Restoring price stability is a key part of the Fed’s mandate, and it is what the American people expect. Achieving it will take time and a broad view of economic conditions. Policymakers have to respond to an economy that is evolving in real time and prepare for what the economy will look like in the future. The following is adapted from remarks by the president of the Federal Reserve Bank of San Francisco to Griswold Center for Economic Policy Studies at Princeton University on March 4.

The most frequent question I am asked these days is, “What will the Fed do next?”

I understand. People are worried. Inflation is high and the Federal Open Market Committee (FOMC) has taken aggressive policy action to bring it down. The responses to our actions range from fearing they will tip the economy into a recession to fearing they won’t be sufficient to get the job done.

For most, this adds up to a lot of uncertainty. And the impulse to look for answers in the immediate. The next meeting. The next data release. The next market update. It doesn’t help that we face a round-the-clock ticker tape of economic and financial news.

But achieving our mandated goals takes time and a broader view. As policymakers, we have to respond to an economy that is evolving in real time and prepare for what the economy will look like in the future.

So today, I am going to do just that. I will pull back the lens from the immediate and talk about what the inflation landscape looked like before the pandemic, what it looks like now, and what both could mean for the future.

The world we had

To understand how future inflation could evolve, we must first remember where we were before the pandemic. So, let me start there.

Before the pandemic and the current episode of high inflation, the world was starkly different. The principal and decade-long challenge for the Federal Reserve and most other central banks was trying to bring inflation up to target, rather than pushing it down.

Large structural forces were to blame. The most notable was population aging, which was affecting the labor force and savings rates in industrialized and developing nations alike (United Nations 2022 and Jones 2022). Global productivity growth was also slowing, affecting demand for investment (Fernald et al. 2017 and Fernald and Li 2022). Together, these developments brought about weaker trend growth and lower real interest rates, and they put steady downward pressure on inflation (Carvalho, Ferrero, and Nechio 2017 and Jordà et al. 2019). Economics and policy discussions became focused on secular stagnation—a persistent state of little or no growth with economies running below potential (Summers 2014, Gordon 2015, Eggertsson, Mehrotra, and Summers 2016). Top of mind for policymakers were a low neutral rate of interest, the zero lower bound on interest rates, and the risks of consistently below target inflation (Bernanke 2012, Dudley 2013, Yellen 2013, Hills, Nakata, and Schmidt 2019, Mertens and Williams 2019, and Lansing 2021).

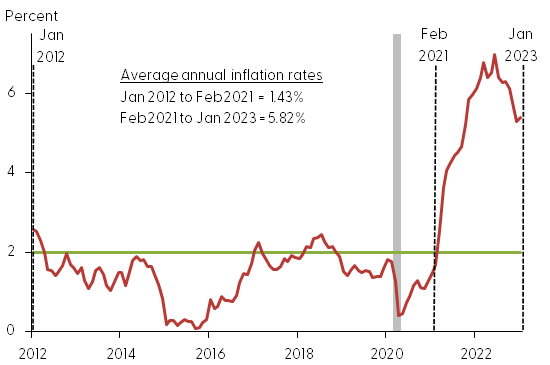

The inflation challenges in the United States were pronounced (Figure 1). Despite sustained monetary policy accommodation after the Great Recession, annual personal consumption expenditures (PCE) inflation remained below 2% for 84 out of 98 months (January 2012 through February 2020), or about 86% of the time. Over that same period, the federal funds rate was set near zero almost half of the time and below 2.5% (the current estimate of the neutral rate) for the entire time.

Figure 1

Headline PCE inflation, January 2012 to January 2023

Source: Bureau of Economic Analysis, FRBSF staff calculations; 12-month rate. Gray shading indicates NBER recession dates.

This environment ended up offering some advantages. The U.S. economy was able to run consistently above estimates of potential growth and unemployment was able to fall to near-historic levels without spurring inflation.

But it also came with risks. Namely, that inflation would fail to get to target in good times and fall further in bad ones. Eventually this would seep into expectations, reducing monetary policy space and compounding the existing structural downward pressures on inflation (Amano, Carter, and Leduc 2020 and Diwan, Leduc, and Mertens 2020). The persistent deflation in Japan underscored this challenge, and it motivated the Fed and many other central banks to fight vigorously to get inflation up to target. It also prompted a review of policy objectives and tools that could reliably deliver on this goal (Board of Governors 2020).

This was the seemingly unchangeable topography of the economy before the pandemic.

And then of course, everything changed.

