Reuven Glick, group vice president at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of October 11, 2019.

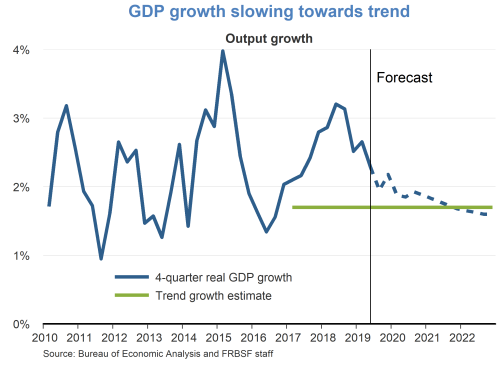

- The U.S. economy continues to grow above trend, but is slowing toward our estimated long-run potential pace of slightly below 2%. The slowdown is attributable to waning tailwinds from last year’s fiscal stimulus combined with growing headwinds from slower foreign growth, rising trade frictions, and the consequent rise in economic uncertainty. Real GDP rose 2.3% in the second quarter over the past four quarters, according to the third report from the Bureau of Economic Analysis.

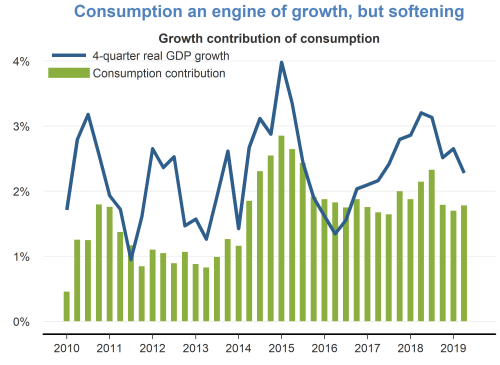

- Consumer spending accounts for about two-thirds of GDP and has been the main driver of overall growth. The growth contribution of consumption depends on the growth rate of consumer spending weighted by its share of overall economic activity. In the second quarter, spending grew at a four-quarter rate of 2.6% and explained 1.8 percentage points of the observed GDP growth rate of 2.3%. Recent monthly data suggests some softening of consumer spending. However, consumer fundamentals still remain fairly healthy with continued job growth and steady wage gains.

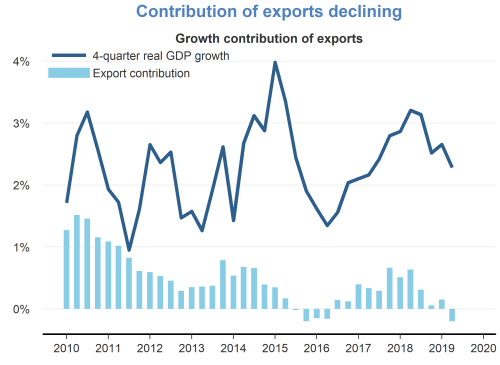

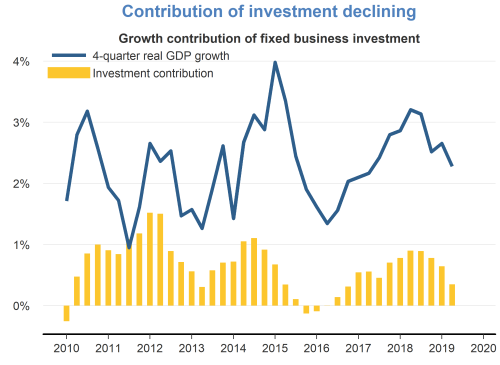

- Other factors, particularly slowing exports and business fixed investment, also have contributed to slower GDP growth over the last several quarters, reflecting the headwinds affecting the economy.

