The COVID-19 pandemic produced a sharp contraction in capital flows in emerging markets during the spring of 2020. Such contractions are known as “sudden stops” and historically have been associated with significant downturns in a country’s economic activity. Evidence from Mexico’s financial crisis history suggests that sudden stops tend to exhibit a common pattern: the crisis lasts one to two years before a rapid but partial recovery, followed by years of protracted stagnation.

In early 2020, the COVID-19 pandemic hit countries around the world, causing unprecedented disruptions to households and businesses. Financial markets in the United States and abroad seized up, leading to massive disruptions in financial intermediation and access to credit. Emerging economies, in particular, suffered unprecedented outflows of capital.

Although the COVID-19 pandemic has no recent historical comparison, we can look to past financial crises in emerging markets that were driven by rapid capital outflows. Understanding the economic dynamics during and after these so-called sudden stops can provide important insights into how emerging market economies are likely to evolve over the coming years. In this Economic Letter, we use recent models of sudden stops and draw from Mexico’s history of financial crises to derive implications for emerging markets during and after the pandemic.

Our results indicate that sudden stop crises tend to last a year or two. Recoveries from such crises tend to happen rapidly but are only partial. They are then followed by lengthy periods of stagnation, as output and investment languish for years beyond the crisis. Because our analysis focuses solely on the financial crisis aspect and ignores additional disruptions in economic activity caused by the policy attempts or failures to contain the virus, it is plausible to expect that emerging markets will feel the effects of COVID-19 for years to come.

Capital outflows since COVID-19

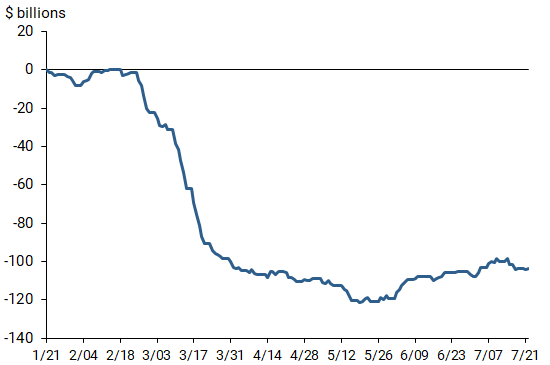

Figure 1 shows the dramatic cumulative amount of capital flowing out of emerging economies during the onset of the pandemic. From February 25 to April 1, 2020, these economies lost more than $100 billion of foreign investments, equivalent to about 3.5% of the international investment position in these countries (International Monetary Fund 2020a). The capital outflows were exceedingly large and rapid, dwarfing the impact of the 2008 Global Financial Crisis. In that earlier crisis, about 2.0% of the international investment position fled emerging markets during a more protracted decline over several months (International Monetary Fund 2020b).

Figure 1

Cumulative portfolio flows from emerging markets in 2020

Source: International Monetary Fund (2020a).

Many emerging economies, such as those in Latin America, were not on the forefront of the caseload for COVID-19 in March and April 2020. The financial contraction caused by foreign investors pulling their funds largely preceded the spread of the disease in those countries (Benigno et al. 2020a).

To assess the dynamics associated with these kinds of crises in emerging economies, we turn to the estimated model in Benigno et al. (2020b). The model considers how different supply and demand shocks are propagated in the economy and how financial frictions can amplify such shocks. In particular, when debt tends to be large relative to collateral, borrowing from abroad—the key source of financing for emerging economies—can become severely restricted because foreigners become less willing to invest. These sudden stops in capital flows produce dramatic swings in economic activity.

Financial crises in Mexico’s history

We look to Mexico’s financial history to identify some common patterns of sudden stops. We focus on Mexico for three reasons. First, this country experienced multiple sudden stops in the recent past that can illuminate the dynamics associated with these episodes. Second, the dynamics of Mexico’s sudden stops are indicative of similar episodes in other emerging economies (Cerra and Saxena 2008). Third, Mexico is part of Latin America, a region that has been hit particularly hard by the current crisis.