The pandemic shock

We all know the story. When COVID-19 hit, the economy faltered. The Fed cut interest rates, purchased long-term assets, and opened lending facilities, all to help bridge the economy through the very worst. U.S. fiscal agents took equally aggressive action.

These efforts were unprecedented. And they worked, to an extent. U.S. economic growth rebounded, demand surged, and the labor market began to recover. Supply chains, however, were slow to respond. And by early 2021, price pressures were starting to build—first in a few sectors directly affected by the pandemic, and then more broadly, as imbalances between robust demand and limited supply spread throughout the economy. By the fall of 2021, inflation was high and heading higher.

The chart puts the change in inflation in perspective (Figure 1). After averaging about 1.4% per year in the low-inflation period, PCE inflation shot up to an average of 5.8% between February 2021 and today—that’s a quadrupling of average inflation. Said simply, within a year, inflation went from consistently undershooting our 2% target to reaching levels not seen in more than a generation.

In response, the Fed pivoted from a stance of sustained accommodation to one of rapid tightening, first through forward guidance and then through conventional increases in interest rates. Since March of last year, the FOMC has raised the federal funds rate at every meeting, by a cumulative total of 4½ percentage points. This is the fastest pace of monetary policy tightening in 40 years. Broader financial market conditions, which capture funds rate movements, along with FOMC forward guidance and the reduction in the Fed’s balance sheet, have tightened even more (Choi et al. 2022).

This tightening, while pronounced, was and remains appropriate given the magnitude and persistence of elevated inflation readings. Higher interest rates help bridle demand growth, bringing it back in line with supply (Shapiro 2022). This rebalancing helps reduce inflation pressures (Hazell et al. 2022 and Jørgensen and Lansing 2021, 2023).

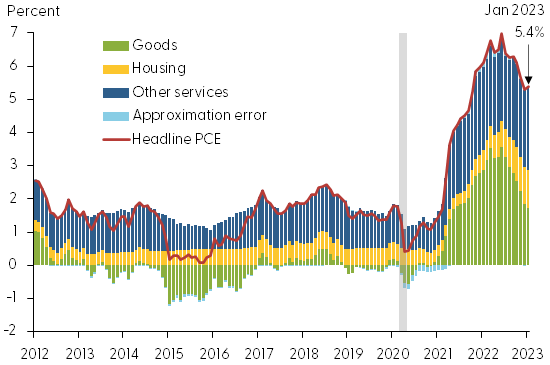

And this is what we are seeing (Figure 2). The economy has been gradually slowing and inflation has followed. Since June of 2022, overall inflation has been easing, falling from its highs of around 7% to its current reading of 5.4% in January.

Figure 2

Decomposition of headline PCE inflation (12-month rate)

Source: Bureau of Economic Analysis, FRBSF staff calculations. Gray shading indicates NBER recession dates.

This is good news, a sign that policy is doing its job and—along with improvements in supply—working to reduce the imbalances that have pushed inflation so high.

But the work is far from done. Overall inflation remains well above target and contributions from each of the components of inflation—goods, housing, and other services—remain well above their historical trend (Figure 2). Moreover, the incoming data have been bumpy. The recent PCE reading is a good example. After months of decline, headline and core inflation both ticked up in January on a 12-month basis, and the monthly inflation rate rose at its fastest pace in seven months. This suggests that the disinflation momentum we need is far from certain.

Putting all of this together, it’s clear there is more work to do. In order to put this episode of high inflation behind us, further policy tightening, maintained for a longer time, will likely be necessary.

But restoring price stability is our mandate and it is what the American people expect. So, the FOMC remains resolute in achieving this goal.

As we work toward that end, we must also consider the world we are entering. What will the pressures on inflation be once the pandemic shock has fully worn off? Will we return to a world where the central bank struggles to get inflation up to target? Or has the pandemic left a more permanent imprint, such that the pressures on inflation now trend higher and we have to work to keep them at bay?

The answers aren’t yet clear. But the questions are imperative. And we must begin to think about them.

An uncharted path

In doing that, let’s start with what we know. We know what forces drove the pre-pandemic inflation trend. And we know what forces are driving the ongoing pandemic-induced inflation surge. What we don’t know is how they will evolve and interact after the pandemic is gone, or what this new confluence will mean for underlying inflation.

So, let me offer four things that I think could be important for our future inflation path—four things that could counterbalance or even offset entirely the deflationary trend of the past.