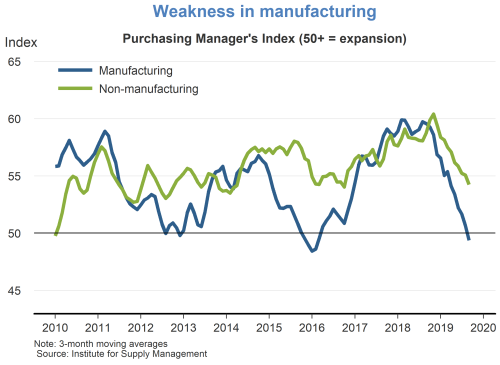

- Monthly purchasing manager surveys provide more timely readings about economic conditions in broad sectors. The Institute for Supply Management (ISM) index for manufacturing fell in August and in September reached its lowest level since the 2009 recession, indicating that this sector may be contracting. The service sector makes up a considerably larger share of the economy than manufacturing and is still expanding, though at its lowest pace in three years according to the ISM’s nonmanufacturing index.

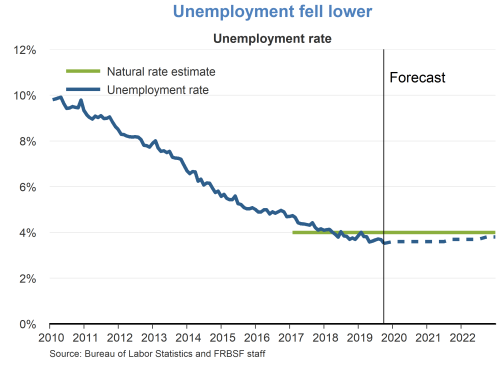

- The labor market remains healthy. U.S. jobs increased by 136,000 in September, while the gains for July and August were revised up by a cumulative 45,000. The six-month moving average was 154,000 jobs in August, a downshift from last year’s average of 223,000. However, job gains are still above the breakeven level needed to absorb new entrants in the labor force over the longer term, which we estimate at around 90,000 jobs per month.

- The job gains helped pull the unemployment rate down from 3.7% to 3.5% in September, the lowest since the 1960s and below our current estimate of its long-run natural rate of 4.0%. Over the medium term, as growth slows, we expect the unemployment rate to gradually revert back toward its natural rate.

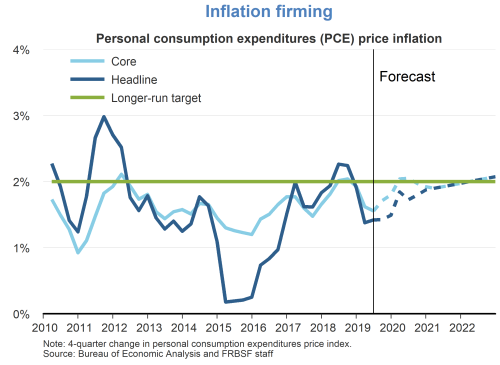

- Inflation remains below the FOMC’s 2% target. The overall personal consumption expenditures (PCE) price index rose 1.4% over the 12 months ending in August. Core inflation, which excludes volatile food and energy prices, rose 1.8%. Given the tight labor market, we expect inflation to reach the 2% objective over the next few years.

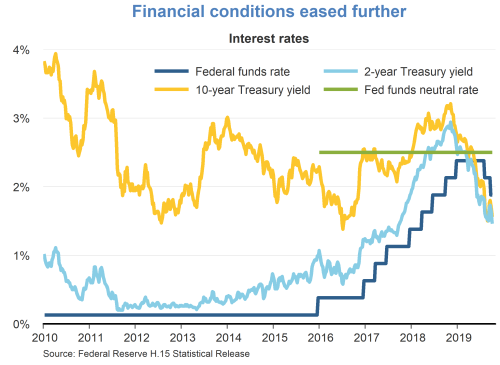

- With inflation below the 2% target and the economy facing growing headwinds, the Federal Reserve has increased monetary accommodation in recent months. At its September meeting, the FOMC cut its funds rate target by 25 basis points to a range between 1.75% and 2%, on the heels of a similar reduction in July.

