Robert G. Valletta, associate director of research and senior vice president at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of December 1, 2022.

- As the year 2022 comes to a close, our focus remains on high inflation and the prospects for it to fall. Monetary policy has shifted toward an increasingly restrictive stance in response to persistently high inflation. This shift has raised inevitable questions about the extent of cooling in economic activity and the labor market in response to the Fed’s policy tightening.

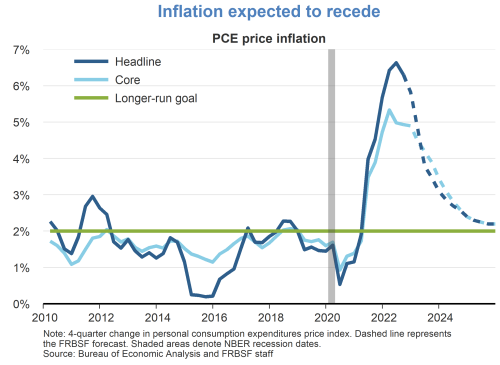

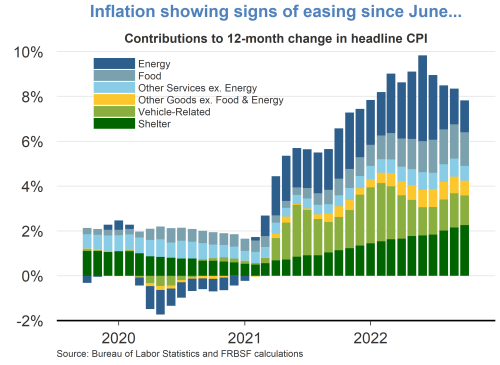

- Recent data suggest that inflation may have peaked. In the third quarter, the headline personal consumption expenditures (PCE) price index was up 6.3% on a four-quarter basis, while the core PCE index that excludes food and energy was up 4.9%. Both of these figures are down a few tenths from their highs earlier in the year. Data through October for the consumer price index (CPI) also show that incoming inflation readings have been easing since June. Price increases for some types of goods have slowed considerably, notably for used vehicles. By contrast, price increases for services remain high, in large part due to continued increases in the pace of shelter inflation, which often trails broader adjustments in housing market conditions.

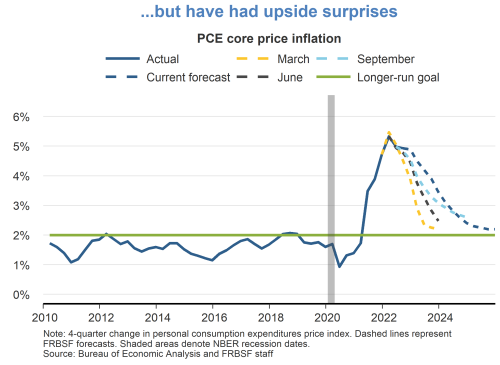

- We project that inflation will continue to recede gradually but not reach the Fed’s 2% average goal for another three years or more. Moreover, we judge the risks to this forecast as weighted to the upside. Prior forecasts have consistently underestimated the extent and persistence of existing inflation pressures. The repeated upside surprises may reflect pandemic-related supply disruptions that lasted longer than expected but now appear to be relenting. However, strong consumer demand has also contributed to elevated inflation readings, suggesting that a sustained slowing of economic activity is needed to bring inflation down.

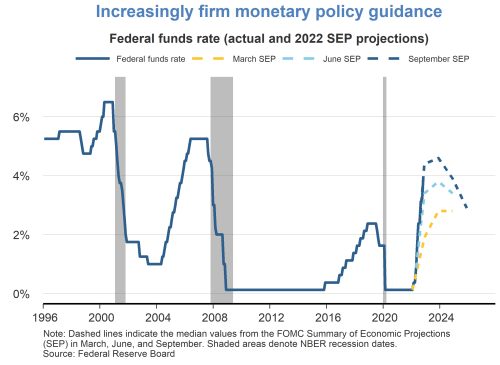

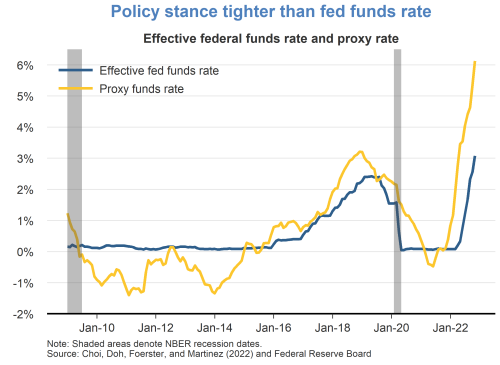

- Monetary policy has responded to persistent elevated inflation this year via substantial tightening. The Federal Open Market Committee (FOMC) has raised the federal funds rate by nearly 4 percentage points since March, which is the fastest pace of increases in four decades. This rise in the short-term lending rate has been accompanied by ongoing reductions in the Federal Reserve’s balance sheet, which began in June 2022, and forward guidance about the likely path of the federal funds rate. These additional elements of monetary policy tend to reinforce movements in the funds rate by pushing up longer-term rates as well.

- Consistent with this ongoing shift in the stance of monetary policy, broader financial market indicators show even tighter conditions than does the funds rate alone. In particular, as of October, a proxy funds rate that accounts for a broad set of financial indicators registered slightly above 6%, about 2 percentage points above the Fed’s target range of 3.75 to 4% announced at the conclusion of the most recent FOMC meeting on November 2.

