The COVID-19 pandemic has caused massive disruptions to the U.S. educational system. Research on school closures—particularly combined with parental income loss—implies that children are likely to attain lower levels of lifetime education compared with pre-pandemic trends. Projections show learning disruptions could lower the level of annual economic output ¼ percentage point on average over the next 70 years. The effect is small the first 5–10 years then peaks at a loss of ½ percentage point in about 25 years, when the children reach prime working age.

The COVID-19 pandemic continues to severely disrupt most aspects of everyday life. One of the most significant changes has been the massive shift towards online schooling. The weekly Household Pulse Survey by the Census Bureau shows that nearly 86% of U.S. students at all levels had transitioned to some form of remote learning as of November 2020. The change in educational structure appears disruptive for learning, at least in the near term. In the Census Bureau survey, 45% of students reported spending less time on schoolwork than before the pandemic.

The children of today form the workforce of tomorrow. Hence, widespread disruptions to current learning may reduce the productivity of the economy in the long run if they lead to lower lifetime educational attainment for many children around the country. In this Economic Letter, we gauge the potential impact of these learning disruptions on the future productive capacity of the economy.

The importance of education for overall output

A standard way to study the sources of change in aggregate economic output, or GDP, is known as “growth accounting.” Long-run growth accounting breaks output changes into changes in labor and in productivity, meaning the efficiency of the economy in using labor inputs. This method assumes capital inputs rise with labor and productivity, because the ratio of capital to output has been stable over long periods of time.

Education influences the effective amount of labor—its quantity and quality—in the economy. First, the employment rate tends to increase with higher educational attainment. Second, education raises the general skill level of workers. For example, high school teaches general math and language skills that are useful in most jobs, while education at the college level and beyond provides specialized skills required for professional jobs, such as engineers, scientists, and programmers.

Growth accounting quantifies the contribution of education to aggregate output by measuring how the quantity and quality of labor changes with education. The quantity component reflects the rise in employment rate with education, while the quality component reflects workers with more education tending to earn more per hour, depending on experience and occupation. Thus, in the accounting framework, education raises the number of workers as well as their productivity.

Using the growth accounting methodology, many papers have found that rising educational attainment was an important driver of increasing prosperity in the United States after World War II. For example, Fernald and Jones (2014) find that rising educational attainment accounts for one-fifth of growth in output per hour between 1950 and 2007, while Bosler et al. (2016) find that changes in the education composition of workers played an important role in productivity growth around the 2008–09 recession. Given education’s historical importance, it is possible that the pandemic’s widespread disruption to learning could have a long-lasting impact on the U.S. economy.

Estimating the impact on educational attainment

To gauge the overall impact of learning disruptions, we use the growth accounting method in Bosler et al. (2016). We first estimate how disruptions will affect the lifetime educational attainment of the workforce. Given that physical school closures began less than a year ago, only preliminary estimates are available and many uncertainties surround future health and policy outcomes. Hence, we determine a plausible baseline magnitude and then discuss factors that can affect the magnitude.

For our baseline, we use the estimates of educational attainment from Fuchs-Schündeln et al. (2020). The authors argue that pandemic-induced school closures amid widespread job and income loss among parents have reduced investment in children’s education and will result in some attaining a lower level of education in their lifetime. The negative shock to parental income is relevant because it restricts parents’ ability to offset educational losses with supplementary instruction such as tutoring.

Fuchs-Schündeln et al. (2020) consider a 25% lower investment in public education over two years amid parental income losses of about 5%. In this scenario, the authors estimate a 0.5 to 0.9-percentage point decline in the share of children ages 4 to 14 who eventually finish a bachelor’s degree or higher and a 0.3 to 1 percentage point increase in the share that never finishes high school. The share of high school graduates increases somewhat because some potential college enrollees choose to stop at high school.

Potential impact on aggregate output

To translate the estimates of Fuchs-Schündeln et al. (2020) into an impact on aggregate output, we first calculate the change in the educational composition of the labor force for many years in the future. Fuchs-Schündeln et al. (2020) estimate that the share of children age 14 today who will finish college will drop about 0.7 percentage point, from 28.2% to 27.5%. This implies a 2.4% reduction in the number of children in this cohort that will finish college. Looking ahead 25 years, for example, the impact on today’s 14-year-old students implies a 2.4% decline in the number of college-educated 39-year-olds in 2045. We calculate this 25-year impact for each cohort currently aged 4 to 14—the range analyzed by Fuchs-Schündeln et al. 2020—and then calculate the average change in the number of workers for each education level.

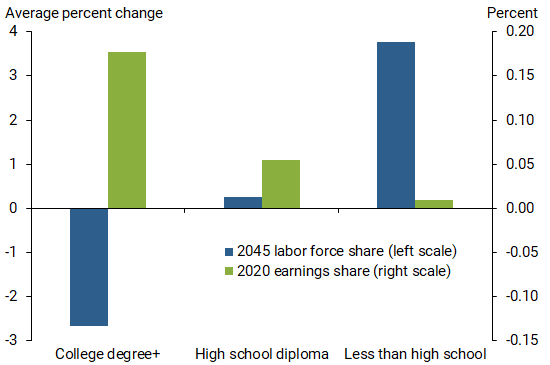

On average, we find that learning disruptions today may reduce the number of college-educated workers ages 29 to 39 in 2045 by 2.7% and increase the number of workers in that age group with less than high school education by 3.8% (blue bars in Figure 1).

