Economic security depends on both jobs and stable prices. Together, these two congressionally mandated goals constitute the Fed’s dual mandate. This mandate is not a choice between two desirable things. It is a balance meant to deliver on a singular goal—a sustainable and expanding economy that works for everyone. The following is adapted from remarks by the president of the Federal Reserve Bank of San Francisco at Boise State University on September 29.

I’d like to start by talking briefly about the Federal Reserve’s congressionally mandated goals, which together form what is known as our dual mandate. One part of that mandate is full employment. The other is price stability (see Board of Governors 2022a).

Now, these goals are often characterized as tradeoffs. More of one means less of the other. But for most people, they are deeply intertwined.

I know this from my many years as a policymaker. But I also know it from experience.

I grew up in Ballwin, Missouri, during the Great Inflation of the 1970s. Rapidly rising prices made it hard for working families like mine to afford the things we needed. Eventually, the Federal Reserve raised interest rates and inflation came down. But the abruptness and magnitude of the response caused two painful recessions. Unemployment soared. Jobs became tough to find. And one impossible situation gave way to another.

I didn’t know it then, but this experience would teach me an enduring lesson, one that I would carry with me over the course of my career as a policymaker. The lesson is that economic security depends on both jobs and stable prices. Together, these two pillars form the foundation for everything else.

Seen in this light, the Federal Reserve actually has a singular purpose: to keep the economy on a sustainable path by delivering low, stable prices and durable labor market strength.

Today, I am going to discuss this singular purpose and how price stability and full employment work together to support it.

Inextricably linked

If you travel almost anywhere in the United States these days, you’ll hear two things about the economy. The first is that the labor market is strong. The second is that inflation is high.

Both of these things are true.

Virtually anyone who wants a job can find one. Unemployment is extremely low and has been so for some time. Job growth continues to run well above 300,000 per month, about 200,000 jobs more than we need to keep pace with new graduates and others entering the labor force (see the Atlanta Fed Jobs Calculator). All of this adds up to about twice as many vacant positions nationwide as there are people wanting to fill them. As any business owner will tell you, this puts considerable pressure on wages and salaries.

So it’s a great time to be a worker, right?

Well, not so much. Inflation is high, running well over the Fed’s average 2% target for well over a year now. This can be traced back to a number of factors, but it boils down to a large and persistent imbalance between demand and supply. Demand has been supported by pandemic-related monetary and fiscal relief, robust household savings, and, over the past year, a very strong labor market. At the same time, domestic and global supply have been highly constrained, hit by a series of negative shocks, including the pandemic, the war in Ukraine, and severe labor shortages.

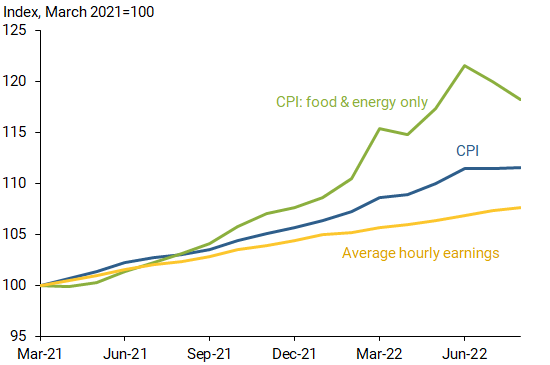

Persistent high inflation across a broad range of goods and services is eroding the purchasing power of earnings, even those that are rising. This erosion is insidious—a gradual, but persistent chipping away of living standards. The picture makes this clear (see Figure 1). Price inflation measured by the consumer price index, or CPI, has been rising far faster than average hourly earnings. Indeed, average real wages, which take account of inflation, have declined by 9% over the past two years. This means that the average worker in the U.S. economy has lost rather than gained ground, all while the labor market remains historically strong.

Figure 1

CPI inflation and average hourly earnings

Note: seasonally adjusted data.

