The development of a robust offshore bond market is an important pillar of China’s renminbi internationalization strategy. For the renminbi to become a global currency, foreign investors need access to deep and liquid markets of renminbi-denominated securities. Offshore renminbi bonds, colorfully referred to as dim sum bonds, are intended to serve as a source of renminbi debt securities for foreign investors. However, like other aspects of renminbi internationalization, the growth of the offshore bond market has been halting and uneven.

One indication of a currency’s global status is the amount held by foreign investors. If a currency is seen as an attractive store of value, non-residents will be willing to hold it beyond temporary use for trade settlement and other payments. An example of this is the large foreign holdings of dollars and dollar-denominated securities, both inside and outside of the United States. A currency is more desirable when there are large and open capital markets that allow investors to earn a return and manage liquidity needs in that currency.

Although China’s domestic bond market has begun to open up to international capital flows, formal and informal limitations on outflows make onshore securities too illiquid for general use and continue to deter wider participation by foreign investors. Recognizing this limitation, Chinese authorities have actively promoted the development of an offshore bond market, which is free from capital controls. In fact, the Chinese Ministry of Finance issued its first offshore bond in 2009, during the early stages of the renminbi internationalization process.

The first dim sum bond was issued in 2007 in Hong Kong by China Development Bank. As renminbi internationalization progressed, other global financial centers eagerly entered the offshore renminbi bond market. Taiwan, London, Singapore and Frankfurt have all permitted renminbi bond issuances. Hong Kong, however, remains the dominant market for offshore renminbi bonds.

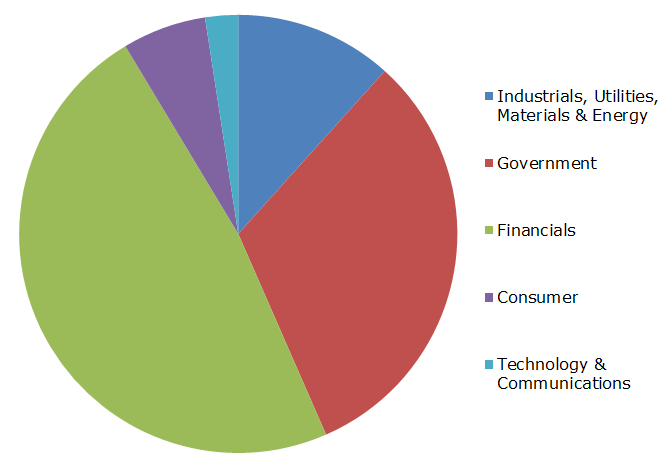

Issuers from 38 different economies have sold offshore renminbi bonds, but Chinese entities make up the majority of issuers. As seen in Figure 1, the largest issuers of offshore bonds are financial institutions, followed by government organizations. Together, these two entities account for nearly 80 percent of the market.

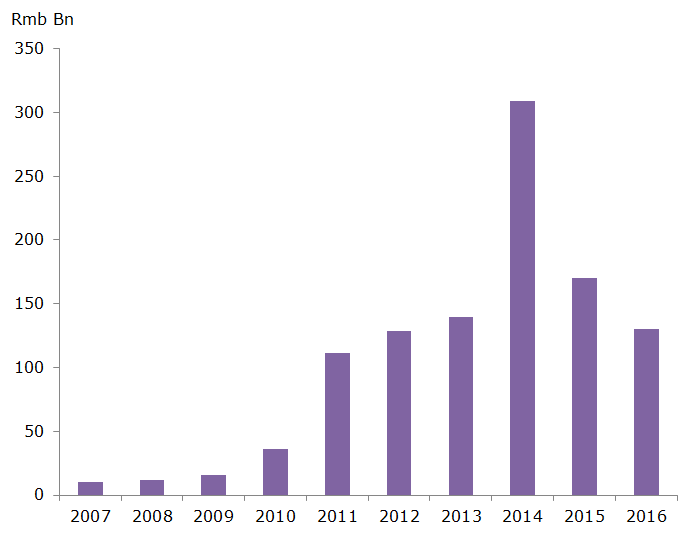

Figure 2 shows that while offshore renminbi bond issuances grew rapidly at the outset they have since slowed dramatically.

What explains the slowdown in the once-promising offshore bond market? As with the other aspects of renminbi internationalization, the desire to hold renminbi bonds is influenced by the exchange rate. The widespread expectation that the renminbi would continue to steadily appreciate against the dollar made offshore renminbi bonds attractive. In addition to the bond yield, foreign investors could count on an additional return when they converted their funds back into dollars.

When the renminbi began a sustained period of depreciation against the dollar in 2014, the calculus for many investors changed. The currency carry became negative, reducing the attractiveness of renminbi bonds. The corresponding decline in offshore renminbi deposits has also meant that there are fewer sources of renminbi to be invested in offshore bonds.

Additionally, as the Chinese economy has slowed, interest rates have declined substantially for both onshore and offshore bonds. The reduced yield combined with the depreciation of the currency mean that the expected return on many bonds is low or even negative.

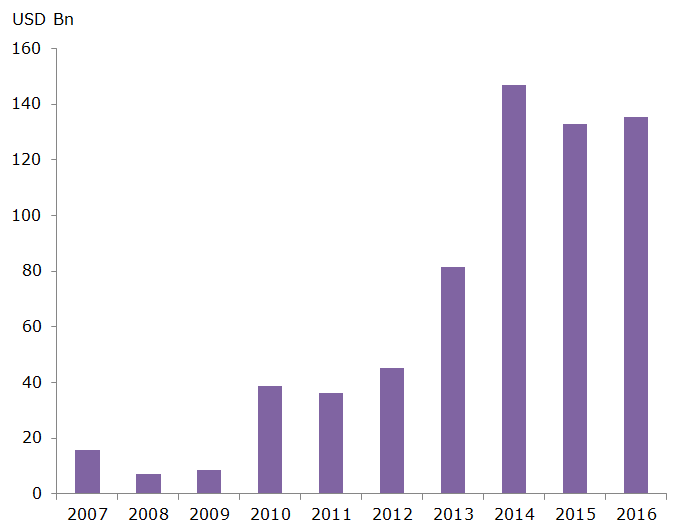

Importantly, the slowdown in the offshore renminbi bond market does not seem to reflect a wider skepticism towards Chinese issuers. As shown in Figure 3, the dollar bond issuances by Chinese entities declined in 2015 before recovering moderately in 2016. Overall, the USD bond market for Chinese issuers is more than six times larger than the offshore renminbi bond market.

The need for an offshore bond market may ultimately be lessened by onshore financial reforms. Last year the Chinese government took steps to liberalize access to the large interbank bond market for foreign central banks, sovereign wealth funds, and institutional investors. These changes, along with the renminbi’s inclusion in the International Monetary Fund’s Special Drawing Rights (SDR), have already led to a noticeable increase in foreign holdings of Chinese bonds. Overall, however, the share of Chinese bonds held by foreign investors remains minimal. The Chinese government has also encouraged the development of Panda bonds, onshore renminbi bonds sold by foreign entities. Although the onshore market is not yet open enough to serve as a replacement for the offshore market, this may change over time with additional reforms.

The offshore renminbi bond market is one of the many elements of renminbi internationalization that has slowed recently. In the short-term, uncertainty around the exchange rate will continue to hinder development. Over a longer period, investor demand for exposure to China seems likely to spur further growth, but the offshore market will face strong competition from an increasingly liberalized onshore bond market.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.