The San Francisco Fed has launched a new data page that helps gauge the stance of monetary policy under various types of actions. The Proxy Funds Rate page focuses on financial market indicators, which show the influence of the Fed’s forward guidance and asset sheet actions beyond what can be seen through the level of the federal funds rate.

The evolution of conducting monetary policy

For many years, the Federal Open Market Committee (FOMC) conducted monetary policy solely through changes in the federal funds rate—the short-term interest rate that is the basis for other interest rates in the U.S. economy. However, to help the economy recover from the Great Recession, the FOMC needed to begin relying on additional ways of putting policy into action, specifically through forward guidance and the balance sheet.

Using these new tools has become an effective way of helping the Fed guide the economy toward its dual mandate goal of stable prices and maximum employment. But because the tools are different, it’s challenging to find a single way to measure the broad stance of monetary policy. In other words, how do we know whether forward guidance and changes in the balance sheet are having an effect, and can we summarize the multiple tools into an easy-to-interpret indicator?

Developing the proxy funds rate

We discuss a way to track this in our recent FRBSF Economic Letter, “Monetary Policy Stance Is Tighter than Federal Funds Rate.” In the Letter, we detail a “proxy funds rate” that uses financial variables to assess the broad stance of monetary policy.

The idea is that, when the FOMC issues forward guidance—communicating the likely course of future policy—or makes changes to the size or composition of the Federal Reserve’s balance sheet, these actions affect financial markets. The proxy rate translates a set of financial variables into a rate that is comparable to the federal funds rate.

In other words, the proxy rate can be interpreted as indicating what federal funds rate would typically be associated with prevailing financial market conditions if the funds rate were the only monetary policy tool being used.

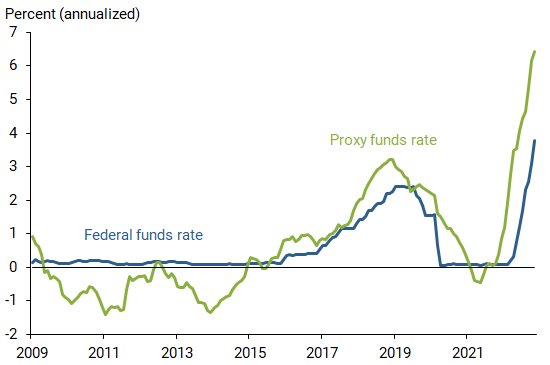

Recently, the FOMC has raised the federal funds rate target, issued forward guidance for additional rate increases, and decreased the size of the balance sheet. These actions have tightened financial conditions. In early November 2022, the FOMC raised the funds rate target to between 3¾ and 4%. But the tighter financial conditions meant that the proxy rate through November was 6.42%.

This gap between the proxy rate and the funds rate means that financial markets are reacting as if the main policy rate is higher than it actually is. Being mindful of the gap can help policymakers assess how much tighter policy needs to go to achieve price stability, while also guarding against tightening too much (Daly 2022).

Figure 1: Proxy funds rate and effective federal funds rate, 2009-present

Monthly updates to proxy funds rate data

To continue tracking how the stance of monetary policy evolves, we will update the proxy funds rate series every month on our new data page.

How this series evolves can help gauge how fast policy is tightening or loosening. This information can help us assess the effectiveness of the Fed’s forward guidance or balance sheet policies. It can also make it easier to compare how effectively current monetary policy is working toward the Fed’s goals relative to times when only the federal funds rate was used.

References

Choi, Jason, Taeyoung Doh, Andrew Foerster, and Zinnia Martinez. 2022. “Monetary Policy Stance Is Tighter than Federal Funds Rate.” FRBSF Economic Letter 2022-30, November 7.

Daly, Mary C. 2022. “Resolute and Mindful: The Path to Price Stability.” FRBSF Economic Letter 2022-33, November 28.

Doh, Taeyoung, and Jason Choi. 2016. “Measuring the Stance of Monetary Policy on and off the Zero Lower Bound.” FRB Kansas City Economic Review 101(3), pp. 5-21.

You may also be interested in:

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.