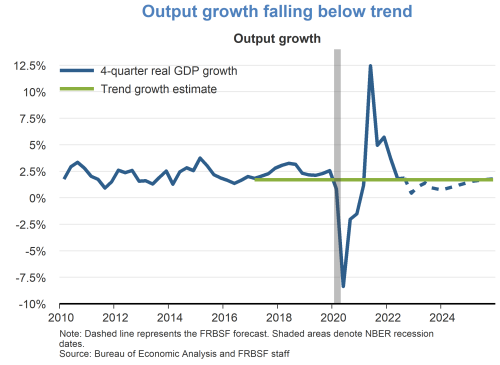

- Tighter monetary policy restrains growth and inflation, but the process is slow and typically spread out across multiple years. The slowdown had already begun in the first half of this year, when real Gross Domestic Product (GDP) fell 1.1% at an annual rate. Despite a bounceback in the third quarter to 2.9% growth, we expect growth to remain well below trend this year and next year before converging back to trend in 2025.

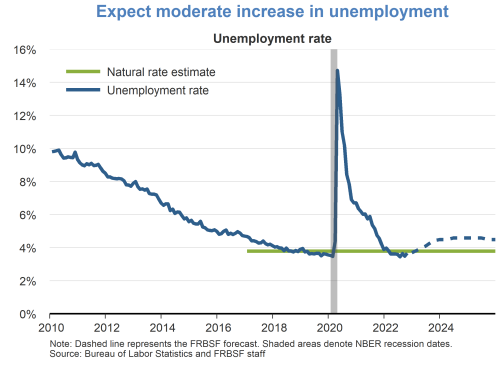

- As the expected slowdown continues, a key question is how much the labor market will cool. Monthly employment growth and other indicators of labor demand such as job openings have fallen from their peaks earlier this year. Nevertheless, the labor market remains unusually strong by historical standards, with unemployment still near the 50-year low of 3.5% recorded most recently in September 2022. We expect a moderate increase in unemployment of about one percentage point through 2024.

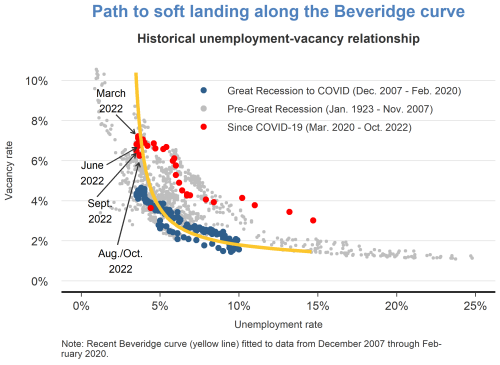

- The degree to which the unemployment rate rises as labor demand cools depends in part on the shape of the so-called “Beveridge curve.” The Beveridge curve depicts a negative relationship between the unemployment rate and the strength of labor demand, as captured by the vacancy (or job openings) rate. The vacancy rate reached unusual highs during the rapid labor market recovery from early 2021 through early 2022. Research suggests that the underlying Beveridge curve relationship can support a reduction in vacancies back to pre-pandemic levels without a large increase in the unemployment rate. A significant decline in the vacancy rate since March, without any meaningful increase in unemployment, bolsters this perspective.

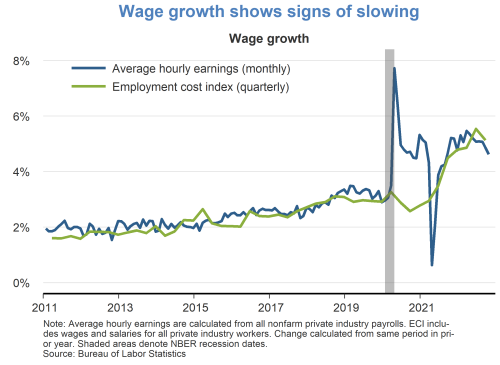

- Softening labor market conditions may be starting to show through to wage growth. Growth in average hourly earnings (on a 12-month basis) has moderated, falling nearly one percentage point from a peak of 5.6% in March to 4.7% in October. Wage growth measured by the four-quarter percentage change in the employment cost index also edged down recently, but the decline was only a tenth of a percentage point, occurring between the second and third quarters of this year.

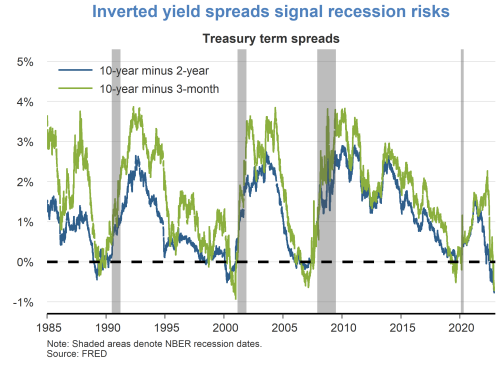

- Although we expect continued growth, we view the risks to economic activity as weighted to the downside. Recession signals from financial markets are now sounding the alarm, most notably the inverted spreads between yields on long-term and shorter-term Treasury bonds. Such yield curve inversions have proven historically to be reliable predictors of recessions over the subsequent 12 months. After some divergence earlier this year, two leading measures of the yield spread have now both become inverted. Their predictions come with substantial statistical uncertainty, however, and are not definitive indications that a recession is looming.

TopicsInflation

About the Author

Robert G. Valletta is senior vice president and associate director of research in the Economic Research Department of the Federal Reserve Bank of San Francisco. Learn more about Robert G. Valletta

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.