Reuven Glick, group vice president at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of September 8, 2016.

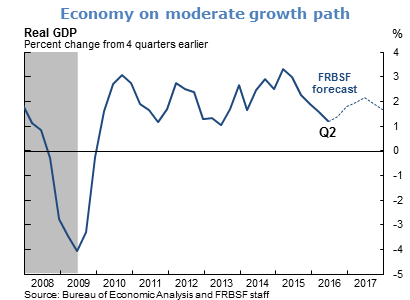

- GDP growth for the first half of this year has been weak. Real GDP growth was revised down to an annualized rate of 1.1% in the second quarter from an initial estimate of 1.2%, following 0.8% growth in the first quarter. Growth has been supported by healthy consumer spending, but dampened by weak business investment spending and by firms’ inventory drawdowns; the latter alone subtracted 1.3 percentage points from overall growth in the second quarter.

- We expect GDP growth to rebound to above 2% in the second half of 2016, as personal income grows, households continue to spend, and firms stop reducing their inventory stocks. We anticipate that the weakness in business investment will come to an end, as the lingering effects of earlier dollar appreciation and lower energy prices dissipate, though slow foreign growth will continue to pose a headwind. We expect GDP growth to be closer to trend in the 1-1/2% to 2% range in 2017.

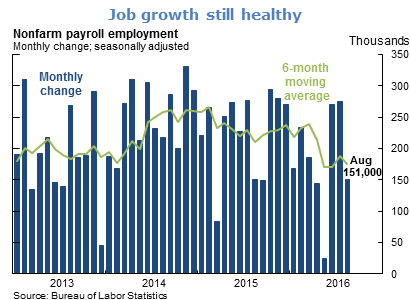

- Following very strong gains in June and July, nonfarm payroll employment in August rose by 151,000 jobs, less than private analysts’ expectations. Over the past six months, job gains have averaged 175,000 jobs per month. Though the August reading represents a slowdown from prior months, it is well above 60,000 to 100,000 new jobs per month, the estimated “break-even” range needed to absorb new entrants to the labor force.

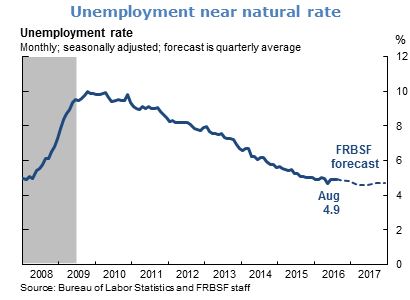

- The unemployment rate stayed unchanged in August at 4.9%, close to our estimate of the natural rate of unemployment of 5%. We anticipate that modestly above-trend GDP growth will push the unemployment rate down a bit further over the next year.

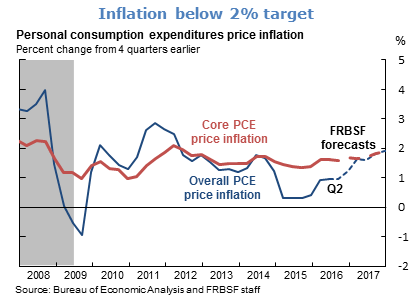

- Inflation continues to run below the Federal Reserve’s 2% target. Overall inflation, as measured by the change in the personal consumption expenditures (PCE) price index, was 0.8% in the 12 months through July. Very low overall inflation is largely attributable to lower energy prices and the strengthening of the dollar. Core inflation, which strips out movements in energy and food prices, rose 1.6% over the past 12 months. Average hourly earnings grew slightly in July, bringing the 12-month increase in wages to 2.4%. We expect that diminishing slack as well as the fading effects of the dollar’s appreciation and declining energy prices will push core and overall PCE inflation up gradually towards 2%.

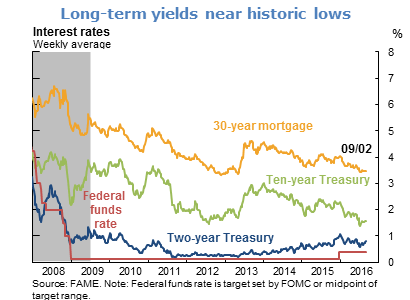

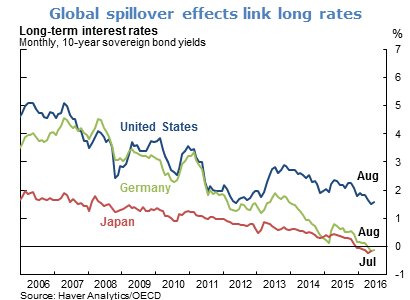

- Since the Federal Reserve raised its funds rate target range in December 2015, longer-term U.S. Treasury yields have fallen to near historic lows. The decline in rates reflects a combination of long-term and short-term factors.

- Over the long term, slower trend productivity and output growth in the United States and other advanced economies have reduced demand for investment. Aging populations and shrinking labor forces have also put downward pressure on output and depressed investment demand. In addition, the so-called “global saving glut” in many emerging market economies has added to the supply of funds in financial markets. More saving and less investment have pushed down equilibrium interest rates.

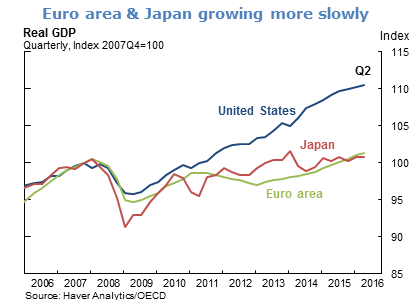

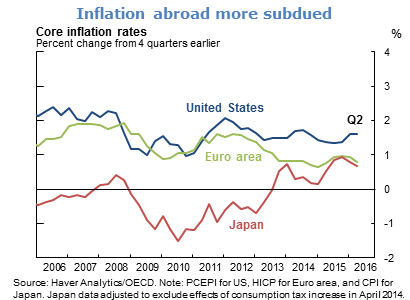

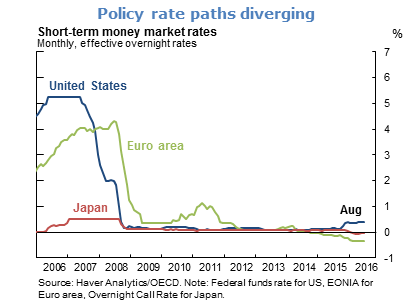

- In the short term, heightened global uncertainty has increased demand for safe-haven assets, such as U.S. Treasuries. In addition, expansionary monetary policies in advanced countries have had cross-country spillover effects on interest rates. In recent years, the spillover effects have been quite strong because of divergent economic conditions and monetary policy paths in the United States and other advanced economies. In particular, output growth in other advanced economies, such as the Euro area and Japan, has been relatively stagnant since the global financial crisis. Foreign inflation has also been subdued in comparison with the United States. These differences in economic performance have resulted in diverging monetary policy stances. The United States has begun to normalize its monetary policy and is expected to tighten it more in the future. In contrast, the European Central Bank and the Bank of Japan have eased monetary policy further—through more negative rates on reserve deposits and greater quantitative easing—and both central banks are expected to stay very accommodative in the near term. This divergence in policy paths has increased demand for U.S. assets by foreign investors seeking higher returns, and further pushed U.S. long-term interest rates down.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.