Source: Federal Reserve Economic Data, Bureau of Labor Statistics.

The story is even starker when we look at prices for basic necessities like food and energy. These prices have been climbing about twice as fast as overall inflation and around three times as fast as average hourly earnings. The toll of this type of inflation falls on everyone, but it does not fall uniformly. It lands hardest on families with low and moderate incomes, who spend, on average, about 75 to 80% of their budgets on necessities, compared to 65% for high-income families (see Council of Economic Advisors and Office of Management and Budget 2021). Inflation also tends to erode the value of fixed-income assets, which are held relatively more by older and less wealthy citizens (see Diwan, Duzhak, and Mertens 2021 and Board of Governors 2022c).

This corroding of real wages is more than just painful. It also undermines the basic American promise, which says that if you work hard, you can get ahead. Inflation traps people in an endless loop of running fast and falling behind, unrelated to effort or input.

Eventually, this sense of falling behind starts to affect decisionmaking.

Distortions and decisions

As people struggle to keep up with rising prices, earning money becomes the central factor in determining which jobs they choose.

Now, in some ways this seems fine. We work so we can buy things—to support ourselves, take care of our families, and give back to our communities. But when wages dominate all other considerations, like the type of job we do or the chance for future mobility, they become a wedge—putting space between what people need today and what they want for their future.

Workers everywhere are facing these choices. I recently heard an example at a gathering of local business leaders. One of them was from a large restaurant group with locations in multiple cities. It offered competitive salaries, health benefits, and lots of opportunities for professional growth. But longtime employees who had been advancing through the ranks and building careers with the organization were suddenly leaving. When the owner asked them why, he learned they were no longer able to afford rent near the city and had to move much farther away. Then gas prices started to rise and commuting so far became unsustainable. So many of them left to take lower-paying fast-food jobs nearer to where they lived. These jobs had fewer benefits and little opportunity for upward mobility. But what choice did they have? They had to manage their short-term budget pressures, even when it meant giving up jobs with brighter long-term prospects.

The effect of these choices, multiplied across large numbers of workers, has an impact on firms. Businesses are experiencing considerable churn in their employee base, often losing workers as fast as they can train them (see the BLS JOLTS report). Their response is predictable: raise wages as much as possible to try and retain staff; divide jobs into simpler tasks that require less training; and accelerate the search for ways to automate or outsource in order to reduce future worker demand. In the meantime, produce less and expand more slowly.

Unfortunately, the distortions from high inflation don’t stop there. They also influence longer-term decisionmaking in a way that lingers well after inflation has come down. One of the clearest examples of this long-term impact can be seen in trends in postsecondary schooling. Enrollments in two- and four-year colleges, certification programs, and technical training are all falling (see National Student Clearinghouse Research Center 2022). This is happening for many reasons, but two key factors are affordability and opportunity cost. Postsecondary education is already expensive. But it is even more costly when people have to give up earnings and still pay more for gas, food, and rent. And when firms are avidly bidding up wages to compete for workers, the equation just doesn’t add up. And so young people are taking jobs and delaying or opting out of school, as they have done in past tight labor markets (see Aaronson et al. 2019, Blom, Cadena, and Keys 2021, Dellas and Koubi 2003, and Dellas and Sakellaris 2003).

And here again, these individual choices bubble up to firms. Their strategic decisions about where to locate, expand, and invest are shaped by the projected availability of workers, especially skilled ones. As they plan for their future, declining school enrollments will factor into all of these decisions.

In other words, persistently high inflation is painful and it’s disruptive. It seeps into everything, including investment, production, and growth. Over time, it accumulates into a mountain of misallocations and lost opportunities. And it adds up to a smaller economic pie for all.

And this is why price stability is so crucial. It allows households and businesses to make decisions based on preferences, ideas, drive, and talent and lays the foundation for sustainable growth and durable expansion now and in the future. Price stability is like an asset that pays dividends year after year. And protecting it supports everyone.

