The ongoing trend of climate change—including higher temperatures and more extreme weather—will result in economic and financial losses for many businesses, households, and governments. Moreover, the uncertainty about the severity and timing of these losses is a source of financial risk. Recently, the Federal Reserve joined other financial regulators to warn that such climate-related financial risk may threaten the safety and soundness of individual financial institutions and the stability of the overall financial system.

Climate change describes the current trend toward higher average global surface temperatures and the accompanying environmental shifts, such as rising sea levels and more severe storms, floods, droughts, and heat waves. Climate change will have sweeping effects on all aspects of human society including the economy and financial sector. Climate-related shifts in the physical environment can slow economic growth and increase the likelihood of disruptions and reductions in output, employment, and business profitability. Furthermore, the substantial economic transformation required to mitigate and adapt to climate change may lower the value of certain business and household assets in the not-too-distant future.

This Economic Letter describes how uncertainty about the magnitude, scope, and timing of the economic damages from climate change translates into financial risk, which can adversely affect financial markets, asset classes, and institutions as well as the income and balance sheets of businesses, households, and governments. During the past year, U.S. and international financial regulators and supervisors, including the Federal Reserve, have increasingly warned that the uncertainty, volatility, and economic transformation related to climate change can threaten the stability of financial institutions and the financial system as a whole.

Climate change creates physical and transition financial risk

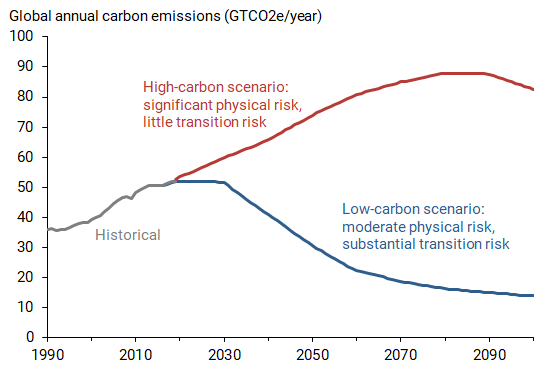

Recent climate change has been driven by increased levels of carbon dioxide (CO2) and other greenhouse gases in the atmosphere. The future path of greenhouse gas emissions will depend crucially on the adoption of climate policies and technological innovations (IPCC 2018). Figure 1 illustrates two potential global carbon emissions scenarios from a wide range of possible alternatives. The “business as usual” high-carbon emissions path (red line) extrapolates recent trends in economic output and energy efficiency. By contrast, in the low-carbon scenario (blue line), effective climate policies and breakthroughs in technology cause greenhouse gas emissions to plateau and then rapidly decrease. This decline primarily reflects a shift away from burning fossil fuels for electricity, heat, and transportation toward renewable energy sources.

Figure 1

Two possible future scenarios for greenhouse gas emissions

Note: Historical data, 1990 to 2019, and baseline and optimistic future scenarios from Climate Action Tracker.

These two scenarios produce different probability distributions for the extent of further climate change. In the high-carbon emissions path, average global surface temperatures are projected to increase about 6 to 9°F by the end of this century relative to the late 1800s. The associated climate-related adverse outcomes—including rising sea levels and more severe storms, floods, and wildfires—can disrupt business operations, damage property, and devalue assets. By contrast, the low-carbon emissions path would likely result in about half as much global warming and less climate uncertainty, especially a lower probability of a climate catastrophe—that is, a smaller so-called tail risk. Still, the low-carbon path requires a transformation of the economy to new energy sources and business models, comparable in magnitude to shifts during the Industrial and Digital Revolutions. This decarbonization of the economy can be timely and deliberate—as shown in the blue line—or it can be delayed and disorderly—say, a late sharp drop from the red line to the blue one. Importantly, financial risk stems from uncertainty not only about the future path of emissions, but also about the associated climate outcomes and policy responses and the resulting economic and financial fallout.