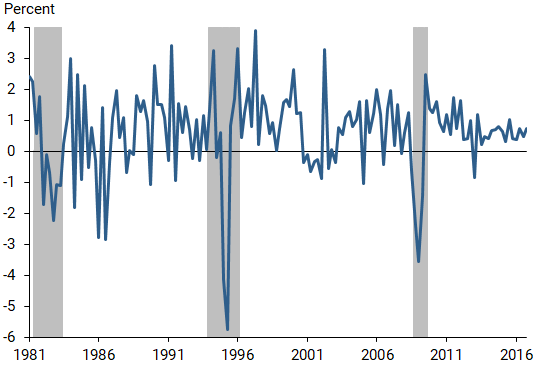

We use the Benigno et al. (2020b) model to analyze Mexico’s business cycle and financial crisis history from 1981 to 2016. Figure 2 shows the substantial volatility and several large negative swings in Mexico’s quarterly output growth over this period. Our model uses this series as one of several inputs to estimate when Mexico experienced financial crises, shown by the gray shaded bars in the figure. The model thus helps differentiate crises from standard business cycle fluctuations by using financial constraints to amplify downturns and track the abnormal output drops during crisis periods. This distinction otherwise would be difficult to capture with traditional business cycle models.

Figure 2

Quarterly output growth and crises in Mexico, 1981–2016

Note: Gray bars denote crisis periods as estimated in Benigno et al. (2020b).

Our model identifies three distinct sudden stop episodes. The first is the early 1980s debt crisis, which lasted eight quarters, from the third quarter of 1981 to the second quarter of 1983. This crisis occurred after debt-fueled growth of the 1970s left Mexico reliant on high leverage and hence susceptible to adverse shocks. While our model indicates that the crisis ended by 1983, the following years saw low average growth with many quarters of outright contraction; this period is commonly referred to as “the lost decade” of the 1980s. The second crisis is the Mexican peso crisis, which lasted nine quarters from the first quarter of 1994 through the first quarter of 1996. This crisis was precipitated by a forced devaluation of the peso in late 1994 triggered by capital flight from the government debt market. Finally, the model identifies the Global Financial Crisis that originated in the United States but produced a sudden stop in capital flows to Mexico lasting four quarters, from the fourth quarter of 2008 to the third quarter of 2009.

Post-crisis recoveries and stagnation

While the three crises our model identified had different origins, each had similar dynamics associated with outflows of capital from the country and substantial losses in output. The sudden stop in 2020 due to the COVID-19 pandemic, therefore, shares key similarities to those earlier episodes that our model is meant to capture. To study the possible implications for the current situation and how emerging economies might evolve in coming quarters and years, we turn to model-based simulations of such crisis episodes. We caution that these simulations are not forecasts. Rather, they are useful as a means of illuminating the key economic forces that will determine the path of future growth in emerging economies like Mexico.

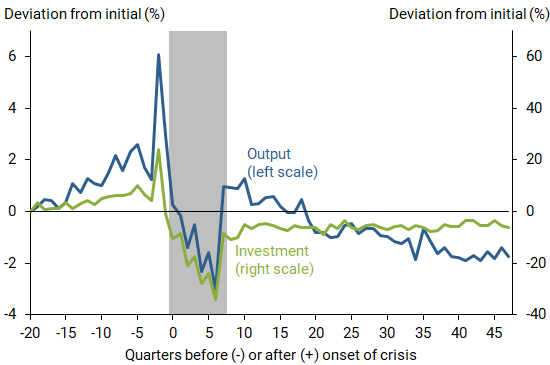

Figure 3 shows the paths for output and investment in a typical simulated crisis from our model. Because crises tend to last a year or two, in this experiment we focus on crises lasting at least eight quarters. We consider a window starting 20 quarters before the onset of the crisis, followed by the eight quarters of the crisis (gray bar) and then the post-crisis recovery.