Returning to 2%

But when you have been far away from something for a while, it can seem hard to find your way back. And this is the concern that many have about inflation. People worry that something has been lost, and the only way to regain it is to induce a painful recession like the ones we saw in the 1980s (see Goodfriend and King 2005).

But the circumstances back then were different. Policymakers had two major problems. One was that inflation was high and rising. Another was that inflation had been elevated for more than a decade and had seeped into the psychology of American consumers and businesses. Everyone expected high inflation to continue. So as inflation went up, longer-term inflation expectations went up with it (see Daly 2022 and Erceg and Levin 2003). The Fed had no choice but to “rip the Band-Aid” off and dramatically slow the economy in order to reset inflation psychology.

Today, we are in a better place. Of course, inflation has been too high for too long, coming in above target for more than a year. But inflation expectations, especially at the longer end, have remained stable and well anchored around the Fed’s 2% inflation goal. This means that, so far, inflation psychology has not been lost and the public continues to believe the Fed has the tools and the resolve to restore price stability (see, for example, Armantier et al. 2022).

But we cannot take this for granted. The longer inflation remains high, the more likely it is to change people’s expectations and undermine confidence (see Malmendier and Nagel 2016, Jordà et al. 2022, and Lansing 2022). And that is a problem we must avoid.

The question, of course, is how?

Navigating the economy toward a more sustainable path necessitates higher interest rates and a downshift in the pace of economic activity and the labor market. But for now, inducing a deep recession does not seem warranted by conditions, nor is it necessary to achieve our goals.

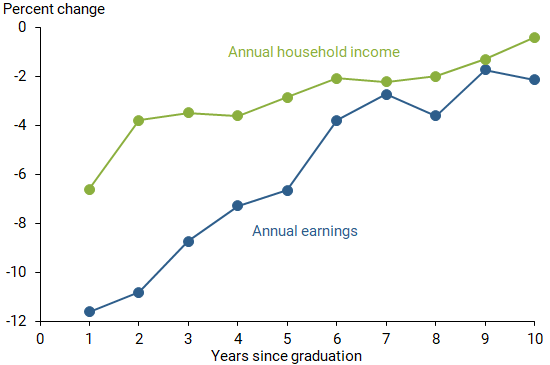

And this is crucial. Decades of research show the heavy toll that deep recessions take on people and families (see, for example, Okun 1973, Hassan and Mertens 2017, and Krueger, Mitman, and Perri 2016). Whole generations of workers feel lasting effects. The impact is striking (see Figure 2). People who enter the labor market during a recession come in on lower rungs of the career ladder and earn wages well below their peers who enter during expansions (see for example, von Wachter 2012, Altonji, Kahn, and Speer 2016, Schwandt and von Wachter 2019, Kahn 2010, and Oreopoulos, von Wachter, and Heisz 2012). Everyone is affected; college graduates, non-college graduates, all genders and races. But those historically less advantaged, including those with less than a high school education and people of color, are especially hard hit (see Duzhak 2021 and Hoynes, Miller, and Schaller 2012). And these effects are not short-lived. They persist throughout an individual’s career. The more severe the recession, the greater the potential harm.

Figure 2

Changes in annual earnings and income

Note: Drop in earnings for students graduating in a downturn relative to an expansion.

Source: Schwandt and von Wachter (2019) and FRBSF staff calculations.

Avoiding this kind of harsh recession will not be easy, but we must try.

And we’ve done it before. The expansion that started in the 1990s is a notable example (see Blinder 2022). After the Fed tightened policy to keep prices stable, growth slowed but no recession ensued. And a decade of sustained growth followed.

No doubt, the job will be harder this time. We are facing a myriad of risks. Ongoing battles with COVID globally, the war in Ukraine, and impending recession in Europe, all while central banks across the globe are tightening monetary policy to combat high and rising prices (see Obstfeld 2022). These risks, combined with stubbornly persistent supply chain issues, ongoing strength in the labor market, and robust consumer spending, narrow the path for a smooth landing. But they do not close it (see Bauer and Mertens 2022 and Bok et al. 2022).

