Evgeniya Duzhak, regional policy economist at the Federal Reserve Bank of San Francisco, stated her views on the current economy and the outlook as of February 10, 2022.

- The strong economic recovery from the impact of the coronavirus pandemic continued in the last quarter of 2021, and growth remains robust. Despite the spike in COVID-19 cases due to the rapid spread of the Omicron variant, economic output expanded at a solid pace, and further gains emerged in the labor market. Numbers of new COVID-19 cases began to sharply decline across the United States in January, and we expect the positive momentum in the recovery to persist. Nevertheless, the overall economy remains sensitive to the future path of the virus.

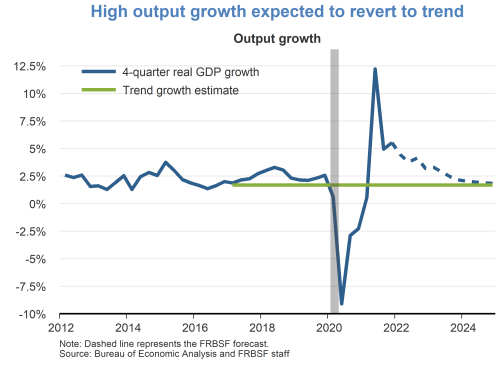

- The U.S. economy expanded at a fast pace during the fourth quarter of 2021, with real GDP growing at an annualized rate of 6.9%. The largest contributing factor was the buildup of business inventories that needed to be replenished following drawdowns in response to high demand combined with supply chain disruptions. Personal consumer spending also contributed to growth over the quarter. The rapid expansion in the fourth quarter brought real GDP growth rate to a healthy 5.5% during 2021.

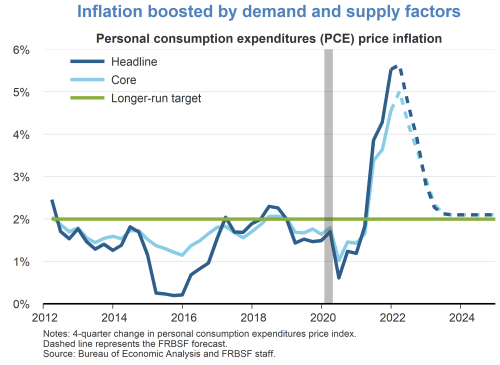

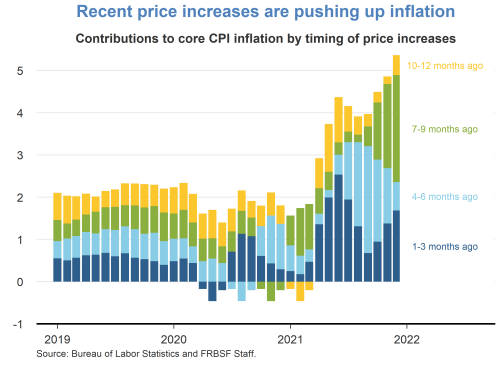

- Prices of goods and services have been rising rapidly. The headline personal consumption expenditures (PCE) price index increased by 5.8% in the 12 months through December 2021. The core PCE price index, which excludes the more volatile food and energy components, rose at a rate of 4.9% compared to a year ago. Global supply chain disruptions along with waves of COVID-19 infection and their resulting effects on worker availability continued to hamper the supply side of the economy, amplifying pressure on prices. At the same time, overall monetary and fiscal conditions remained accommodative and further contributed to households’ asset balances and income levels that have added to demand pressure on prices. For most of the pandemic period, service sector inflation has been notably lower than goods inflation, as consumers curtailed spending on in-person activities and shifted their demand towards goods, particularly durables. However, in recent months, price increases have become more widespread across the economy. Rising shelter costs accounted for a significant portion of recent inflation.

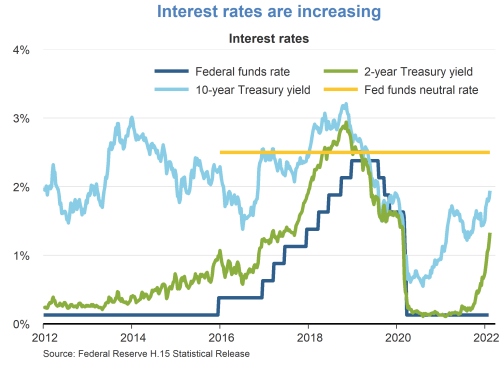

- At its most recent meeting in January, the Federal Open Market Committee kept the federal funds rate unchanged at a target range of 0% to 0.25% and announced that its tapering of asset purchases will be concluded by March 2022 as well as that it “expects it will soon be appropriate to raise the target range.”

