How households expect inflation to evolve plays an important role in explaining overall inflation dynamics. Household expectations rose dramatically over the past year or so, much faster than professional forecasters’ inflation expectations. News coverage can explain part of this growing gap. Analyzing the volume and sentiment of daily news articles on inflation suggests that one-fourth of the increased gap between household and professional expectations can be attributed to heightened negative media coverage. These results highlight the important impact of the content and tone of economic information on the real economy.

Inflation rose substantially after its pandemic low in the spring of 2020, reaching its highest level in 40 years during the summer of 2022. The June 2022 peak for the consumer price index (CPI) showed year-over-year inflation of 9.1%. Research suggests that this reflected a combination of pandemic-related supply bottlenecks, higher demand, and supply disruptions of oil, natural gas, and food commodities due to the war in Ukraine (Barnichon, Oliveira, and Shapiro 2021 and Shapiro 2022). Alongside this surge, professional forecasters raised their inflation outlook, expecting that some degree of this heightened inflation would persist.

Compared with professional forecasts, expectations of future inflation among households grew even faster. This gap has caused concern for policymakers because household inflation expectations play an important role in determining where future prices and wages are actually headed (Coibion and Gorodnichenko 2015). One reason why the two measures diverged may be because households digest different information than professionals do when deriving their inflation outlooks. Indeed, past research has shown that household inflation expectations may be overly sensitive to goods, such as gasoline, with prices that are very visible or “salient” (Trehan 2011).

In this Economic Letter, we examine the role of the news media in driving the gap between households’ and professional forecasters’ inflation expectations. To do this, we construct novel measures of both the volume and the tone of inflation news coverage. We first show that there has been a striking increase in the amount of inflation news articles as well as the negativity of those articles in recent months. We then estimate the historical average effect of these news variables, controlling for the impact of other factors—such as price changes for gasoline and food—on the gap between households’ and professional forecasters’ inflation expectations.

We find that an increase in negative inflation news tends to push household expectations away from professional forecasts, while favorable inflation news tends to shrink the gap. We find that the increased volume and negativity of inflation news explains one-fourth of the widening gap between household expectations and professional forecasts from June 2021 to June 2022.

Recent inflation expectations

Empirical research shows that household inflation expectations play a large role in explaining inflation dynamics (Coibion and Gorodnichenko 2015). Elevated inflation expectations can push up actual inflation, setting off an inflationary spiral. This has raised concerns that recent high inflation expectations could become entrenched into actual inflation.

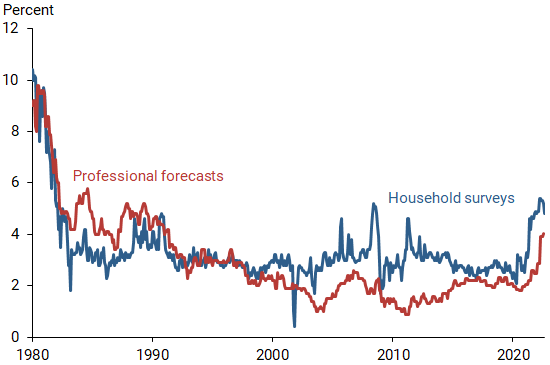

Measures of household inflation expectations rose substantially between the summers of 2021 and 2022. Figure 1 plots for each date the median expected rate of inflation over the next year from the University of Michigan’s nationwide survey of households (blue line). It also shows a measure of professional forecasters’ expectations for 1-year-ahead inflation (red line). This professional forecaster series comes from two sources. For 1980 to 2016, we use the Federal Reserve Board’s internal staff forecasts, known as the Greenbook and Tealbook. Because these documents are not publicly available beyond 2016, we use the average from Consensus Forecasts, a survey of a large number of institutional forecasters conducted by Consensus Economics.

Figure 1

Household, professional forecaster inflation expectations

Source: Consensus Economics, University of Michigan Surveys of Consumers, Federal Reserve System, and authors’ calculations.

Note: Inflation expectations are for one year ahead.

Figure 1 shows that inflation expectations rose from early 2020 through the summer of 2022, but household expectations grew more than professional forecasts. The gap between household expectations and professional forecasts increased especially sharply—by 0.91 percentage point—between June 2021 and June 2022.

