set the stage for the burst of productivity growth in the decade leading up to 2005. The expansion of large firms also may have intensified competition and cut into profits, discouraging them from innovating within markets. This, in turn, could have contributed to the eventual slowdown of productivity growth in recent years.

Our hypothesis underscores the potential tradeoffs for policymakers when considering limiting the growth of large firms. On the one hand, curbing the expansions of large firms can be detrimental to growth in the short run because large firms may be able to provide goods and services at a lower cost. However, curbing their expansions may also sustain profit margins that provide incentives for innovation and stimulate long-run growth. The net impact depends on an array of unknown factors including consumer preferences. Policymakers need to gain a fuller understanding of the tradeoffs to formulate appropriate policy and avoid potential unintended consequences.

Peter J. Klenow is a professor of economics at Stanford University and a visiting scholar in the Economic Research Department of the Federal Reserve Bank of San Francisco

Huiyu Li is a senior economist in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Theodore Naff is a research specialist at the National Bureau of Economic Research.

References

Aghion, Philippe, Antonin Bergeaud, Timo Boppart, Peter J. Klenow, and Huiyu Li. 2019. “A Theory of Falling Growth and Rising Rents.” FRB San Francisco Working Paper 2019-11.

Aghion, Philippe, Nick Bloom, Richard Blundell, Rachel Griffith, and Peter Howitt. 2005. “Competition and Innovation: An Inverted-U Relationship.” The Quarterly Journal of Economics 120(2, May), pp. 701–728.

Autor, David, David Dorn, Lawrence F. Katz, Christina Patterson, and John Van Reenen. 2019. “The Fall of the Labor Share and the Rise of Superstar Firms.” NBER Working Paper 23396.

Crouzet, Nicolas, and Janice Eberly. 2018. “Intangibles, Investment, and Efficiency.” AEA Papers and Proceedings 108, pp. 426–431.

Holmes, Thomas J. 2011. “The Diffusion of Wal-Mart and Economies of Density.” Econometrica 79(1, January), pp. 253–302.

Rossi-Hansberg, Esteban, Pierre-Daniel Sarte, and Nicholas Trachter. 2019. “Diverging Trends in National and Local Concentration.” FRB Richmond Working Paper 18-15.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org