John Fernald, senior research advisor at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of January 12, 2017.

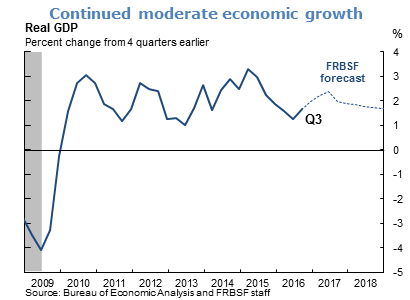

- Recent data confirm that the economy has picked up from its modest pace of the first half of 2016. Indeed, in the third quarter of 2016 GDP growth was revised up from an annualized rate of 3.2% to 3.5%. This rapid pace in part reflected transitory factors such as inventory accumulation and agricultural exports. Going forward, GDP growth is likely to remain for some time a bit above its long-run trend of 1½% to 1¾%. The fundamentals of consumer spending remain healthy, including solid income growth and strong household balance sheets. And business capital spending is poised to rebound from its weak pace of the past several years.

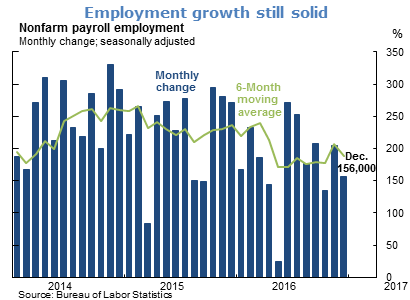

- Employment gains remain solid. Nonfarm payroll employment rose by 156,000 jobs in December. Unusually cold weather in many parts of the country appear to have held down those job gains somewhat. However, even without controlling for weather, the pace of gains remains well above the “breakeven” level needed to absorb new entrants to the labor force, which we estimate at roughly 80,000 new jobs on average per month.

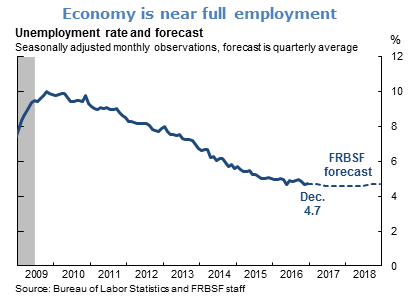

- The labor market remains near its sustainable, full employment level. The unemployment rate in December ticked up to 4.7%, a touch below our estimate of the natural rate of unemployment of 5%. The December unemployment rate was the lowest end-of-year rate since 2006.

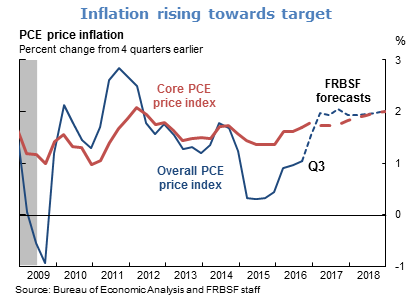

- Inflation remains below the Federal Reserve’s 2% objective, but has been gradually increasing towards the target rate since early 2016. Overall consumer prices, as measured by the price index for personal consumer expenditures, were 1.4% higher in November than a year earlier. Core consumer prices, which strip out volatile movements in energy and food prices, were 1.6% higher. With a tight labor market and the waning effects of past energy price declines, we expect overall and core consumer price inflation to run just a shade below 2% this year.

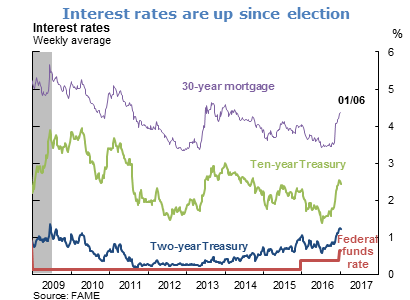

- Interest rates have risen sharply since the election in early November. In addition, the Federal Open Market Committee as widely expected raised its target for the federal funds rate at its December meeting. At the post-meeting press conference, Federal Reserve Chair Yellen noted that the decision to raise the fed funds target was “a reflection of the confidence we have in the progress the economy has made and our judgment that progress will continue.”

- There is considerable uncertainty about the scope of policy changes that might be implemented under the incoming administration and about their effects on the Federal Reserve’s dual-mandate objectives of maximum employment and price stability. Of particular focus are possible changes in Federal tax and spending policy.

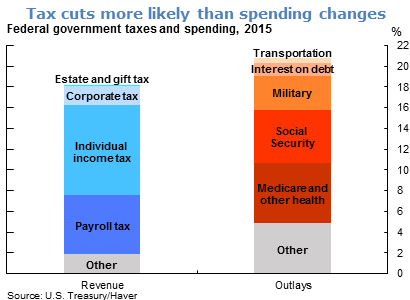

- Federal revenues fell short of federal outlays in 2015, leaving a deficit of about 2½% of GDP. There are conflicting political pressures that could influence the path of future government spending. On the one hand, there is some desire to restrain spending in order to keep the budget deficit down. On the other hand, there is some desire to increase military and infrastructure spending, while an aging population will put upward pressure on Social Security and Medicare spending.

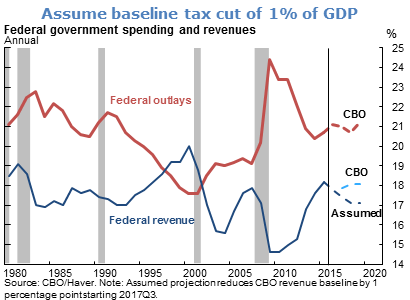

- Federal spending as a share of GDP typically goes up in recessions and stabilizes or falls in expansions. That was particularly true in the past decade. The Great Recession of 2007-09 lowered GDP deeply, and, to help cushion the downturn, the government increased spending under the 2009 American Recovery and Reinvestment Act. Since 2010, the spending share has fallen as the economy has grown and the temporary stimulus package ended. In addition, budget caps implemented in 2011 have constrained spending. Given the competing political pressures, our forecast assumes that the path of overall federal spending remains unchanged although there may be shifts in composition.

- Federal revenue as a share of GDP typically goes down in recessions and rises in expansions. For example, with a progressive tax system, the average tax rate falls when income falls. As with spending, this pattern was especially pronounced in the Great Recession. Revenues as a share of GDP are currently close to their average levels over the past few decades. Our forecast assumes that there will be reductions in individual and corporate taxes amounting to about 1 percent of GDP.

- All else equal, tax cuts boost household and business income. Although the details of the tax cut matter, a plausible estimate is that desired spending may rise by perhaps 0.6 percent of GDP. (Households and businesses will try to save the rest.) However, because the economy already is near full employment, this increase in desired spending likely will be dampened somewhat by higher interest rates and a stronger dollar. On balance, we expect that tax cuts will raise the level of GDP by a total of about 0.4%. Since it is likely to take time for the legislation to be passed and for the increase in spending to occur, we expect that tax changes will boost our growth forecast by 0.1% to 0.2% for the next few years.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.