Resolute to our goals, the Fed has raised the benchmark interest rate rapidly this year, and projects additional increases will be needed (see Board of Governors 2022b). These are necessary and appropriate adjustments, taken to put the economy back on a solid footing.

We are already starting to see the effects—housing markets are cooling, the labor market is easing, and projections of future growth are softening. Of course, the full impact of our policies will unfold over time, given likely lags in the effects of monetary policy (see, for example, Greenspan 2004 and Barnichon and Matthes 2018). So, we will need to remain attentive to the data, and recognize the signs that enough has been done or more is needed. History tells us that the costs of errors are high. Too little could allow inflation expectations to drift, requiring even more difficult policy actions in the future. And too much could end in overtightening and an unnecessary and painful downturn. Successful policy will require vigorous analysis, extreme data dependence, and a resolute commitment to delivering on our mandate.

Two mandates, one goal

The enduring lesson of my childhood is that people need both jobs and stable prices. That is why the dual mandate is not a choice between two desirable things. It is a balance meant to deliver on a singular goal—a sustainable and expanding economy that works for everyone.

That is the foundation of economic security. And that is what the Federal Reserve is working to achieve.

Thank you.

Mary C. Daly is president and chief executive officer of the Federal Reserve Bank of San Francisco.

References

Aaronson, Stephanie R., Mary C. Daly, William Wascher, David W. Wilcox. 2019. “Okun Revisited: Who Benefits Most from a Strong Economy?” Brookings Papers on Economic Activity (Spring), pp. 333-404.

Altonji, Joseph G., Lisa B. Kahn, and Jamin D. Speer. 2016. “Cashier or Consultant? Entry Labor Market Conditions, Field of Study, and Career Success.” Journal of Labor Economics 34(S1), pp. S361-S401.

Armantier, Olivier, Argia Sbordone, Giorgio Topa, Wilbert Van der Klaauw, and John C. Williams. 2022. “A New Approach to Assess Inflation Expectations Anchoring Using Strategic Surveys.” Journal of Monetary Economics 129(S), pp. S82-S101.

Barnichon, Regis, and Christian Matthes. 2018. “Functional Approximation of Impulse Responses.” Journal of Monetary Economics 99, pp. 41-55.

Bauer, Michael D., and Thomas M. Mertens. 2022. “Current Recession Risk According to the Yield Curve.” FRBSF Economic Letter 2022-11 (May 9).

Blinder, Alan. 2022. “Landings Hard and Soft: The Fed, 1965–2020.” Slides from presentation to Markus’ Academy, Bendheim Center for Finance, Princeton University, Princeton, NJ, February 11.

Blom, Erica, Brian C. Cadena, and Benjamin J. Keys. 2021. “Investment over the Business Cycle: Insights from College Major Choice.” Journal of Labor Economics 39(4) pp. 1,043-1,082.

Board of Governors of the Federal Reserve System. 2022a. “Statement on Longer-Run Goals and Monetary Policy Strategy.” Adopted effective January 24, 2012; as reaffirmed January 25, 2022.

Board of Governors, 2022b. “FOMC Projections materials, accessible version.” September 21.

Board of Governors, 2022c. “Distributional Financial Accounts (DFAs).”

Bok, Brandyn, Nicolas Petrosky-Nadeau, Robert G. Valletta, and Mary Yilma. 2022. “Finding a Soft Landing along the Beveridge Curve.” FRBSF Economic Letter 2022-24 (August 29).

Council of Economic Advisors and Office of Management and Budget. 2021. “The Cost of Living in America: Helping Families Move Ahead.” Report, August 11.

Daly, Mary C. 2022. “This Time Is Different… Because We Are.” FRBSF Economic Letter 2022-05 (February 28).