One is a decline in global price competition. If firms decide to reshore some or all of their foreign production facilities, costs and prices are likely to continue to rise. My conversations with business leaders suggest that some of this is already happening. But it’s a major undertaking to completely revamp well-established production networks, and it remains to be seen how far this trend will go. One thing, however, is clear. Globalization has been a key driver of past goods deflation in the United States (Guerrieri, Gust, and López-Salido 2010). And a trend toward less global competition could mean more inflation in the goods sector and more pressure on overall inflation going forward.

Another potential factor affecting future inflation is the ongoing domestic labor shortage. Labor force participation fell precipitously during the pandemic and has been slow to recover, especially among workers 55 years and older. These developments exacerbate the already significant downward drag on participation related to population aging (Hornstein and Kudlyak 2019 and Montes, Smith, and Dajon 2022). Absent a substantial pickup in the share of working-age adults looking to be employed or a large change in immigration flows (Duzhak 2023), labor force participation will continue to decline and worker shortages will persist, pushing up wages and ultimately prices, at least in the near and medium term.

Inflation pressures could also move upward as firms make the transition to a greener economy, which will require investment in new processes and infrastructure. As firms increase their investments in renewable energy and energy-efficient technologies, they are likely to pass some portion of these transition costs on to consumers, boosting inflation. This increased demand for investment could raise the neutral rate of interest, at least in the short and medium term, lessening the importance of the zero lower bound and the downward pressures on inflation that came with it (Daly 2021). But conventional models of the long-run neutral rate of interest do not link it to factors such as the transition to a greener economy (Laubach and Williams 2003).

Finally—and this is at the forefront of my mind as a policymaker—is the possibility that inflation expectations could change. To date, these expectations—especially in the longer run—have remained stable and well anchored near the Fed’s 2% goal (Armantier et al. 2022). In other words, so far, inflation psychology has not shifted and public faith in the Fed’s ability to achieve its price stability mandate remains intact. But the longer inflation remains high, the more likely it is to undermine confidence. And once high inflation becomes embedded in public psychology, it is very hard to change.

Any or all of these factors could influence the natural tilt of inflation and the monetary policy approach necessary to maintain price stability over the long term.

The hard part, of course, is knowing when and how each of these factors will evolve or what force they will have relative to the strong pull coming from population aging and slow productivity growth. If those pre-pandemic trends reemerge as the dominant structural forces, then our efforts to bring inflation down will be reinforced by natural features of the economy. But if the old dynamics are eclipsed by other, newer influences and the pressures on inflation start pushing upward instead of downward, then policy will likely need to do more.

We don’t know what the trend will be. But we do know that, while we continue to diffuse the ongoing inflation shock, we need to be working to gather data and research that illuminates the likely path forward. That’s prudent policymaking. An eye on today, an eye on tomorrow.

The duality of policymaking

That discipline is not easy. When things are hard and you’re right in the middle of it, it’s tempting to get caught up in the present—today’s data release, the newest projection. So much so that we can forget to look forward, take stock, and imagine what the future could hold.

But policymaking requires it. The pandemic and its shockwaves will one day fully dissipate. And we must be ready.

So as I close today, I will return to the question I started with: What will the Fed do next?

My answer: We will work on the economy we have and prepare for the economy to come. That’s what this moment demands. Thank you.

Mary C. Daly

President and Chief Executive Officer, Federal Reserve Bank of San Francisco

References

Amano, Robert, Thomas J. Carter, and Sylvain Leduc. 2020. “Is the Risk of the Lower Bound Reducing Inflation?” FRBSF Economic Letter 2020-05 (February 24).

Armantier, Olivier, Argia Sbordone, Giorgio Topa, Wilbert Van der Klaauw, and John C. Williams. 2022. “A New Approach to Assess Inflation Expectations Anchoring Using Strategic Surveys.” Journal of Monetary Economics 129(S), pp. S82–S101.

Bernanke, Ben S. 2012. “Monetary Policy since the Onset of the Crisis.” Speech presented at the Federal Reserve Bank of Kansas City Economic Symposium, Jackson Hole, WY, August 31.

Board of Governors. 2020. “Federal Open Market Committee Announces Approval of Updates to its Statement on Longer-Run Goals and Monetary Policy Strategy.” Press release, August 27.

Board of Governors. 2020. “Federal Open Market Committee Announces Approval of Updates to its Statement on Longer-Run Goals and Monetary Policy Strategy.” Press release, August 27.

Carvalho, Carlos, Andrea Ferrero, and Fernanda Nechio. 2017. “Demographic Transition and Low U.S. Interest Rates.” FRBSF Economic Letter 2017-27 (September 25).

Choi, Jason, Taeyoung Doh, Andrew Foerster, and Zinnia Martinez. 2022. “Monetary Policy Stance Is Tighter than Federal Funds Rate.” FRBSF Economic Letter 2022-30 (November 7).