Figure 3

Model-implied crisis dynamics for output and investment

Note: The figure shows simulation-based crisis dynamics from Benigno et al. (2020a). Gray bar indicates crisis period.

According to the typical scenario, output and investment tend to rise before the crisis as the economy experiences a gradual boom. The boom accelerates as capital and investment increase; these dynamics are associated with rising leverage as debt increases along with the expansion. The crisis is precipitated by some confluence of supply and demand shocks, which pushes the economy against its leverage or borrowing constraint, leading to a massive decline in output and investment as international capital pulls back from the country.

While the COVID-19 shock is a substantial one, our results also indicate financial crises can be generated by otherwise standard shocks that hit an overleveraged economy. Either way, the loss of access to international capital makes it harder for firms to finance their operations, leading to a pullback in production. The pullback of international lending also curtails households’ access to credit, leading to a loss in consumption. Both of these channels reinforce each other in a contractionary spiral. The crisis continues for two years, until the economy has sufficiently reduced its debt to the point that international investors feel comfortable enough to bring capital back into the country.

However, according to our model, the end of the crisis does not necessarily mean that the economy returns to normal. Instead, while there is a fast rebound in activity, it is only partial relative to the pre-crisis level. In fact, a long period of stagnation follows the crisis. While output and investment surge immediately following the crisis, as some funds from abroad resume, they then languish for up to 10 years following the crisis. This stagnation occurs because losses in investment during the crisis make it difficult to expand production in a substantial and sustained manner. In addition, while the process of deleveraging during the crisis lowers the overall debt level, the value of possible collateral decreases as well. Overall, the lack of collateral makes it difficult for firms to finance production and fund investment.

Conclusion

Emerging economies saw an unprecedented outflow of capital during the sudden stop of 2020 due to the COVID-19 pandemic. Our model showing Mexico’s history of financial crises compared with regular business cycles indicates that sudden stops in capital flows last a year or two. Moreover, after the crisis abates, the initial rebound in economic activity is fast but only partial and is followed by years of stagnation.

These results thus indicate that emerging economies are likely to suffer the consequences of the financial shock caused by the COVID-19 pandemic for years to come. A further concern is that our results focus solely on the financial crisis aspect of COVID-19 and do not take into account the unique circumstances created by the spread of disease and the containment policies adopted. The direct effects of the disease act as compounding factors that further weaken emerging markets and limit their ability to fully recover. In other words, what might appear to be a pessimistic outlook due to the financial aspects of the current crisis may in fact have significant risk of turning out worse due to the additional effects of the pandemic.

Gianluca Benigno is an assistant vice president and function head in the International Research Function at the Federal Reserve Bank of New York.

Andrew Foerster is a research advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Christopher Otrok is the Sam B. Cook Professor of Economics at University of Missouri, Columbia, and a research fellow at the Federal Reserve Bank of St. Louis.

Alessandro Rebucci is an associate professor at the Johns Hopkins Carey Business School, a research fellow at the National Bureau of Economic Research, and a research fellow at the Centre for Economic Policy Research.

References

Benigno, Gianluca, Andrew Foerster, Christopher Otrok, and Alessandro Rebucci. 2020a. “Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach.” FRB San Francisco Working Paper 2020-10, October 2020.

Benigno, Gianluca, Andrew Foerster, Christopher Otrok, and Alessandro Rebucci. 2020b. “COVID-19: A Double Whammy of Financial and Economic Sudden Stops for Emerging Economies.” In COVID-19 in Developing Economies, eds. Simeon Djankov and Ugo Panizza. London: VoxEU, pp. 329–341.

Cerra, Valerie, and Sweta Chaman Saxena. 2008. “Growth Dynamics: The Myth of Economic Recovery.” American Economic Review 98(1), pp. 439–457.

International Monetary Fund. 2020a. “EM Capital Flows Monitor.” Monetary and Capital Markets Department, April 1.

International Monetary Fund. 2020b. Global Financial Stability Report: Markets in the Time of COVID-19. Monetary and Capital Markets Department, April 14.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org