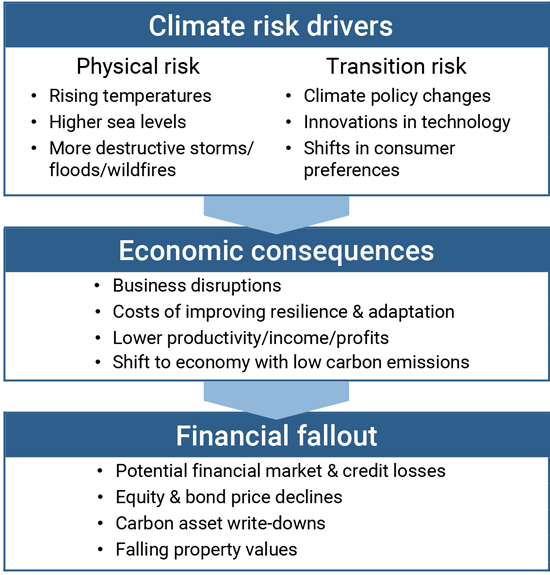

Figure 2 summarizes two key channels for the economic and financial risk from climate change. Physical risk reflects the uncertain economic costs and financial losses from tangible climate-related adverse trends and more severe extreme events. For example, low-lying coastal real estate and public infrastructure face physical risk from higher sea levels and more destructive storms, and hotter temperatures pose chronic risks to human health, worker productivity, and food production. Transition risk stems from the uncertain pace and scope of the economic transformation required to produce fewer carbon emissions. Such decarbonization risks include possible declines in asset prices, income, and profitability in the sectors that rely on high carbon emissions. These risks are most salient for the energy sector, which may face oil reserve write-downs and early decommissioning of fossil fuel power plants, but they are also relevant for transportation, construction, manufacturing, and other industries. Businesses that rely on emissions of greenhouse gases may suffer financial losses and stranded assets. However, a decarbonization will also create new financial opportunities in other sectors, such as electric vehicle manufacturing, although those opportunities could also induce financial risks to asset prices from an overly exuberant low-carbon investment boom.

Figure 2

Economic and financial fallout from climate change

Climate risk drivers include physical risk from rising temperatures, higher sea levels, and more destructive storms, floods, and wildfires. Drivers also include transition risk from such factors as climate policy changes, innovations in technology, and shifts in consumer preferences.

The physical and transmission risks lead to economic consequences, including business disruptions; costs of improving resilience and adaptation; lower productivity, income, or profits; and the shift to an economy with low carbon emissions.

From these consequences, the financial fallout can include potential financial market and credit losses, equity and bond price declines, carbon asset write-downs, and falling property values.

The bottom line is that every future scenario includes climate-related financial risk, though the level and form of the underlying uncertainty vary. A high-carbon scenario would generate considerable physical financial risk from uncertain extreme events and adverse trends. A low-carbon path would moderate such climate hazards but produce transition financial risk from the possible adoption of new climate policies and technology.

Financial regulators are requiring more climate risk assessment

While climate-related financial losses and risks could harm a wide range of individuals and institutions, central banks and financial regulators have increasingly worried about the implications for the financial sector (Rudebusch 2019). These are some of their official initiatives of the past year:

- The Bank of England provided details of an upcoming climate risk stress exercise for major U.K. banks and insurers including a 30-year time horizon (Bailey 2020). The central banks of France and the Netherlands have similar examinations completed or underway (CFTC 2020).

- The European Central Bank described its supervisory expectations related to the management and disclosure of climate-related risks by financial institutions (ECB 2020).

- The Network of Central Banks and Supervisors for Greening the Financial System issued a guide to assist in quantifying how bank lending portfolios and balance sheets react to climate risk (NGFS 2020).

- The United Nations issued detailed handbooks (UNEP FI 2020a, 2020b) on the physical and transition risks of climate change that financial institutions must identify and manage.

- The Basel Committee on Banking Supervision (BIS 2020) surveyed supervisory actions that can lessen climate risks to banks.

- The Commodity Futures Trading Commission released a landmark report (CFTC 2020) that argued: “U.S. financial regulators must recognize that climate change poses serious emerging risks to the U.S. financial system, and they should move urgently and decisively to measure, understand, and address these risks.”

- The New York State Department of Financial Services asked financial institutions under its supervision to incorporate climate-related risks (DFS 2020).

- The Securities and Exchange Commission’s current acting chair called for financial institutions to disclose their climate risks including those associated with the financing they provide (Lee 2020).

The Federal Reserve has joined these efforts on two broad levels. First, regarding the microprudential oversight of risk management at individual financial institutions, the Fed (BOG 2020a) noted its supervisory expectation that these institutions should “monitor all of their material risks, which for many banks are likely to extend to climate risks.” For example, as a result of climate-related risks, business assets or property may become damaged or less profitable, and financial institutions may need to absorb the associated credit and marketable securities losses. Financial institutions also face risks to their own operations because acute climate events can close offices and data centers. In this way, climate change can affect financial institutions through the traditional supervisory risk categories of credit, market, and operational risk (Alvarez et al. 2020).

