Walter Yao

For those who follow China’s banking sector closely, credit quality has always been a top regulatory concern. Many predicted that due to fallout from the 2008 stimulus package and the subsequent excessive growth of bank lending, balance sheet weaknesses would start to emerge as economic growth decelerated. China’s ongoing rebalancing efforts also added to worries that default rates might spike for “old economy” borrowers, such as steel makers and coal miners.

Problem loans started to grow steadily after 2011, and had more than quadrupled by Q2 2018, to US$296 billion. Nonetheless, the system-wide nonperforming loan (NPL) ratio—defined as the sum of “substandard”, “doubtful,” and “loss” loans as a share of total loans—only increased moderately from 1 percent of all balances, to 1.86 percent. However, the health of the headline numbers is largely due to a steadily expanding denominator: Total loans during the same period increased by nearly 150 percent.

Period-end NPL numbers are just snapshots and do not reflect NPL disposal efforts by banks, or the magnitude of NPL formation.1 Between 2012 and 2017, publicly listed large and joint-stock Chinese banks collectively charged off US$267 billion in problem loans, according to SNL data. Without these charge-offs, the outstanding NPLs would have been much larger in size. For this group of banks, average credit costs in 2017 were 38.5 percent of pre-impairment operating profit. Aggressive provisioning served to dampen earnings and put pressure on banks to raise capital, but also helped shore up banks’ balance sheets.

Bank analysts are also concerned that reported NPL ratios do not accurately reflect underlying trends in credit quality. China’s five-category loan classification system is consistent with some Asian and Latin American jurisdictions, but different from the practice in the United States, where nonperforming loans are defined as non-accrual loans plus loans 90+ days past due (PD) but still accruing interest.2

The concern is that some loans may be classified as “special mention” even though they carry considerable credit risk. In China, the majority of bank loans are extended to large businesses and secured by land and properties. Due to the rapid appreciation of land and property values in many Chinese localities, loans are often well over-collateralized, which may be a justification for banks to conclude that full repayment is not in doubt despite emerging signs of borrowers’ financial troubles.

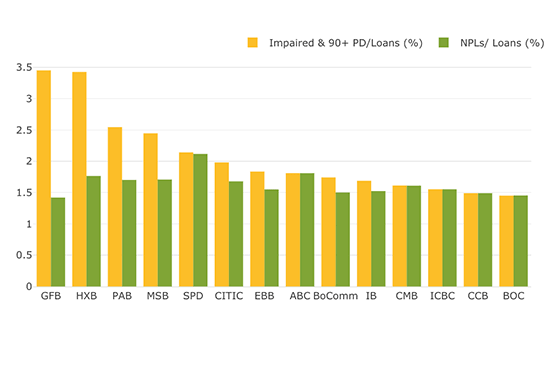

Another measure reported by Chinese banks in their annual reports – the ratio of impaired and 90+ days PD loans to total loans – provides an alternative angle into asset quality. Compared to China’s statutory NPL ratio, this other measure is better aligned with the regulatory practice adopted in the United States.

For large banks, the difference between the two measures is often minimal. However, Figure 1 shows that for several joint-stock banks, impaired and 90+ days PD loan levels are significantly higher than nonperforming loans. Private sector analysts believe the discrepancy is likely even larger for small lenders, such as city commercial banks and rural commercial banks.

Asset quality indicators for select Chinese banks (2017)

Recent regulatory tightening may help narrow the gap. According to Chinese media reports, the China Banking and Insurance Regulatory Commission (CBRIC) has started to require all Chinese banks to recognize all 90+ days PD loans as nonperforming loans, and expand loan loss allowances accordingly.

The broader impact on large and joint-stock banks is likely to be limited. Most of them, especially those that are dual-listed and audited by top accounting firms, have adopted strict loan recognition practices for years. But small lenders are more vulnerable. According to a UBS estimate, city commercial and rural commercial banks could see annual NPL growth of 27 percent and 33 percent, respectively, due to the tightening standards.

UBS forecasts the total impact to the banking sector translates to a 14 percent increase in NPL volume—not insignificant, but also not catastrophic. In fact, a back-of-the-envelope estimate assuming all city commercial and rural commercial banks experience a 300% increase in NPLs suggests the banking sector’s NPL ratio would still remain below 5 percent. For comparison and context, when China experienced a banking crisis in the 1990s, as much as one third of total loans were nonperforming.

Despite those assurances, pockets of risks remain – and anecdotes suggest as much. One rural commercial bank reportedly saw NPL ratios surge to 19.5 percent at end-2017 – compared to 4.1 percent the previous year – after classifying 90+ days PD loans as nonperforming loans. Due to the spike in NPL ratio, the bank’s capital adequacy ratio plunged to less than 1 percent. Banks with similar experiences will likely scramble to replenish capital in order to restore capital ratios and loan loss allowance ratio to levels required by regulators. At the same time, their cost of funding is also poised to increase significantly as higher NPL levels trigger downgrades in issuer ratings.

For the banking sector, the move is a painful but necessary step towards bringing small lenders in line. Tightening standards also means there will likely be significant recapitalization needs down the road, with a related slowing growth in bank credit as small lenders sort out their balance sheets.

1. For in-depth discussion of Chinese banks’ NPL disposal, see “China’s Recent Efforts to Deal with Stressed Loans” and “Chinese Banks are Writing Off More Loans and That is a Good Thing.”

2. For a cross-country comparison of NPL definition, see “Not All NPLs Are Created Equal.”

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.