Vasco Curdia, research advisor at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of January 11, 2018.

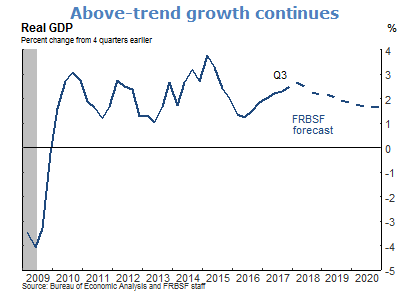

- Real GDP grew at an annual rate of 3.2% in the third quarter, according to the final estimate of the Bureau of Economic Analysis. We forecast that GDP growth averaged 2.5% for 2017. The momentum in GDP growth reflects strong gains in personal income and consumer confidence, supported by continued strength in the labor and financial markets. As monetary policy continues to normalize over the next two to three years, we expect growth to gradually fall back to our trend growth estimate of about 1.7%.

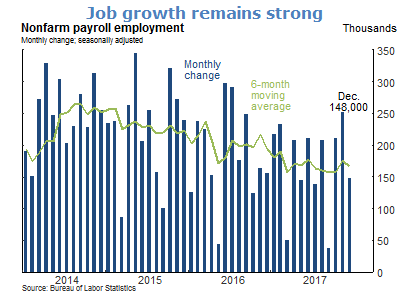

- We continue to see strengthening in labor market conditions. Nonfarm payroll employment increased by 148,000 jobs in December, a bit below expectations. Over the past six months, job gains have averaged close to 166,000, well above the amount needed to absorb the flow of new workers into the labor force.

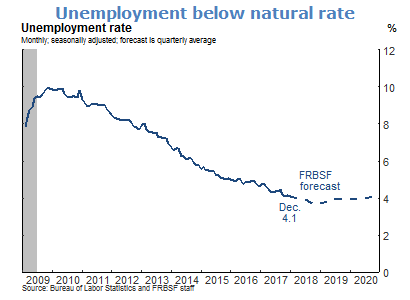

- The unemployment rate was unchanged in December from its November value of 4.1%. We expect the rate to fall below 4.0% in 2018 as the economy continues to strengthen. With the gradual removal of monetary policy accommodation, we expect the unemployment rate to return gradually to our estimate of the natural rate of unemployment of 4¾%.

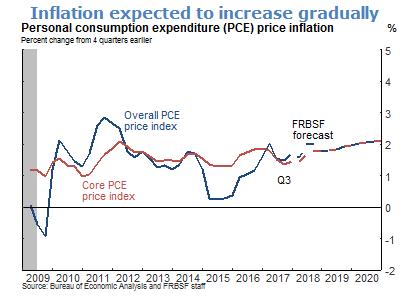

- Inflation remains below the FOMC’s target of 2%. In November, the personal consumption expenditure (PCE) price index rose 1.8% over the past 12 months, and the core PCE price index, which removes volatile food and energy prices, rose 1.5%. Transitory developments for a few categories of goods and services held down inflation in 2017. As these developments loosen their hold, we expect continued tightness in the labor market will push inflation up in the coming year.

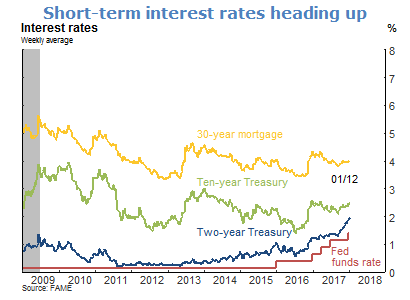

- At the December meeting, the FOMC raised the target range for the federal funds rate by a quarter to 1.25% to 1.50%. Short-term rates followed suit, while longer-term yields did not respond as much to the FOMC announcement.

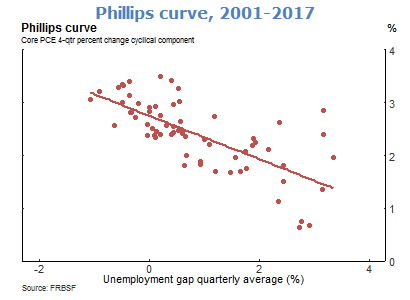

- The relationship between economic slack and inflation is often referred to as the Phillips curve. The theory behind this relationship maintains that conditions that push the economy beyond full employment lead to increased cost pressures on firms and capacity constraints. Cost pressures lead to higher wages and labor costs, while capacity constraints and strained supply chains in the face of high demand push up intermediate costs. In response to these higher costs, firms tend to increase the prices they charge for their goods and services, leading to price inflation.

- Various factors can influence cost pressures independently of economic strength. For example, labor market frictions, such as changes in bargaining power, labor force participation, or long-term unemployment can push up the natural rate of unemployment. Oil prices, the strength of the US dollar, or import prices can similarly affect cost pressures in the economy.

- Inflation expectations also can affect the transmission from cost pressures to price inflation. For example, high inflation expectations in the early 1980s contributed to elevated price inflation for some time, despite high unemployment. If individual firms expect economy-wide prices to increase at a fast pace, they will be reluctant to slow their own price increases. If many firms follow the same reasoning and expect other firms to keep raising prices, then overall inflation will remain strong. Similarly, strategic industry-specific considerations may affect price inflation. For example, recent price wars in the telecommunications sector have led to weaker inflation numbers.

- Staff statistical analysis finds a negative relationship between the unemployment gap and the cyclical component of inflation (excluding components that are not sensitive to business cycle conditions) over the period 2001 to 2017, consistent with economic theory. Currently, the economy is beyond full employment and thus, based on the Phillips curve, we are likely to see an increase in cyclical inflation, in turn pushing up overall price inflation.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.