A useful tool for calibrating these risks is climate scenario analysis, which explores the repercussions for financial institutions from different climate-related outcomes (Brainard 2020). Essentially, high-level scenarios like those in Figure 1 are expanded to quantify how specific bank lending portfolios and balance sheets react to the drivers of physical and transition risk. There are many challenges to such detailed risk assessments including the requisite long time horizons of a decade or more. Climate risks may also diverge sharply from the past—for example, the occurrence of several 100-year floods in quick succession—which makes the historical record less useful for calibrating uncertainty. Climate hazards also vary widely across local geography and industry, so risk assessments require granular data about the type and location of the underlying assets. Finally, the extent of climate-related losses by financial markets and institutions depends on who holds the relevant assets and their risk management and loss-absorbing capabilities (Stiroh 2020).

A second Fed initiative in late 2020 (BOG 2020b) signaled that climate risk is relevant to its macroprudential oversight of the overall financial system. The Fed stated that it “will monitor and assess the financial system for vulnerabilities related to climate change through its financial stability framework.” Macroprudential oversight provides a holistic supervisory assessment of financial system stability, a response to the interconnected risk management failures during the 2008 global financial crisis. Relative to that episode, the financial impacts of climate change appear even more complex, uncertain, opaque, and persistent. As a result, there is considerable scope for abrupt shifts in perceived climate risks and a rapid repricing of assets threatened by climate change or reliant on carbon emissions. The greater likelihood of such a disruptive, cascading asset repricing could increase financial vulnerabilities. In this way, both the physical and transition risks of climate change could pose a threat to financial stability (Brainard 2020).

One macroprudential approach to assessing climate-related financial risk is a climate stress test. Current stress tests evaluate how vulnerable large financial institutions are to adverse macroeconomic shocks, like a recession, over the next few years. Regulators in other countries—notably, in Great Britain, Canada, France, and the European Union—are exploring the ability of climate risk stress tests to assess the solvency of financial institutions across a range of future climate change outcomes. These are preliminary attempts to understand the resiliency of the financial system to climate risks (CFTC 2020). Climate risk stress tests must account for complex behavioral responses, feedback effects, and nonlinearities but may help quantify the risk vulnerability of the financial system.

Conclusion

The effects of climate change are inescapable and include far-reaching economic and financial consequences for many households and businesses. However, the precise magnitude, timing, and form of these effects are uncertain. Over the past year, central banks and financial supervisors around the world—including the Federal Reserve—have made progress on a path to identify, assess, and manage the resulting climate-related financial risks.

Glenn D. Rudebusch is senior policy advisor and executive vice president in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Alvarez, Nahiomy, Alessandro Cocco, Ketan B. Patel. 2020. “A New Framework for Assessing Climate Change Risk in Financial Markets.” Chicago Fed Letter 448.

Bailey, Andrew. 2020. “The Time to Push Ahead on Tackling Climate Change.” Speech, November 9.

BIS. 2020. “Climate-Related Financial Risks: A Survey on Current Initiatives.” April.

BOG. 2020a. Supervision and Regulation Report. Board of Governors of the Federal Reserve System. November.

BOG. 2020b. Financial Stability Report. Board of Governors of the Federal Reserve System. November.

Brainard, Lael. 2020. “Strengthening the Financial System to Meet the Challenge of Climate Change.” Speech, December 18.

CFTC. 2020. Managing Climate Risk in the U.S. Financial System. September.

DFS. 2020. “Letter to the Chief Executive Officers or the Equivalents of New York State Regulated Financial Institutions, re: Climate Change and Financial Risks.” October 29.

ECB. 2020. Guide on Climate-Related and Environmental Risks. November.

IPCC. 2018. Global Warming of 1.5°C. Intergovernmental Panel on Climate Change Special Report. Geneva, Switzerland.

Lee, Allison. 2020. “Playing the Long Game: The Intersection of Climate Change Risk and Financial Regulation.” Speech, November 5.

NGFS. 2020. Guide to Climate Scenario Analysis for Central Banks and Supervisors. Network for Greening the Financial System, June.

Rudebusch, Glenn D. 2019. “Climate Change and the Federal Reserve.” FRBSF Economic Letter 2019-09 (March 25).

Stiroh, Kevin. 2020. “Climate Change and Risk Management in Bank Supervision.” Speech, March 4.

UNEP FI 2020a. Charting a New Climate. UN Environment Programme Finance Initiative. September.

UNEP FI 2020b. Beyond the Horizon. UN Environment Programme Finance Initiative. October.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org