The portion of national income that goes to workers, known as the labor share, has fallen substantially over the past 20 years. Even with strong employment growth in recent years, the labor share has remained at historically low levels. Automation has been an important driving factor. While it has increased labor productivity, the threat of automation has also weakened workers’ bargaining power in wage negotiations and led to stagnant wage growth. Analysis suggests that automation contributed substantially to the decline in the labor share.

A strong labor market and low unemployment traditionally help boost wages. But in the past two decades, the labor share—the portion of national income going to workers—has declined from about 63% in 2000 to 56% in 2018. This decline accelerated during the Great Recession, and the labor share has remained at historically low levels, even with strong employment growth in recent years.

One possible cause of the decline in the labor share is that workers have lost bargaining power over the years. The late economist Alan Krueger highlighted several contributing factors, such as declines in union membership, increased outsourcing and offshoring, and noncompete clauses that hinder workers’ mobility across employers and regions (Krueger 2018).

Another factor to consider is automation. Businesses have more options to automate hard-to-fill positions now than in the past. With rapid advances in robotics and artificial intelligence, robots can perform more jobs and tasks that required human skills only a few years ago. The steady decline in the relative prices of robots and automation equipment over the past few decades have made it increasingly profitable to automate. In this environment, workers may be reluctant to ask for significant pay raises out of fear that an employer will replace their jobs with robots.

In this Economic Letter, we examine the impact of automation on the labor share by looking at its effects on workers’ bargaining power. We show that the threat of automating a job weakens workers’ bargaining positions and thus restrains wage growth in a tight labor market. Although automation boosts labor productivity, the productivity gains do not fully translate into wage gains. We find that automation has contributed to a signification portion of the decline in the labor share over the past two decades. Our theory also helps explain the puzzle of stagnant wage growth in recent years.

The decline in the labor share

The labor share represents the portion of national income that goes to workers. It is the ratio of labor compensation in the form of wages and other benefits relative to the compensation of all factors of production in the economy, which is national income. For a given size of national income, a drop in labor compensation reduces the labor share.

A useful way to think about the labor share is that it is the ratio of real wages to labor productivity. As a result, the labor share would be constant if an increase in labor productivity were matched by an equal increase in real wages. However, the labor share would decline if real wages weren’t able to keep up with increases in labor productivity.

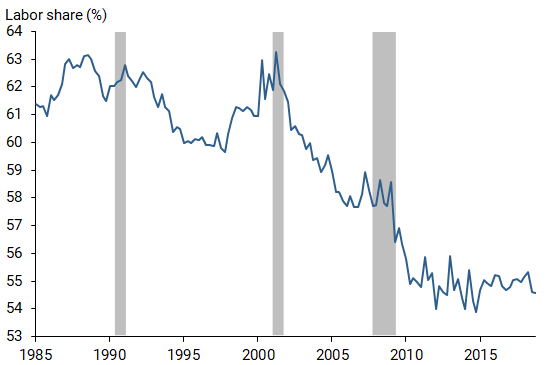

There are practical challenges in measuring the labor share. For example, it is not clear what proportion of self-employment compensation should be counted as labor income (Elsby, Hobijn, and Sahin 2013). As a benchmark, we use the measure of the labor share of the nonfarm business sector constructed by the Bureau of Labor Statistics, shown in Figure 1. The labor share fluctuates over the business cycle, but it stayed around 63% between 1985 and 2000.

Figure 1

Labor share in U.S. nonfarm business sector

Source: Bureau of Labor Statistics. Gray bars indicate NBER recession dates.

Since the early 2000s, however, the labor share has fallen about 7 percentage points. About half of the drop occurred during the Great Recession. Even during the lengthy recovery and expansion, the labor share has stayed around 56%, near the historical low in our sample. The significant decline in the labor share reflects that increases in real wages have not kept up with labor productivity improvements over the past two decades.

Automation, workers’ bargaining power, and the labor share

Economists have long understood that technological improvements that make it easier to automate jobs—so that businesses can substitute capital for labor—can reduce the labor share. For instance, the British economist John Hicks noted the potential link back in the 1930s.

However, in traditional macroeconomic models, productivity improvements triggered, for instance, by automation go hand in hand with rising wages because labor markets in those models are perfectly competitive and frictionless. In other words, wages would instantly adjust until the supply of labor meets demand, leading to full employment. Workers also would be paid for how much an additional hour of work adds to production, known as their marginal products. Thus, traditional macro models predict that a technological improvement that raises workers’ productivity also raises wages. This prediction is inconsistent with recent data, though: the decline in the labor share since the early 2000s has been accompanied by stagnant wage growth. Viewed through the lens of the traditional model, this observation would cast doubts on the importance of automation (Elsby et al. 2013).

In our recent work (Leduc and Liu 2019), we revisit the link between automation and the labor share in a more realistic model of the labor market. Our model features wage bargaining in a labor market with job search frictions. These search frictions capture the reality that businesses and workers are constantly searching to find suitable employment matches and that searching is costly. Businesses need to post vacancies and interview candidates, while job seekers must comb through ads, send résumés, and interview with potential employers. This costly search process implies that there is a range of possible wage rates that businesses and workers could agree upon in forming a job match. The final wage decisions depend on the relative bargaining power between the employers and the job seekers. Also, the wage rates in general do not coincide with the workers’ marginal products. Employed workers are willing to stay in their current positions even when wages fall short of their marginal products, because they would like to avoid the costly search process necessary to find a new job.

In contrast to traditional models with perfectly competitive labor markets, our model predicts that automation can lead to a decline in the labor share, along with stagnant wage growth. Automation gives employers another option in wage negotiations and thus weakens workers’ bargaining power.

