Kevin J. Lansing, research advisor at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of August 9, 2018.

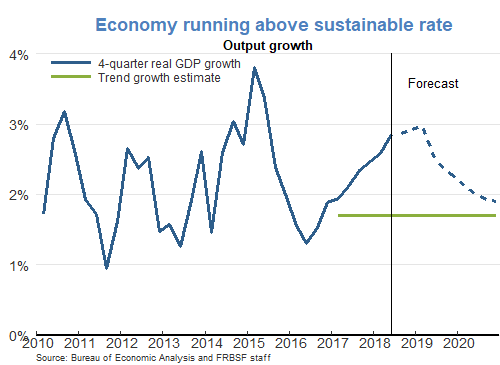

- The initial estimate of real GDP growth in the second quarter of 2018 came in at 4.1% at an annual rate, resulting in a growth rate of 2.8% over the past four quarters. For 2018 as a whole, we expect growth to come in just under 3%, well above our estimate of the economy’s long-run sustainable growth rate. Given the diminishing effects of federal fiscal stimulus over the next few years and the expected tightening of financial conditions, we project that growth will slow to just under 2% by 2020.

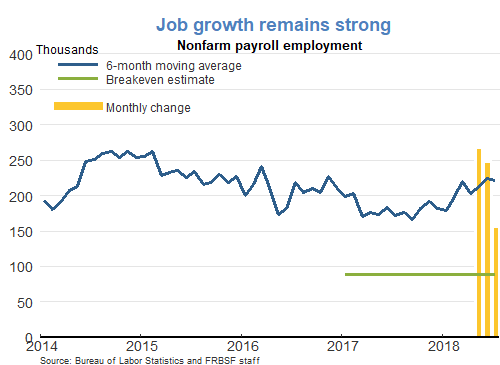

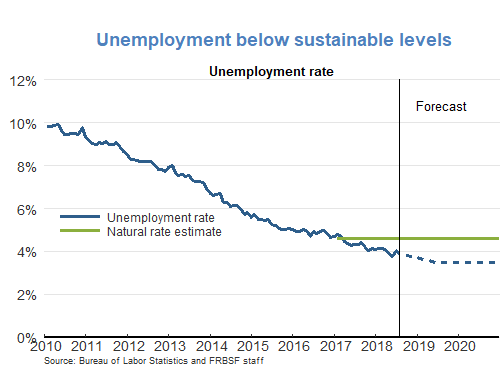

- The Bureau of Labor Statistics reported that payroll employment increased by 157,000 jobs in July. Data for the previous two months were revised upward, resulting in an average job gain over the past three months of 224,000. Over the past year, the average monthly gain was 203,000 jobs. The unemployment rate edged down to 3.9% from 4% in June. We expect monthly job gains to remain above the breakeven level needed to keep pace with the growth rate of the labor force. Consequently, we expect the unemployment rate to decline further below our 4.6% estimate of the natural rate of unemployment.

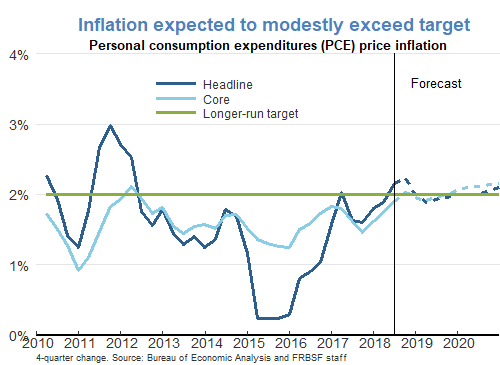

- Inflation over the past year is close to the Federal Open Market Committee’s (FOMC’s) 2% target. With unemployment below the natural rate and real GDP growth above its long-run sustainable pace, we expect some upward pressure on inflation over the medium term, causing the four-quarter inflation rate to slightly overshoot the 2% target in 2020.

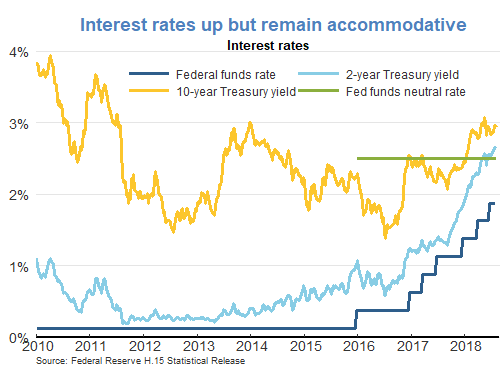

- Following the conclusion of its latest meeting on August 1, the FOMC announced its decision to maintain the target range for the federal funds rate at 1¾ to 2%. The Committee noted that recent economic activity has been strong and that risks to the economic outlook appear roughly balanced. The Committee expects further gradual increases in the target range for the federal funds rate.