What explains this divergence in inflation expectations? Past studies have shown that price changes for gasoline and food tend to affect household expectations more than they affect actual inflation, likely due to their particular salience for households (Trehan 2011). Gasoline and food prices rose sharply over the same period. However, another factor may have been at work—the news. The news media has been intently focused on inflation, which may have caused households to think more about, and hence worry more about, how future inflation would evolve.

Recent inflation news

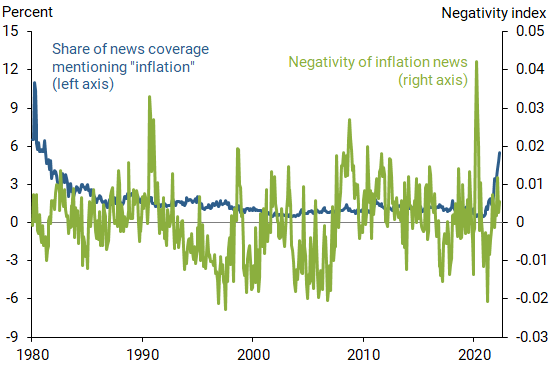

To check whether inflation news coverage is indeed historically high, we apply text analysis tools to a large historical database of print and online news articles. The database of articles covers 24 major U.S. newspapers and comes from the Factiva news aggregator service. We use data from 1980 to the present to simply calculate the share of articles that mention the word “inflation.” We refer to this as the volume of inflation news coverage.

We are also interested in the tone or sentiment of the inflation news. To measure the sentiment of the inflation news articles, we apply the sentiment analysis algorithm developed in Shapiro, Sudhof, and Wilson (2022). This is the same sentiment algorithm used to construct the San Francisco Fed’s Daily News Sentiment Index. The algorithm provides a continuous measure of the sentiment of the news, ranging from –1 for maximum positivity to +1 for maximum negativity.

Figure 2 plots both the volume of inflation news coverage (blue line) and the inflation news negativity (green line) from 1980 to present. Both the volume and negativity are currently elevated. The volume of coverage is at levels not seen since the early 1980s, while negativity has risen substantially over the past year. As Figure 2 shows, it is rare for both of these factors to be elevated at the same time. This suggests a kind of perfect storm of high volume and unfavorable inflation news coverage.

Figure 2

Volume and negativity of inflation news

Source: Factiva Analytics and authors’ calculations.

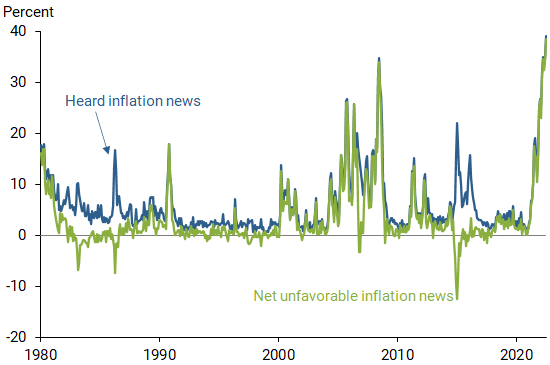

These aggregate measures of inflation news coverage and sentiment can be compared to similar information from the University of Michigan household survey. In that survey, households are first asked, “During the last few months, have you heard of any favorable or unfavorable changes in business conditions?” Those that answer yes are then asked to specify what topics they heard. For responses that mention “prices,” the interviewer classifies the responses as being “favorable news: lower prices” or “unfavorable news: higher prices.”

Figure 3 shows both the percent of survey respondents that report hearing news about prices (blue line) and the net amount of unfavorable news, which is the percent reporting unfavorable news minus the percent reporting favorable news (green line). Consistent with our newspaper-based measures, the survey data indicate that both the share of households receiving news about prices or inflation and the unfavorable tone of that news have been elevated over the past year.

Figure 3

Household survey results for inflation, unfavorable news

Source: University of Michigan Surveys of Consumers and authors’ calculations.

Does the news move household expectations relative to professional forecasts?