To assess the importance of automation for explaining the declines in the labor share, we estimate our model using quarterly data for unemployment, job vacancies, inflation-adjusted wage growth, and labor productivity growth. Our sample covers the period from 1985 to 2018. Fitting our model to the time series of labor productivity, along with the other labor market variables, helps quantify the role of automation. Labor productivity growth has slowed substantially since the mid-2000s and has been particularly weak since the Great Recession (Fernald 2015). However, automation has become increasingly important in recent years and should ultimately affect productivity.

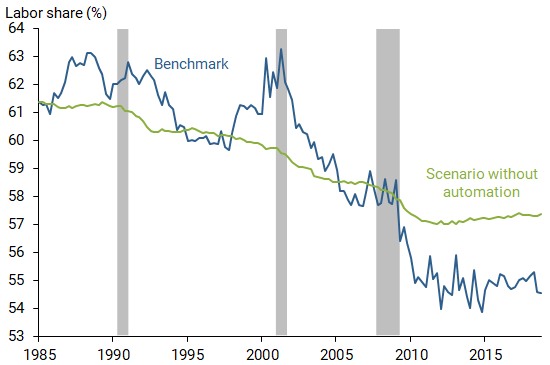

We use our estimated model to evaluate the contribution of automation to the change in the labor share from 1985 to 2018. The contribution of automation is captured by the difference between the actual labor share in the data and that implied by a special scenario using our model in which the degree of automation is kept constant at its long-run average.

Figure 2 shows that the labor share in the special scenario with no changes in automation (green line) does not fluctuate over the business cycle; more importantly, the decline in the labor share would have been much more muted than in the actual data (blue line). Our model predicts that, without automation, the labor share at the end of 2018 would have stayed around 59.5%, much higher than the actual labor share of about 56%.

Figure 2

U.S. labor share: Actual versus scenario without automation

Source: Bureau of Labor Statistics and authors’ calculations. Gray bars indicate

NBER recession dates.

Our model implies that the probability that businesses will automate a job position is procyclical, rising in expansions and falling in recessions, because the net benefits of automation are procyclical. If the automation probability increased in good economic times, then employers would have an alternative option to fill job openings, giving them an upper hand in wage negotiations. The resulting decline in workers’ bargaining power would act as a drag on wage increases, even if productivity improved through automation. In other words, workers would not get all the benefits of rising labor productivity. Our model implies that, if automation had not been a part of the picture over the past two decades, productivity would have risen even less than it actually did, while wages would have risen more.

Although automation weighs on the labor share in our model, it nevertheless has a positive impact on aggregate employment and thus has contributed to the steady decline in the unemployment rate in recent years. The option to automate jobs boosts the incentive for firms to create jobs, because they can adopt a robot to perform the job if the search process fails to yield a match with a worker. Therefore, our model does not predict that automation triggers a form of technological unemployment, as Keynes suggested in the 1930s. Instead, while automation eliminates certain types of jobs, it also generates new ones (see Acemoglu and Restrepo 2018).

Additional evidence

Our model predicts that increases in automation restrain wage increases and thus reduce the labor share. This prediction is in line with other independent empirical studies. For example, David Autor and Anna Salomons (2018) used data from 28 industries across 18 developed countries to show that automation has had a significant negative impact on the labor share, particularly since the early 2000s. They also find that automation did not reduce employment in their sample, consistent with our findings.

The predictions from our model are also consistent with evidence at the establishment level. For instance, Dinlersoz and Wolf (2018) use data from the 1991 U.S. Census Bureau’s Survey of Manufacturing Technology to document that business establishments with more investment in automation experienced greater productivity gains but also larger declines in their labor shares.

Conclusion

The labor share in the United States has declined roughly 7 percentage points over the past two decades. The decline started in the early 2000s and accelerated during the Great Recession. After the recession, the labor share failed to bounce back despite strong employment gains, particularly over the past few years.

In this Letter we argue that automation may have been partly to blame. Having the option to automate jobs strengthens firms’ bargaining power against workers. This keeps wage increases stagnant despite productivity gains. We find that automation contributed substantially to the decline in the labor share since the early 2000s.

Sylvain Leduc is executive vice president and director of research in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Zheng Liu is senior research advisor and director of the Center for Pacific Basin Studies in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Acemoglu, Daron, and Pascual Restrepo. 2018. “The Race between Man and Machine: Implications of Technology for Growth, Factor Shares, and Employment.” American Economic Review 108, pp. 1,488–1,542.

Autor, David, and Anna Salomons. 2018. “Is Automation Labor-Displacing? Productivity Growth, Employment, and the Labor Share.” Brookings Papers on Economic Activity, Spring, pp. 1–87.

Dinlersoz, Emin, and Zoltan Wolf. 2018. “Automation, Labor Share, and Productivity: Plant-Level Evidence from U.S. Manufacturing.” U.S. Census Bureau Center for Economic Studies Working Paper, pp. 18-39.

Elsby, Michael, Bart Hobijn, and Aysegul Sahin. 2013. “The Decline of the U.S. Labor Share.” Brookings Papers on Economic Activity, Fall, pp. 1–63.

Fernald, John G. 2015. “Productivity and Potential Output before, during, and after the Great Recession.” Chapter 1 in NBER Macroeconomics Annual 2014, volume 29, eds. Jonathan Parker and Michael Woodford. Chicago: University of Chicago Press, pp. 1–51.

Krueger, Alan. 2018. “Reflections on Dwindling Worker Bargaining Power and Monetary Policy.” Luncheon address to FRB Kansas City’s Jackson Hole Symposium, August 24.

Leduc, Sylvain, and Zheng Liu. 2019. “Robots or Workers? A Macro Analysis of Automation and Labor Markets.” FRB San Francisco Working Paper 2019-17.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org