Galina Hale, research advisor at the Federal Reserve Bank of San Francisco, stated her views on the current economy and the outlook as of January 10, 2019.

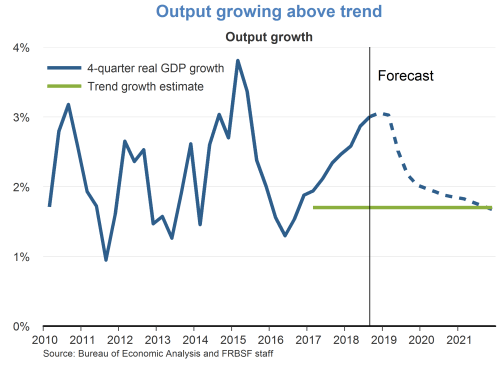

- The economy has continued to grow at a robust pace, primarily driven by solid gains in consumer income and spending. We project that GDP growth rate averaged 3.1% for 2018. We forecast that growth will slow down to 2.0% in 2019, as monetary policy continues to normalize and fiscal stimulus wanes, and fall gradually to our estimated long-term potential rate of 1.7%.

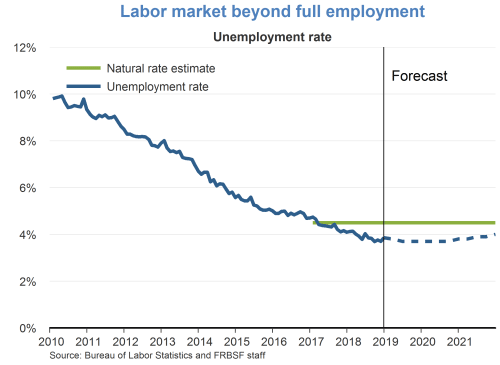

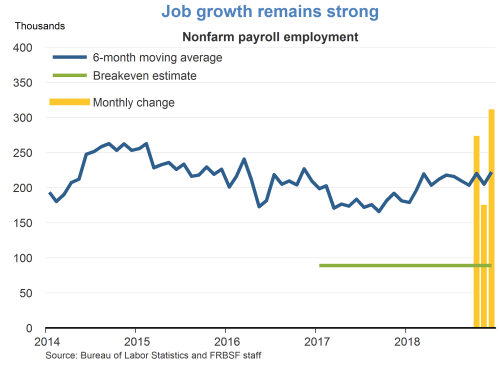

- The labor market remains very strong. The economy added 312,000 jobs in December, significantly exceeding the breakeven rate, which we estimate at about 90,000 jobs per month. The increases in payroll numbers were revised up for both October and November to 274,000 jobs and 176,000 jobs, respectively. Though the December unemployment rate rose 0.2 percentage point to 3.9%, this mainly reflects a sharp increase in the number of people entering the labor force, and it remains well below our estimate of the natural unemployment rate of 4.5%. We expect unemployment to decline to 3.7% by the end of 2019, and then gradually climb to 4.0% by the end of the forecast horizon.

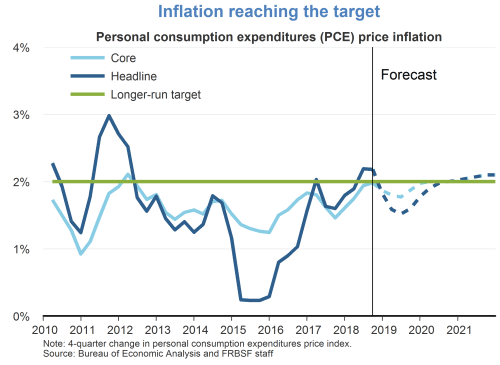

- Headline inflation of the personal consumer expenditures (PCE) price index over the past 12 months came in at 1.8% in November, slightly below the Federal Open Market Committee’s (FOMC) target of 2%. Core inflation, which excludes volatile food and energy prices, rose 1.9%. We forecast that inflation will remain at this level below target through 2019. The recent softening in inflation is partially attributable to the pass-through of low commodity prices and lower-than-expected increases in health-care costs. As the labor market continues to strengthen and the effects of these transitory factors diminish over time, we expect both headline and core inflation rates to slightly overshoot the 2% target by the end of 2020.

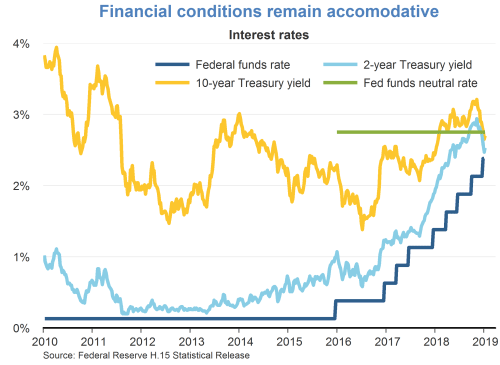

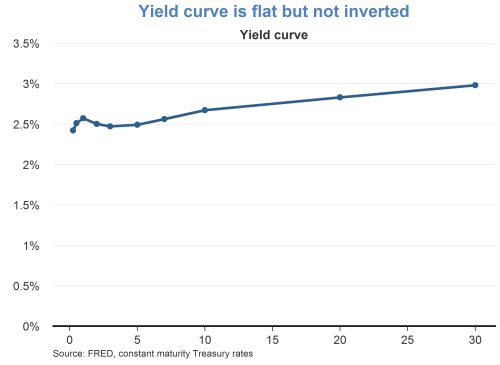

- After the conclusion of the FOMC’s latest meeting held on December 18-19, the committee announced its decision to raise the target range for the federal funds rate to 2¼ to 2½%. The current level of the funds rate is still below our estimate of the neutral rate of 2¾%, indicating that monetary policy remains accommodative. Following the Fed’s release of the December Summary of Economic Projections (SEP), which included fewer rate hikes than indicated in the September SEP, long-term and medium-term Treasury rates declined. Short-term rates increased in line with the federal funds rate, further flattening the Treasury yield curve. As of January 4, 2019, the difference between 10-year and 3-month Treasury security rates is 25 basis points.

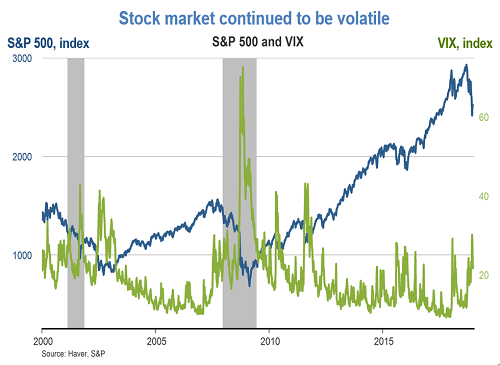

- The stock market has been volatile in the past few months, and ended the year 2018 with a substantial correction of more than 14% from its most recent peak in October. This decline comes on the heels of an unprecedented nearly decade-long expansion. The volatility index (VIX) is now near its historical average.

- The Fed’s Financial Stability Report, published for the first time in November 2018, presents the Federal Reserve Board’s view of the risks to U.S. financial stability. Four sources of potential risks are considered: asset valuation pressures; non-financial sector borrowing, including both household and business borrowing; financial sector borrowing; and financial sector liquidity. The November report states that while the domestic financial system faces risks, arising mainly from elevated asset valuation pressures and non-financial business sector borrowing, financial institutions, particularly the country’s largest banks, are currently liquid and well capitalized. This suggests that U.S. financial institutions are resilient to the risks of repricing and loan losses, and they are unlikely to transmit or amplify shocks to their balance sheets and liquidity. Read the full Financial Stability Report (pdf, 2.5 mb).

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.