- Interest rates reacted to economic news, particularly on inflation, as well as the prospect of less accommodative stance of monetary policy. Yields for Treasury securities rose across all maturities with faster gains at the short end of the yield curve. The yield on 2-year Treasuries rose by 1.2 percentage points relative to a year ago, while the 10-year Treasury yield increased by a 0.7 percentage points over the same time horizon. The decrease in the spread between the two means that the yield curve flattened by about half a percentage point.

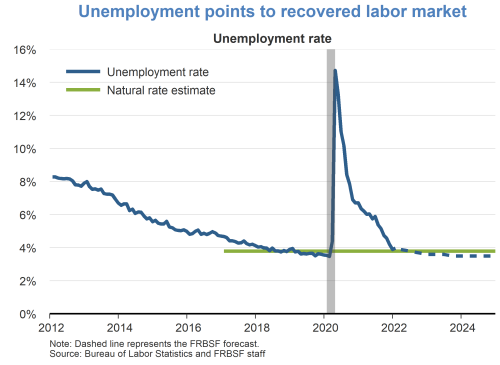

- The improvements in the labor market reflect the economy’s robust recovery from the coronavirus pandemic. The unemployment rate in January stands at 4.0%, close to the natural rate of unemployment which we estimate to be around 3.8%. Demand for workers remains strong, with 467,000 jobs added in January 2022 and noticeable upward revisions to the prior two months. Some of the gains were offset by updated population estimates. Overall, total employment is still 2.9 million jobs below its pre-pandemic level. Labor force participation stands at 62.2%, below its pre-pandemic level in February 2020 of 63.4%.

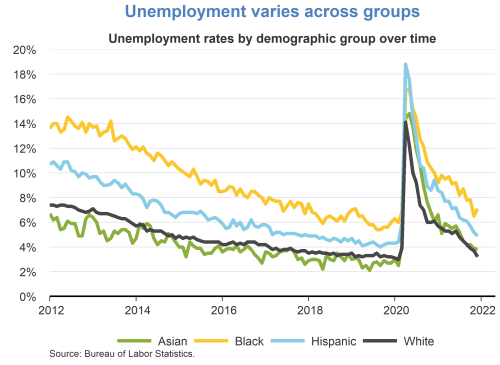

- A breakdown of unemployment rates across various demographic groups displays significant disparities, with unemployment among Blacks and Hispanics typically higher than rates for Asians and Whites. In addition, the magnitude of these disparities varies with the business cycle, rising with recessions and declining with expansions. Thus, the unemployment gap between Black and Hispanic workers, on the one hand, and Asian and White workers, on the other, rose greatly during the 2007-08 financial crisis. The ensuing long economic expansion through 2019 helped to significantly reduce unemployment among Black and Hispanic workers, narrowing the gap with the other demographic groups.

- While unemployment rates for Black and Hispanic workers as well as male workers has generally been more sensitive to business cycle downturns than unemployment for Asian, White, and female workers, the pattern during the recent pandemic recession has been different. In particular, unemployment among Asian workers rose more during COVID-19, while Black unemployment rose much less in comparison to past recessions.

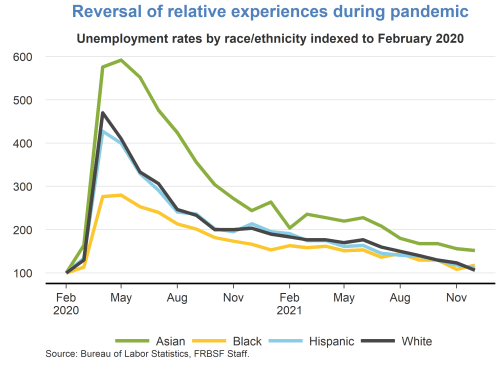

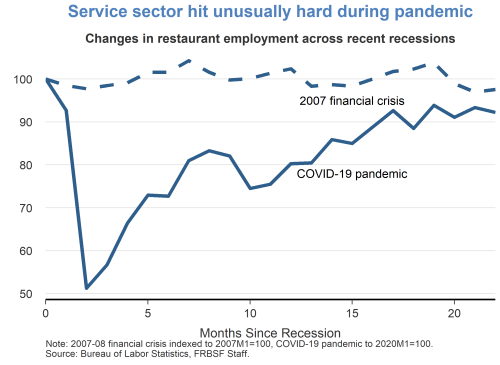

- Sectors that have tended to lose the greatest number of jobs during a recession include construction, production, transportation, and material moving, while the recent pandemic downturn has had a more adverse impact on service industries and occupations with higher social contact. For example, Asian restaurant workers, especially those with lower education, experienced a relatively higher rise in unemployment. Increases in the unemployment rates for Black and Hispanic workers were softer due to their higher representation in occupations in the construction and production sectors. Consequently, the gap between groups with the lowest and highest unemployment levels is not as wide as it has been in past recessions. Current unemployment rates are close to their pre-pandemic levels for most demographic groups.

TopicsInflation

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.