The patterns over time hint at the possibility that the elevated volume of inflation news coverage and its negativity could have contributed to the widening gap between household inflation expectations and professional forecasts over the past year. To examine this link more rigorously, we turn to the household-level microdata from the University of Michigan survey.

We first examine whether and how the gap between household expectations and professional forecasts is affected by simply receiving inflation news. Looking only at how a given household’s inflation outlook changes after that household reports whether or not it has heard inflation news is problematic. For example, if a household expects inflation to change, it may also be more inclined to read news about inflation. This means that households’ reports about hearing inflation may both affect and be affected by inflation expectations.

To address this issue, we use a common two-stage estimation method. The first stage predicts the likelihood than an individual will report hearing inflation news based solely on the volume of inflation news coverage in the prior month. Then, in the second stage, we estimate how the likelihood of hearing inflation news—predicted by last month’s volume—affects the household’s inflation expectations gap.

In the same analysis, we estimate the effects on the gap from recent changes in gasoline prices, food prices, housing rents, and core CPI inflation; core inflation strips out food and energy inflation. Including these recent price changes ensures that any effects we find from news coverage are above and beyond the effects of the media’s reporting of actual inflation data. Finally, not all respondents answer the survey question on hearing about business conditions, so a respondent’s likelihood of answering could be related to their inflation expectations and their attention to inflation news. To account for this individual-level likelihood, we include so-called household fixed effects. This is possible to do because respondents are surveyed more than once.

We find that the simple binary variable measuring whether or not a household has heard inflation news does not have a significant effect on the gap. However, it turns out that this result reflects offsetting effects of favorable and unfavorable inflation news. Specifically, we repeat this regression but split the heard inflation news indicator into separate indicators for whether the household reported hearing favorable or unfavorable inflation news. These two separate indicators also could be affected by inflation expectations and not simply be drivers of inflation expectations. Thus, we use first-stage regressions to predict each of these two variables using lagged values for volume and negativity of inflation news as predictors. Taken together, the volume and negativity indicators strongly predict both the favorable and unfavorable inflation news outcomes. The results of the new second-stage regressions show that favorable inflation news reduces the gap between household expectations and professional forecasts, while unfavorable news increases the gap.

To infer the implications for the recent episode, we do a simple back-of-the-envelope calculation to quantify how much the increases in the volume and negativity of inflation news can explain the 0.91 percentage point increase in the average household’s inflation expectations gap from June 2021 to June 2022. We estimate that the increase in volume and negativity of inflation news explains about one-fourth of the widening gap between household and professional forecasts. The remainder, according to this simple regression model, can be attributed to increases in gas and food prices and unobserved factors.

Conclusion

Because household inflation expectations play an important role in explaining overall inflation dynamics, their dramatic climb over the past year or so has become a cause for concern. Our analysis shows that a significant portion of the run-up in household inflation expectations relative to professional forecasts is attributable to heightened negative news coverage of inflation. This suggests that continued extensive and negative news coverage of inflation could pose a risk for household inflation expectations becoming entrenched and contributing to higher inflation itself. More generally, these results demonstrate the importance of the content and tone of economic information in impacting the economy.

Augustus Kmetz is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Adam H. Shapiro is a vice president in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Daniel J. Wilson is a vice president in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Barnichon, Regis, Luiz E. Oliveira, and Adam Hale Shapiro. 2021. “Is the American Rescue Plan Taking Us Back to the ’60s?” FRBSF Economic Letter 2021-27 (October 18).

Coibion, Olivier, and Yuriy Gorodnichenko. 2015. “Is the Phillips Curve Alive and Well After All? Inflation Expectations and the Missing Disinflation.” American Economic Journal: Macroeconomics 7(1), pp. 197–232.

Shapiro, Adam Hale. 2022. “How Much Do Supply and Demand Drive Inflation?” FRBSF Economic Letter 2022-15 (June 21).

Shapiro, Adam Hale, Moritz Sudhof, and Daniel J. Wilson. 2022. “Measuring News Sentiment.” Journal of Econometrics 228(2), pp. 221–243.

Trehan, Bharat. 2011. “Household Inflation Expectations and the Price of Oil: It’s Déjà Vu All Over Again.” FRBSF Economic Letter 2011-16 (May 23).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org