Figure 1

Estimated change in labor force in 2045 by earnings share

How costly is this reduction in educational attainment for the economy? Compared with average earnings in 2020 (green bars), Figure 1 shows that college-educated workers ages 29 to 39 accounted for nearly one-fifth of total earnings in 2020, while those with less than a high school education accounted for less than 1%. Growth accounting interprets this difference as higher productivity from a college education. Hence, the negative relationship between current earnings share and future labor force changes arising from the pandemic in Figure 1 suggests that current learning disruptions will reduce the productivity of the future workforce.

To translate the negative relationship in Figure 1 to an overall impact, we add up the weighted changes in worker numbers at each education level, multiplying each group by its share of total earnings. We construct the earnings share of each group in 2045 by adjusting the earnings share in 2020 to account for the Census projection of the age composition in 2045. We arrive at a decline in quality-adjusted labor of slightly less than half a percentage point. In the long run, since capital adjusts, changes in labor tend to translate one-for-one into changes in output. Hence, the disruption to learning today could plausibly lower the level of aggregate output in 2045 by about half a percentage point. This is an economically significant reduction.

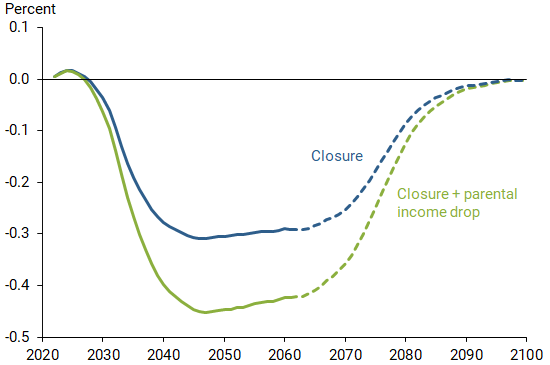

The estimated half-point loss is for a single year, with lower projections for other years before and after 2045. To understand the cumulative effect, we follow the same procedure to create a time profile of output losses from pandemic-induced school closures. Since Census projections of age composition are only available through 2060, we construct the post-2060 age composition based on 2020 data.

The green line in Figure 2 shows a small initial effect because children are not a significant fraction of the workforce. The initial effect is mildly positive because some children choose to enter the workforce after high school instead of going to college. However, the impact becomes increasingly negative as groups reach prime working age. The negative effect peaks at 0.5% from 2045 to 2050 when the affected children reach ages 29 to 39 and the earnings share differences by education groups are the largest. The effect lasts through 2091, when the affected cohorts will have retired. On average, the path of output will be 0.23 percentage points lower over the next 70 years because of pandemic school closures.

Figure 2

Impact of learning disruptions today on level of future GDP

The effect on annual growth rates is relatively modest. For example, having 0.5 percentage points lower output in 25 years is equivalent to reducing average growth over this period by 2 hundredths of a percentage point per year. This annual loss may appear small when compared with pre-COVID projections by Fernald and Li (2019) of 1.6% annual U.S. long-run output growth. However, it is significant in level because the U.S. economy is large. Using the Congressional Budget Office projection of potential output, the loss in 2045 is just shy of $150 billion adjusted for inflation. Moreover, the cumulative loss is substantial because it persists until the affected cohorts retire.

Other factors affecting learning disruptions

Figure 2 also shows that the magnitude of the impact from school closures depends on how parental income is affected. Fuchs-Schündeln et al. (2020) estimate that when parents’ income is unaffected (blue line), the impact on changes in students’ lifetime educational attainment declines by about one-third at its peak because parents are better able to make up for the loss of education. This suggests that the long-run effects of learning disruptions on the economy will depend crucially on how fast the economy recovers, which will impact how much lost education during the pandemic can be remediated.

A few factors suggest our estimates may understate the pandemic’s true impact on future output. Our analysis does not cover students 15 years or older, whose human capital accumulation may have also been disrupted during the pandemic. Furthermore, the estimates in Fuchs-Schündeln et al. (2020) assume a 25% reduction in education over two years and employment recovery by the third quarter of 2020. However, many schools continue to struggle with virtual or hybrid classroom setups, and the employment recovery has stalled in recent months, especially among lower educated groups. Hence the length of recovery and the scale of education loss may be more damaging than the scenario underlying the results in Figure 2. Finally, given education’s importance for fostering new ideas, lower attainment may also decrease future innovation and research development.

Beyond productivity, the disruption to schooling may exacerbate income inequality. Fuchs-Schündeln et al. (2020) find that educational attainment of children from poorer households is likely to decline more because their parents may have fewer resources to make up for school disruptions.

Conclusion

The COVID-19 pandemic continues to pose considerable challenges to the economy and the educational sector. This Economic Letter demonstrates that disruptions to children’s learning today can have a persistent and large impact on the production capacity of the economy and harm future growth. Lower parent incomes have exacerbated the situation. Policies to mitigate income losses for parents and raise incentives for students to continue their education may help offset these long-run losses caused by the pandemic.

John Fernald is a senior research advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Huiyu Li is a senior economist in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Mitchell Ochse is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Bosler, Canyon, Mary C. Daly, John G. Fernald, and Bart Hobijn. 2016. “The Outlook for U.S. Labor-Quality Growth.” FRB San Francisco Working Paper 2016-14.

Fernald, John, and Charles I. Jones. 2014. “The Future of U.S. Economic Growth.” American Economic Review 104(5, May), pp. 44–49.

Fernald, John, and Huiyu Li. 2019. “Is Slow Still the New Normal for GDP Growth?” FRBSF Economic Letter 2019-17 (June 24).

Fuchs-Schündeln, Nicola, Irina Popova, Alexander Ludwig, and Dirk Krueger. 2020. “The Long-Term Distributional and Welfare Effects of COVID-19 School Closures.” NBER Working Paper 27773.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org