Daly, Mary C. 2021. “Climate Risk and the Fed: Preparing for an Uncertain Certainty.” FRBSF Economic Letter 2021-17 (June 28).

Diwan, Renuka, Sylvain Leduc, and Thomas M. Mertens. 2020. “Average-Inflation Targeting and the Effective Lower Bound.” FRBSF Economic Letter 2020-22 (August 10).

Dudley, WIlliam C. 2013. “Lessons at the Zero Bound: The Japanese and U.S. Experience.” Remarks at the Japan Society, New York, NY, May 21.

Duzhak, Evgeniya A. 2023. “The Role of Immigration in U.S. Labor Market Tightness.” FRBSF Economic Letter 2023-06 (February 27).

Eggertsson, Gauti B., Neil R. Mehrotra, and Lawrence H. Summers. 2016. “Secular Stagnation in the Open Economy.” American Economic Review: Papers and Proceedings 106(5), pp. 503–507.

Fernald, John, Robert Hall, James Stock, and Mark W. Watson. 2017. “The Disappointing Recovery of Output after 2009.” Brookings Papers on Economic Activity (Spring) pp. 1–54.

Fernald, John, and Huiyu Li. 2022. “The Impact of COVID on Productivity and Potential Output.” FRB San Francisco Working Paper 2022-19.

Gordon, Robert J. 2015. “Secular Stagnation: A Supply-Side View.” American Economic Review: Papers and Proceedings 105(5), pp. 54–59.

Guerrieri, Luca, Christopher Gust, and J. David López-Salido. 2010. “International Competition and Inflation: A New Keynesian Perspective.” American Economic Journal: Macroeconomics 2(4), pp. 247–280.

Hazell, Jonathan, Juan Herreño, Emi Nakamura, and Jón Steinsson. 2022. “The Slope of the Phillips Curve: Evidence from U.S. States.” Quarterly Journal of Economics 137, pp. 1,299–1,344.

Hills, Timothy S., Taisuke Nakata, and Sebastian Schmidt. 2019. “Effective Lower Bound Risk.” European Economic Review 120(103321).

Hornstein, Andreas, and Marianna Kudlyak. 2019. “Aggregate Labor Force Participation and Unemployment and Demographic Trends.” FRB San Francisco Working Paper 2019-07.

Jones, Charles I. 2022. “The End of Economic Growth? Unintended Consequences of a Declining Population.” American Economic Review 112(11), pp. 3,489–3,527.

Jordà, Òscar, Chitra Marti, Fernanda Nechio, and Eric Tallman. 2019. “Why Is Inflation Low Globally?” FRBSF Economic Letter 2019-19 (July 15).

Jørgensen, Peter Lihn and Kevin J. Lansing. 2021. “Return of the Original Phillips Curve.” FRBSF Economic Letter 2021-21 (August 9).

Jørgensen, Peter Lihn, and Kevin J. Lansing. 2023. “Anchored Inflation Expectations and the Slope of the Phillips Curve.” FRB San Francisco Working Paper 2019-27 (revised February 2023).

Lansing, Kevin J. 2021. “Endogenous Forecast Switching Near the Zero Lower Bound.” Journal of Monetary Economics 117(1), pp. 153–169.

Laubach, Thomas, and John C. Williams. 2003. “Measuring the Natural Rate of Interest.” Review of Economics and Statistics 85(4, November), pp. 1,063–1,070.

Mertens, Thomas M., and John C. Williams. 2019. “Monetary Policy Frameworks and the Effective Lower Bound on Interest Rates.” American Economic Review: Papers and Proceedings 109(May), pp. 427–432.

Montes, Joshua, Christopher Smith, and Juliana Dajon. 2022. “‘The Great Retirement Boom’: The Pandemic-Era Surge in Retirements and Implications for Future Labor Force Participation.” Federal Reserve Board of Governors, Finance and Economics Discussion Series 2022-081.

Shapiro, Adam Hale. 2022. “How Much Do Supply and Demand Drive Inflation?” FRBSF Economic Letter 2022-15 (June 21).

Summers, Lawrence H. 2014. “U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound.” Business Economics 49(2), pp. 65–73.

United Nations. 2022. World Population Prospects 2022: Summary of Results. Report, Department of Economic and Social Affairs, Population Division, New York, NY.

Yellen, Janet L. 2013. “Challenges Confronting Monetary Policy.” Speech presented at the 2013 National Association for Business Economics Policy Conference, Washington, DC, March 4.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org