- Interest rates have continued to increase with the ongoing monetary policy normalization. Nevertheless, the current level of the federal funds rate remains accommodative as it stands about 50 basis points below our estimate of the “neutral” federal funds rate.

- Few, if any, past recessions have been successfully predicted either by the Federal Reserve or professional forecasters. Forecasting recessions is difficult because each one tends to differ in important ways from previous episodes. Past recessions have been triggered by upward spiking oil prices, increases in policy interest rates designed to bring down high inflation, and bursting asset price bubbles.

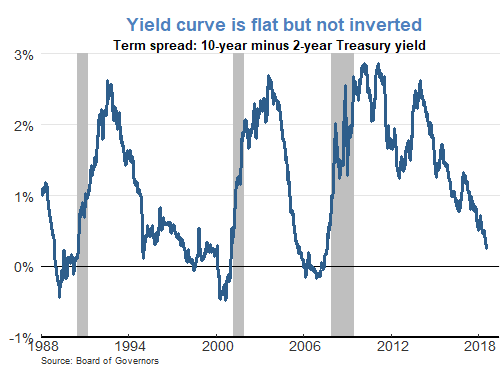

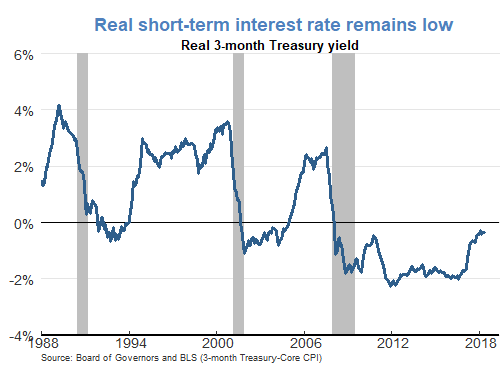

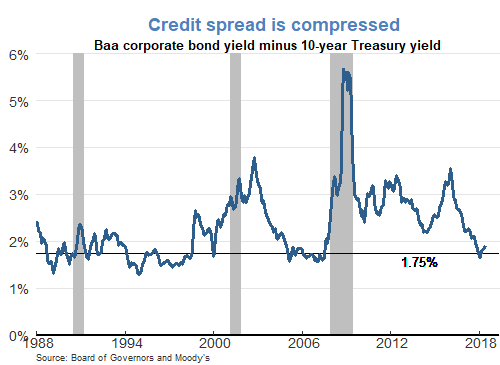

- Despite the varied triggers, recessions are typically preceded by some characteristic interest rate configurations. These include an inverted Treasury yield curve, an elevated real short-term interest rate, and a compressed credit spread (as measured by the yield difference between Baa corporate bonds and 10-year Treasury bonds).

- An inverted yield curve is often observed after a sustained series of monetary policy tightening actions that serve to raise real short-term Treasury yields. Long-term Treasury yields, which reflect expectations of future economic conditions, tend to move up with short-term yields during the early phases of an economic expansion, but may stop doing so (resulting in a flat or inverted yield curve) if investors’ economic outlook becomes more pessimistic.

- Corporate bond yields are typically higher than Treasury bond yields because corporate yields must compensate investors for the risk of default. During an economic expansion, default risk declines which causes the credit spread to compress. But a sustained expansion may cause investors to underestimate the risk of default, contributing to weak lending standards, excessive borrowing, and a credit spread that is too low. The onset of an economic slowdown or a recession would trigger the unwinding of such conditions. Research shows that optimistic credit market sentiment, as measured in part by a compressed credit spread, tends to predict slower economic activity at a two-year horizon.

- The current interest rate configuration can be described as follows: (1) The Treasury yield curve is relatively flat but not inverted, (2) the real short-term interest rate has been increasing but is still low by historical standards, and (3) the credit spread is compressed. This configuration can be described as providing mixed signals about the future. While the first two observations suggest that the risk of a recession remains relatively low, factoring in the third observation would suggest a somewhat higher risk of a recession than otherwise.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.