Daniel Wilson, vice president at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of September 3, 2020.

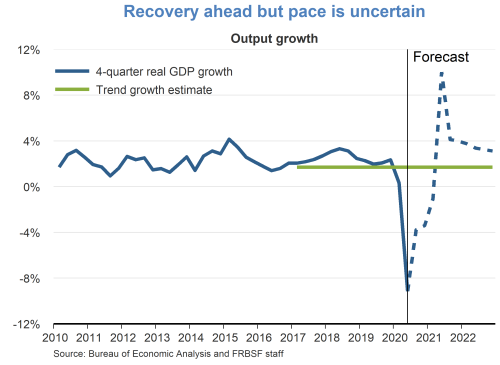

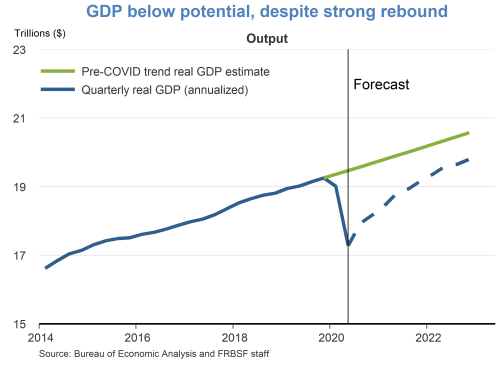

- After the historic hit to real GDP in the second quarter, an economic recovery appears to be underway, and we expect strong real GDP growth in the second half of the year. However, the pace of the recovery is quite uncertain and will depend heavily on the path of the COVID-19 pandemic and the pace of development of vaccines and effective drug treatments.

- Even with the strong growth forecast, it likely will take several years until the level of real GDP returns to the trend path it was on prior to the pandemic.

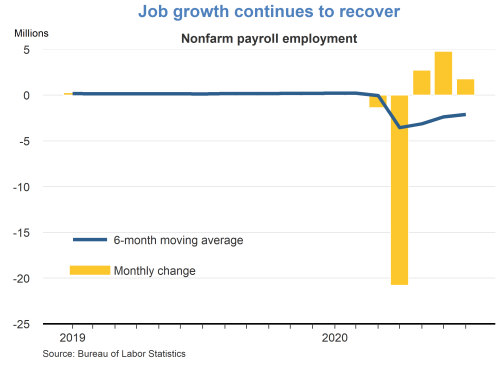

- A similar story applies to the labor market. Like GDP, nonfarm payroll employment plummeted in the spring, falling by over 22 million jobs in March and April. Employment has rebounded strongly in recent months, but far from enough to make up for all of these job losses.

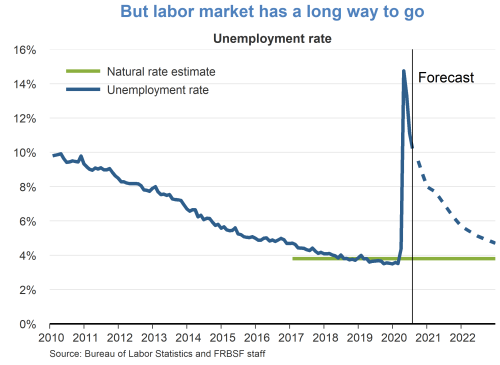

- Correspondingly, the official unemployment rate has fallen from its peak in April of 14.7% to 10.2% in July, but it is still nearly three times higher than it was before the pandemic and is about where it was when it peaked during the Great Recession. We forecast a steady drop in the unemployment rate but do not expect it to return to its pre-pandemic level for many years.

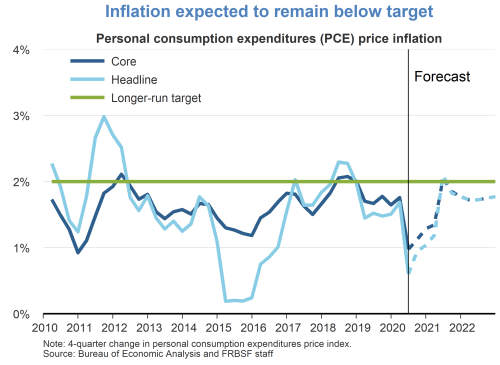

- The huge negative hit to aggregate demand since the onset of the pandemic coupled with drops in oil prices have pushed down both headline inflation and core inflation. Under its recently updated monetary policy framework, the FOMC “seeks to achieve inflation that averages 2% over time.” With the initial hit to inflation over, we expect it to recover going forward, but we do not see inflation reaching 2% on a sustainable basis for several years.