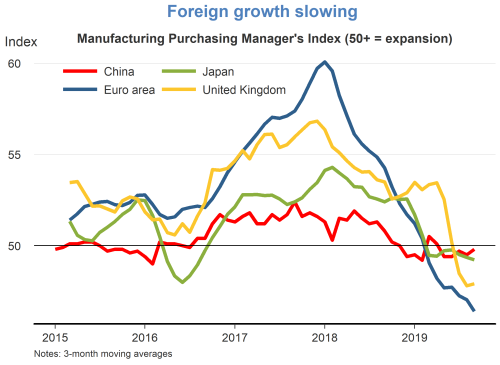

- One of the headwinds facing the U.S. economy is slowing foreign growth, as indicated by declines in manufacturing purchasing indices abroad. Slower growth abroad weakens demand for U.S. exports.

- Some of the weakness in the global economy may be attributed to trade frictions between the United States and China spilling over to other economies. However, much weakness is attributable to local domestic factors. In Germany, car production has dropped because of 2018 structural changes related to stricter emission standards and the potential ban of diesel engine cars in urban areas. In the United Kingdom, concerns about Brexit fallout, particularly if no deal is reached with the European Union (EU), have dampened economic activity. China has sought to slow growth for several years as a way to combat excessive credit buildup in the private sector.

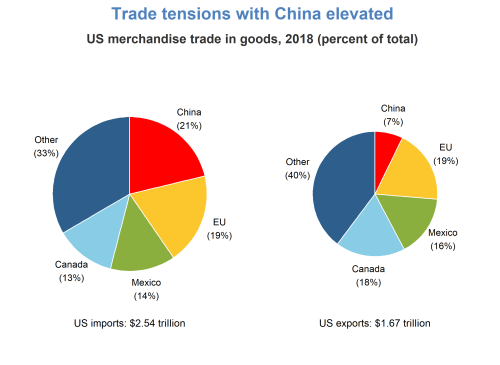

- The trade conflict between the United States and China represents a second headwind. Trade with China accounts for 21% of total U.S. merchandise goods imports and 7% of exports. Since the conflict began in spring 2018, the United States has implemented tariffs ranging from 15% to 25% on roughly 70% of imports from China. Tariffs on most remaining goods are scheduled to be implemented on December 15. China has retaliated in kind by placing tariffs on U.S. exports, though its efforts to retaliate in proportion to U.S. hikes have been hampered because it imports fewer goods from the United States. These actions have raised the costs of U.S. imported goods, reducing the purchasing power of consumers and profits of businesses reliant on Chinese good imports, while also potentially disrupting supply chains.

- Trade tensions with other U.S. trade partners are increasing as well. A recent World Trade Organization decision declared that the EU had improperly subsidized the plane maker Airbus and granted the U.S. justification to apply tariffs on $7.5 billion imports from Europe. The United States has also threatened to impose tariffs on car imports from the EU.

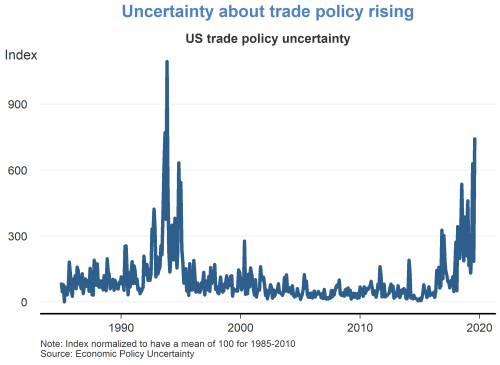

- Uncertainty created by the trade conflicts poses a third headwind to the outlook by adversely affecting business sentiment and investment. Recent escalations of the trade war have heightened trade policy uncertainty to levels not seen since concerns about the formation of NAFTA in the mid-1990s. This uncertainty may be affecting firms by inducing them to postpone or cancel fixed investment decisions.

- The overall impact of these trade disputes on the U.S. economy is difficult to pin down with confidence. However, available estimates suggest that the costs are significant and likely to grow as the trade disputes continue, perhaps putting a meaningful crimp on U.S. growth in the coming year.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.