Dellas, Harris, and Vally Koubi. 2003. “Business Cycles and Schooling.” European Journal of Political Economy 19(4), pp. 843-859.

Dellas, Harris, and Plutarchos Sakellaris. 2003. “On the Cyclicality of Schooling: Theory and Evidence.” Oxford Economic Papers 55(1), pp. 148-172.

Diwan, Renuka, Evgeniya A. Duzhak, and Thomas M. Mertens. 2021 “Effects of Asset Valuations on U.S. Wealth Distribution.” FRBSF Economic Letter 2021-24 (August 30).

Duzhak, Evgeniya A. 2021. “How Do Business Cycles Affect Worker Groups Differently?” FRBSF Economic Letter 2021-25 (September 7).

Erceg, Christopher J., and Andrew T. Levin. 2003. “Imperfect Credibility and Inflation Persistence.” Journal of Monetary Economics 50(4), pp. 915-944.

Goodfriend, Marvin, and Robert G. King. 2005. “The Incredible Volcker Disinflation.” Journal of Monetary Economics 52(5), pp. 981-1,015.

Greenspan, Alan. 2004. “Risk and Uncertainty in Monetary Policy.” American Economic Review 94(2), pp. 33-40.

Hassan, Tarek A., and Thomas M. Mertens. 2017. “The Social Cost of Near-Rational Investment.” American Economic Review 107(4), pp. 1,059-1,103.

Hoynes, Hilary, Douglas L. Miller, and Jessamyn Schaller. 2012. “Who Suffers during Recessions?” Journal of Economic Perspectives 26(3), pp. 27-48.

Jordà, Òscar, Celeste Liu, Fernanda Nechio, and Fabián Rivera-Reyes. 2022. “Wage Growth When Inflation Is High.” FRBSF Economic Letter 2022-25 (September 6).

Kahn, Lisa B. 2010. “The Long-Term Labor Market Consequences of Graduating from College in a Bad Economy.” Labour Economics 17(2), pp. 303-316.

Krueger, Dirk, Kurt Mitman, and Fabrizio Perri. 2016. “On the Distribution of the Welfare Losses of Large Recessions.” NBER Working Paper 22458, July.

Lansing, Kevin J. 2022. “Untangling Persistent Versus Transitory Shocks to Inflation.” FRBSF Economic Letter 2022-13 (May 23).

Malmendier, Ulrike, and Stefan Nagel. 2016. “Learning from Inflation Experiences.” Quarterly Journal of Economics 131(1), pp. 53-87.

National Student Clearinghouse Research Center. 2022. “Term Enrollment Estimates, Spring 2022.”

Obstfeld, Maurice. 2022. “Uncoordinated Monetary Policies Risk a Historic Global Slowdown.” Realtime Economics Issues Watch, Peterson Institute for International Economics blog, September 12.

Okun, Arthur M., William Fellner, and Alan Greenspan. 1973. “Upward Mobility in a High-Pressure Economy.” Brookings Papers on Economic Activity 1973(1), pp. 207-261.

Oreopoulos, Philip, Till von Wachter, and Andrew Heisz. 2012. “The Short- and Long-Term Career Effects of Graduating in a Recession.” American Economic Journal: Applied Economics 4(1), pp. 1-29.

Schwandt, Hannes, and Till von Wachter. 2019. “Unlucky Cohorts: Estimating the Long-Term Effects of Entering the Labor Market in a Recession in Large Cross-Sectional Data Sets.” Journal of Labor Economics 37(S1), pp. S161-S198.

von Wachter, Till. 2012. “Job Displacements in Recessions: An Overview of Long-Term Consequences and Policy Options.” Chapter 2 in Reconnecting to Work: Policies to Mitigate Long-Term Unemployment and Its Consequences, editor Lauren D. Appelbaum. Kalamazoo, MI: W. E. Upjohn Institute for Employment Research, pp. 17-36.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org