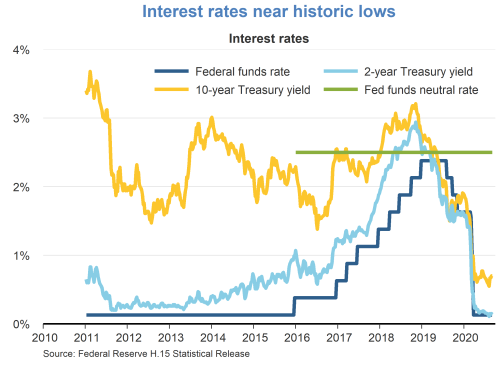

- In response to the pandemic downturn, the Federal Open Market Committee quickly lowered the target federal funds rate down to near zero and launched a series of facilities to calm financial markets. These actions have helped pushed down other interest rates, particularly Treasury bond yields, to near historic lows. Thus, monetary policy and financial conditions are quite accommodative and, together with federal fiscal stimulus, likely have contributed substantially to the economic recovery to date.

- The current and impending fiscal distress facing state and local governments is a brewing risk to the economic recovery. These budgets have been hit hard by the pandemic downturn, with revenues falling sharply because of shrinking income and sales tax bases.

- For instance, a recent study by the Center for Budget and Policy Priorities estimated that total state revenues will fall by $290 billion during the current fiscal year, which as a share of pre-recession revenues is three times larger than the decline during the Great Recession. At the same time, spending needs have only increased, especially in the areas of public health, Medicaid, and unemployment insurance benefits.

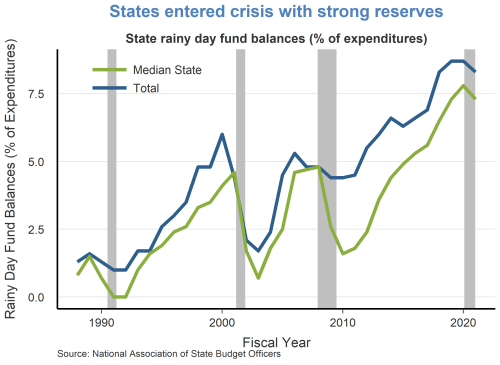

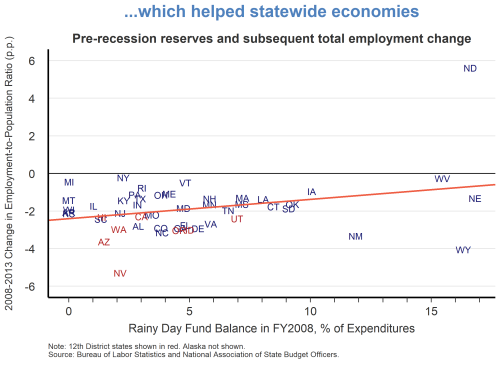

- Fortunately, states entered the crisis with a record-high total of rainy day funds, with an aggregate amount equivalent to nearly 9% of annual expenditures in fiscal year 2020—the year ending June 30, 2020, in most states. In addition, local governments get a considerable amount of their revenues directly from their state governments, so what is good for state finances is good for local finances.

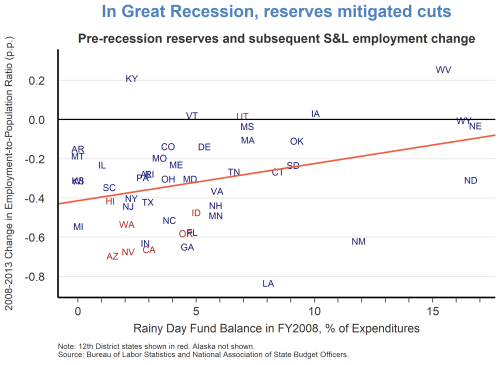

- Rainy day funds help cushion state spending from the effects of revenue shocks. In the Great Recession, states with larger rainy day funds shed fewer state and local government workers (as a share of population) over the subsequent five years compared to states with smaller rainy day funds. These effects carried over to their entire state economy as well. States with larger rainy day funds entering the Great Recession not only saw smaller declines in state and local government employment but also smaller declines in statewide employment. However, in the current environment even rainy day funds as high as 9% of expenditures are likely to be insufficient to make up for the revenue declines facing state and local governments ahead.

- State and local governments are generally prohibited from deficit spending due to balanced budget rules. Their only avenue for long-term borrowing is general obligation bonds for capital infrastructure projects. Therefore, budget shortfalls must be closed in the near term by either tax increases or spending cuts. Because governments are loath to raise taxes in the middle of a recession, we should expect major budget cuts to come.

- Indeed, state and local budget cuts have already begun. The evidence from the Great Recession suggests that, if history is any guide, the state and local budget cuts to come likely will be an important drag on aggregate employment and economic growth over the next few years.

TopicsInflation

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.